At points in time where there seems to be a vacuum of NO important or market moving information, investors should focus on basic fundamentals of companies. The primary concern in a market uptrend is whether there is still more upside ahead or if the advance has more reasons to end. What normally is the case is that as equity prices rise, they become more expensive based on past earnings that have been reported. The phenomenon that we are experiencing now is very different. Are stocks becoming cheaper? Investors, or should I say market prognosticators that are warning of another dot-com-style bubble are focused on prices while ignoring earnings. Despite the S&P 500 rising more than 9% year-to-date, its forward P/E ratio has actually fallen from 22.2x to 20.4x. Earnings estimates have grown roughly twice as fast as the index itself, meaning the market is getting cheaper on fundamentals — not expanding multiples. In fact, the S&P 500 now trades at a similar multiple to May 2024, yet the index is over 40% higher. The “bubble” many fear is becoming cheaper, driven by strong earnings growth rather than speculation. This is virtually unheard of. If earnings are rising, and rising faster than forecasts- as I have been writing about every week, then why are prices not reflecting this? I believe that it is a function of fear. Here is a picture of P/E progression and where we are currently:

Many have been concerned that stocks are way overvalued, but the current AI-driven market rally is not repeating the extreme valuation excesses of the dot-com bubble. AI is not wiping out jobs. It is creating different jobs, and it is making existing jobs much more efficient. Current stock prices are relatively reasonable, while analyst projections for future profits (especially in semiconductors and tech) have reached historic highs. This mismatch suggests the potential "bubble" is confined to spreadsheets rather than actual market prices.

Current valuations remain tame:

- Tech stocks: 22.2x forward earnings.

- S&P 500: 20.4x forward earnings.

- Semiconductor stocks: 18.4x forward earnings (actually cheaper than the broader market).

Dot-com peak in March 2000) historical comparison:

- Tech: 55x forward earnings.

- S&P 500: 25x forward earnings.

My point here is really the drill down. In the New York Times a couple of weeks back there was a very illuminating article about how the majority of the return of the US equity market over the last 100 years could be attributed to only 10 companies. The majority of these companies are technology companies. Today, the hot spot in technology is in the semiconductor / memory space. The bantering is almost relentless on how to wrap one’s brain around this. Semi’s and memory have always been a very cyclical business, but now with the datacenters and the accelerating demand for them not only has the cyclicality been eliminated, but the demand is virtually unquenchable. With this, prices are sure to rise to stratospheric levels, but many companies are setting up their future expenditures by locking in prices and paying today for memory and chips in some cases five years out. This is completely unheard of.

As all of the hoopla on this space has been going on, in the background the Magnificent 7 giant technology companies have been in a pretty solid decline since last November. The semiconductor space picked up the baton and ran with it until about a week and a half ago and then the wheels sort of came off once profit taking kicked in. If we are to look at the major index, the S&P 500 though, it is clear that the other 490 companies in the index have been picking up the slack and the index has remained elevated. I believe that this is a function of the true strength within the US economy and the deflationary and added profitability AI has provided to the other industries within the index. Nonetheless, the index after a straight us run since March, has been in a virtual tug-o-war. Here is a picture of what the index has been doing this year with a circle around this indecision period we have been in since early May:

The question on all investors’ minds now is which way the indexes are going to break out of this indecision area. To answer this, I tend to think about where else the money could go where it is going to be expected to be treated better. If the market is done going up, then when the money leaves, it needs to go somewhere else that it is trying to be treated better. Baring simply going to the sidelines and sitting in cash or short-term money markets, it will instead go to another asset class that is exhibiting opportunity. Developed international (due to wars and oil dislocation) doesn’t appear to be the place. Commodities- by looking at gold, silver, oil, and copper doesn’t appear to be the place. Crypto has been in a so called, “Crypto Winter” and doesn’t appear to be the place. So, this leaves the Emerging Markets and Bonds. The Emerging Markets have seemed to hold up quite well as the wars rage on in the Ukraine and Iran. I believe this is due to the fact that the emerging market tend to benefit from natural resource demand and cheap labor yet tend to be mostly unaffected by conflicts. The one that I want to discuss a bit more is the bond market.

Bond prices have been weak since interest rates have been going up. When interest rates go up, bonds become more attractive as a tradeoff to stocks and tend to signal points in time when US equities tend to drop when interest rates (the cost of capital) rises. The issues that could make it a bit different “this time” is that interest rates could be rising simply because the economy is so strong and oil prices have been high both of which tend to be inflationary. If the rise in rates is due to economic strength, and if the P/E ratios of the broad basket of US stocks is falling, then there doesn’t necessarily appear to be overvaluation that could cause the indexes to decline substantially. If on the other hand the economy wasn’t healthy and if the valuations were being stretched, then there could be a different situation at hand.

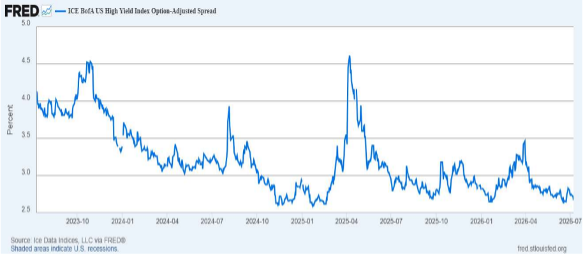

The next question seems to be, “So, if the earnings on the S&P have been rising faster than forecasts, and if this has been occurring consistently for a number of quarters, then eventually the advance could get tired and earnings could plateau.” If this were the case, then private equity would be expected to crack, private debt would experience a higher level of defaults and High Yield vs. US Government interest rate spreads would begin to expand. As I wrote last week and I am repeating here, this hasn’t happened yet. While rates have spiked higher lately, we are not witnessing much evidence of concern in the credit markets. The ICE BofA US High Yield Index Option-Adjusted Spread has been coming down even as rates have gone up. The relative calmness is another factor that seems to support giving the rally in stocks the benefit of the doubt until proven otherwise. Here is a clear picture of how this looks currently:

If bonds are not a place to be and neither are the other asset classes, and if stocks are actually getting cheaper because earnings are growing even faster than prices, then remaining in equities should prove to be the best option currently. This may or may not change based on how companies report second quarter earnings, but this is the next chapter yet to be written.

This week’s note is a bit shorter as we await the second quarter earnings. Labor remains strong, wages remain firm, and inflation remains in check. Great companies in the industries that are benefiting from the current environment should remain the focus. As far as AI and the explosion in semiconductors and memory are concerned, there is an infinite amount being written about how strong demand currently is and how strong it is expected to be. This is another chapter that we are all waiting for with bated breath.

“You have brains in your head. You have feet in your shoes. You can steer yourself any direction you choose. You're on your own. And you know what you know. And YOU are the one who'll decide where to go...”

― Dr. Seuss, Oh, the Places You’ll Go!

-Ken South, Tower 68 Financial Advisors, Newport Beach

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The S&P 500 is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States. Indexes are unmanaged and cannot be invested in directly.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The NASDAQ Composite Index measures all NASDAQ domestic and non-U.S. based common stocks listed on The NASDAQ Stock Market. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the Index. Indexes are unmanaged and cannot be invested in directly.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

Data sourced from Bloomberg (2025).

Stock investing includes risks, including fluctuating prices and loss of principal.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Bonds are subject to availability, change in price, call features and credit risk.

Government bonds are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

Bond yields are subject to change. Certain call or special redemption features may exist which could impact yield.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor’s portfolio. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

The financial professionals with Tower 68 Financial Advisors are registered with, and securities and advisory services are offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC.

LPL Tracking # 1139202