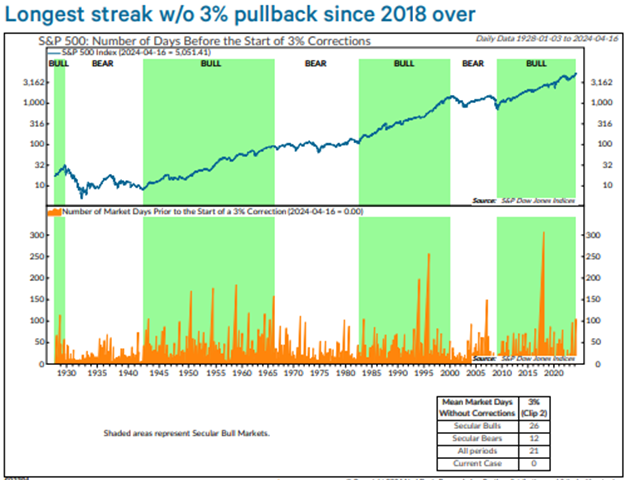

US stock market investors had been enjoying a period of historically low downside volatility (unabated advance) and consistent upside of late. The S&P 500 Index had not endured a 3% correction since 10/27/2023, the longest stretch since the 308-day streak ending on 1/26/2018. Almost on cue, the S&P 500 dipped more than 3%, ending the streak at 105 trading days (chart, below).

The reasons as to “why” the advance has started to sputter are numerous. Since there is NEVER a lack of negative news items (both domestic and international) that can be pegged as “the reason,” I believe that it becomes more of a tug-o-war that eventually starts to go in the other direction once there are enough reasons to tilt the strength of data in the other direction. The current list seems to be a combination of:

- Stronger-than-expected jobs- inflation sticky

- Manufacturing- inflation sticky

- CPI and PPI- inflation sticky

- Retail sales data- inflation sticky

- Earnings report stronger than forecasted- inflation sticky

- Israel Gaza conflict- international conflict

- Iran attack on Israel- international conflict

- Fear of attacks spreading throughout Middle East- international conflict

- Continued Russia Ukraine conflict- international conflict

These all suggest that inflation is sticky enough and economic growth is solid enough for the Fed to wait for more evidence before cutting its target rate. Both the 2-year and 10-year Treasury yields hit five-month highs in the last week. Good economic numbers, matched by a another decent start to first quarter (Q1) earnings season, should not be reasons for a sell-off. But sentiment left little cushion.

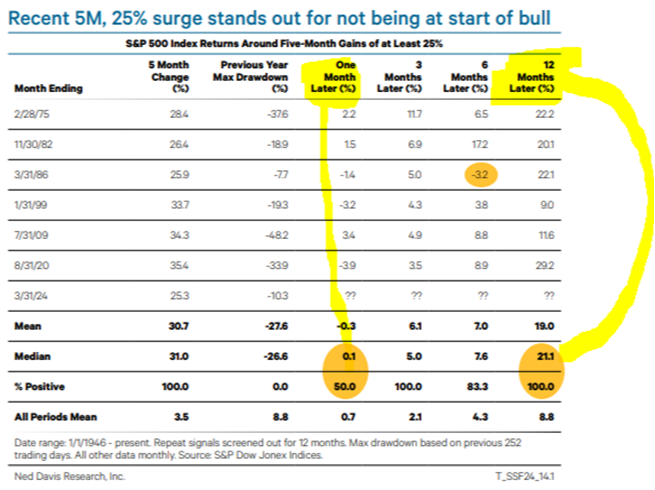

The ultimate reason for this special report is to provide proper and concrete perspective on the historical actions of the US equity market as referenced by the S&P 500 Index and more importantly, what has happened next. Before diving into the “why” of the pullback and index deterioration, a brief analysis of the recent rally is warranted. The S&P 500 Index surged 25.3% in the five months through March 31, only the seventh time the index has gained more than 25% over a five-month span since World War II. See the table below that shows each one, its magnitude and what happened one month, six months and one year afterwards:

Most of the previous dates are familiar to market historians, but I would not expect them to be familiar to most readers, hence please save this data table.

- February 1975 was only months after the brutal 1973-74 recession and bear market.

- November 1982 came a few months after the secular low.

- January 1999 followed the Asian Financial Crisis.

- July 2009 followed the Great Recession.

- August 2020 followed the COVID shutdowns.

The March 2024 case stands out for not following a cyclical bear market. The biggest drawdown in the previous year was 10.3%, driven by a spike in bond yields from July through October 2023. The only comparable case is March 1986. The most recent bear market ended in July 1984, and the drawdown over the previous year was 7.7%. Notably, the Fed cut rates 11 times from November 1984 to August 1986 and inflation was falling from multi-decade highs.

Forward returns were mixed one month later, suggesting the market was overbought after such big rallies. 6 and 12 months later, however, S&P 500 gains were well above the long-term averages. Again, 1986 is an outlier. It is the only case where the S&P 500 was down six months later. One year later, however, the index surged 22.1%, with a max drawdown of 9.4%. The study is a reminder that momentum surges rarely come near the end of bull markets.

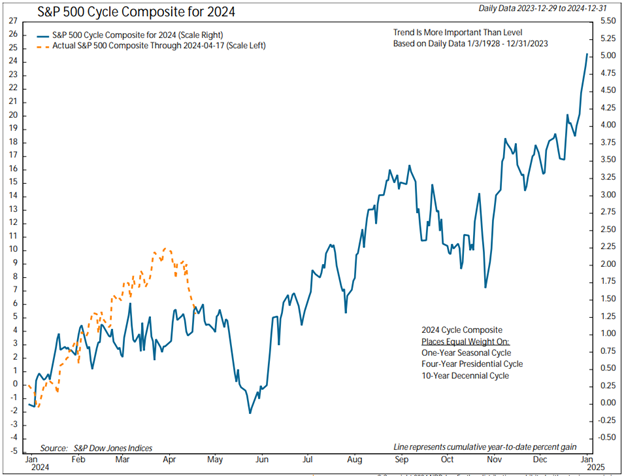

I will conclude with a revisit to the seasonal work that I often address, with the help of Ari Wald of Oppenheimer research and the date of NDR Research team. The consolidation “this time” comes at a time of the year when pullbacks have been common. The S&P 500 Cycle Composite below, as provided by NDR’s Research team, which combines the one year, four year Presidential, and 10-year cycles, shows a high being made on April 22. One reason (I believe) is that investors need funds to pay taxes. Unlike 2023, which reflected the declining markets of 2022, and hence not a lot of capital gains to account for, 2024 should reflect the nice gains of 2023. Investors had plenty of capital gains taxes to pay this tax season.

The history book for the current market action is yet to be written, but after such an expansive period of advance, I felt it helpful to provide perspective and historical data. Of course I will continue to monitor the markets, manicure portfolios and as always be available to address questions or concerns you may have about your individual situation. We are all different, with different needs at different times. DO NOT hesitate to reach out to us to help navigate any situation you are dealing with that we may not be privy to.

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

-

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.