US and global stock, bond, and currency markets were signaling that the US will soon be joining other central banks providing liquidity, until the tariff issue was largely relieved over the weekend. U.S. housing weakness, lower and medium wage consumerism, and the current international issues “are said” to be forcing the Fed to act. Powell clearly squashed this last week. Stocks are not waiting for the Fed to act; they are looking at the actions of other central banks and the data. Below is what we are seeing. Note that as I continue to explain in my weekly notes, that the markets may have been overvalued from an earnings standpoint, and this combined with the very difficult to handicap tariff tussle, both led to the spike down in the last couple of months. But now, we are almost right back to where we were!

Stock market trends over the past year. Data sourced from Bloomberg (2025).

Trump administration trade negotiations demonstrate more nuance and sophistication than feared since Liberation Day’s disastrous rollout. This has convinced investors that the Trump team will not inadvertently destroy the global economy. Then like a positive bomb drop, President Trump and Treasury Secretary Bessent came forward on Sunday and Monday morning and eased most fears by saying that China and US are coming to some good agreements. Since these are the two biggest economies of the world, if China and the US agree, then the rest of the world should simply fall in line. Future deals with other major allies like Japan may further assuage economic fears.

Below is the news flash from CNBC on Monday afternoon. What I believe is happening, that is very difficult for many to understand, is that President Trump (whether you like it or not) is a leader of shock and awe. He stated that he was imposing 145% tariffs on China. This weekend it was settled at 30%. Does anyone really know if he wanted 30% or 145% or ??? I believe that he basically said to China, “This is what we are trying to achieve. How we get there is really not so important to us. You can couch the discussion / negotiation any way you would like so that you can tell your constituency that you won in the negotiation. But at the end, this is what we need.”

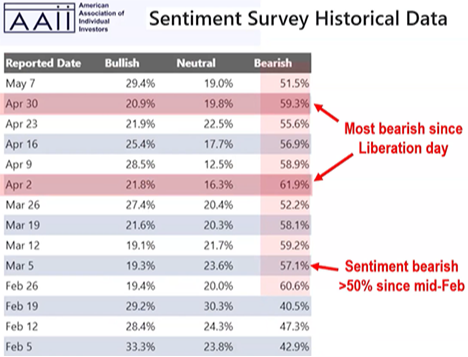

The best way to contextualize current events is to understand that the Trump administration believes it is working to address what it feels are threats to US economic interests and national security with rapid speed to keep opponents off balance and to create momentum. Threats to the US economic and security interests are well known. He style is not normal or what could be construed as “presidential,” but his intentions, according to the financial markets, seem to be working. The average investor is quite rattled by his tactics. If we simply look at how long the AAII investment survey has been negative, it has remained over 50% bearish since the beginning of March.

The central thing to keep front and center in evaluating the equity markets is that balancing these international issues with our domestic GDP growth is paramount. Strong nominal growth is essential given the escalating frictions internationally and the rising debt burden and interest costs, which now are eclipsing military spending.

The Trump administration is only too happy to change many things and quickly. The one constant among the destruction will be the need to keep the markets liquid and nominal GDP growing. Said differently, expect more liquidity and stimulus from both fiscal and monetary policy. If the Dollar falls further in response to US policy, it will act to boost GDP growth and tax receipts. Indeed, it will also reduce the purchasing power of consumers and investors. The US and global economy have structural imbalances and geopolitical risks. Investors will be best served by remembering that things that cannot go on forever will not. But the Fed’s work to make sure that we have a permissive monetary environment will always remain front and center so that we can easily adapt to the international.

Extremes can make the obscure more understandable. I do not think it will be favorable to be defensive or short US stocks in the current environment of structural changes, as structural imbalances are worked out, because nominal values will rise because financial repression and debasement are likely key drivers to solving the imbalances. Without a lot of fanfare, the first quarter earnings season has about come to an end. As of last Friday, 90% of US S&P 500 companies had declared earnings. Of these, profits are up 12.3% from a year earlier on 4.2% revenue growth. Sure doesn’t smell like a recession to me!

As seen above, pullbacks in the equity market earlier this year have mostly looked like “trims” or “haircuts.” Cover of the Business & Finance section on the Wall Street Journal, Monday, had an article titled, “Trade War Rattles Bond Market.” The bond market was rattled - meaning rates went up and bond prices went down, which means that the slowdown that was being baked in the cake is proving to not really come to pass. Instead, earnings and more advantageous trade incentives have almost single-handedly taken the term recession off the page.

Looking at the spread between the cost of high yield debt and US Treasury debt continues to decline, this also infers greater economic stability:

S&P 500. Data sourced from Bloomberg (2025).

Another major concern that has been bantered about is the concern of “stagflation.” Much like, but I believe worse than recession is an environment where prices rise and the economy struggles. This is stagflation. If we are to watch the Fed’s favorite inflation indicator, Core PCE, it can be seen that it was much cooler in March, and as such, prices are the lowest since March 2021. This is far from inflationary:

US Personal Consumption. Data sourced from Bloomberg (2025).

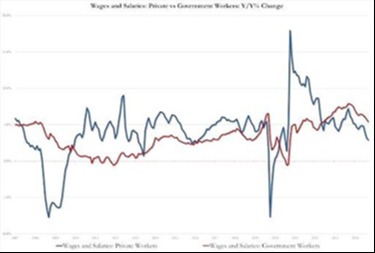

The Elon Musk brainchild, DOGE has also been helping. Since is has really only been in existence for a couple of months, the true long-term effect is yet to be known, but so far, public (Government) worker wages and salaries are up just 2.9%, and down from February to the lowest level since September 2020. As a comparison, during this same measurement period, private (non-Government) salaries were up 5.4%. This is more than double the public rise and again another factoid that does not align with fears of recession:

Wages and Salaries (Private vs. Government Workers). Data sourced from Bloomberg (2025).

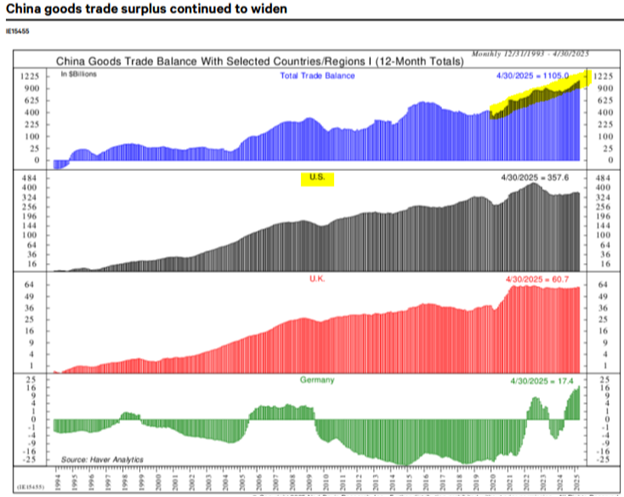

Even though I had expected that we would be able to work through trade tensions with China far better than they would be able to digest our lack of purchasing of their goods, I try and monitor changes in trade as I measure domestic economic measures. China’s exports rose more than expected despite hefty U.S. tariffs. China’s exports rose a more-than-expected 8.1% in April from a year earlier, just a modest slowdown from a 12.4% pace the month earlier. Imports were essentially unchanged, allowing China’s trade surplus to continue to balloon. In a month marked by tariffs of over 100%, Chinese exports to the U.S. plummeted 21% from a year earlier.

The decline in exports to the U.S. was more than offset by robust gains elsewhere, including 20%-plus gains in exports to Germany, India, and ASEAN. It’s possible that the exports to ASEAN (led by Vietnam, Indonesia, and Thailand) could be a means to bypass U.S. tariffs, indicating that growth could fade if high U.S. tariffs are imposed on those economies. Nonetheless, China has reduced its trade ties to the U.S. over the past decades, making the economy more resilient to tariff shocks. I wanted to provide a chart of this trade increase. Below I have separated China’s total trade, from US, UK and Germany so the graphic and consistent rise in US trade vs. the others could be seen. I don’t think that we will discontinue our trade with China, instead, I believe that we will slowly diversify away from China so that dependence is slowly alleviated.

China Goods Trade Balance over last 12 months. Data sourced from Bloomberg (2025).

In closing I want to be clear that we are noticing things happen at a pace I can’t ever remember seeing. I believe that Trump had spent the last 4 years getting everything lined up and therefore when he hit the ground running, he didn’t need to get up to speed on much of anything. I don’t say this to mean that I don’t find his methods particularly calm. From my chair, the equity, bond and currency markets seem to be OK with what he has been doing. I don’t ever relax on this thought, and I am continually watching for another unexpected shoe to drop.

Earnings have created a very good backdrop the unknowns of the future, and if interest rates and currencies remain range bound, we could be in a good place. As always, should something change that we feel is worth noting, we will certainly let you all know.

- Ken South, Tower 68 Financial Advisors, Newport Beach

-

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

Data sourced from Bloomberg (2025).

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.