Click HERE to watch on YouTube Click HERE to print PDF

Equity markets finally adjusted from their ascent last week, albeit by a small margin. The closing on Friday March 1st was a smidge higher than on March 8th, which was a whisker higher than last Friday. So tight in fact it almost makes the advance seem like it is moving in on week 21 vs. ending at week 19. As extended as this rally might seem, there are a couple of points that still speak to the health of the advance in the markets. The first is that there is clearly no break in the uptrend if one were to look at a picture of the NASDAQ COMPOSITE, it is still in a tight channel that is rising.

The second point I find much more interesting and "different this time." According to Thomas Lee of Fundstrat, in his recent meetings many of his institutional investors expressed extreme pessimism- still and therefore still hoarding large amounts of cash on the sidelines. See the chart below of the amount of cash on the sidelines since 2021 (post-COVID). Please note that on February 15, 2023, there was a total of $4.8 Trillion in all money market funds combined. And last week, even after the strong run up in equity prices, the balance now stands at $6.0 Trillion, up $1.2 Trillion.

One needs to ask the logical question, "If stocks are up quite substantially, and there had to be some cash coming off the sidelines to purchase stocks up higher, then where did the extra $1.2 Trillion come from?" In his view, and in ours, this is mostly a combination of interest income from short-term bonds and money markets which generated lots of dry powder. I feel it is helpful to show the simple math behind this growth in money market balances and interest earned based just on the amount in all money market funds numbers from last Friday.

- The average income on short-term instruments is approximately 5% interest.

- 5% of $6 Trillion dollars is $300 Billion.

- Based on last Friday's market closing valuation, the total value of all stocks combined in the S&P 500 is approximately $40 Trillion.

- $300 Billion is 1% of $40 Trillion.

- If just the interest from the cash on the sidelines were to be invested, this represents more fuel in the index's tank!

Now let's take a moment and go back to historical, statistical data of market action. I posed the question of what markets typically do when the markets are higher the previous year and have a strong January. I was able to put these “what ifs” in a table. This is a table that I located last week.

- If the previous year the market is up greater than 15%.

- This is followed by a positive January.

- The markets (since 1950) were up 100% of the time in the first half of the year, 85% of the time in the second half, and for the full year up 92% of the time! for an average return of 16.3%! This is really quite a strong performance given how good 2023 was.

I thought it was interesting to show what the annual return was in these 12 of 13 instances as well. But also, if one is to prognosticate based on this historical precedent, the base case for the S&P 500 could be a strong number as well:

Presidential Posturing Begins

The next point that I wanted to bring up is some of the rumbling that is starting to go on about what the presidential candidates are going to say about their respective platforms. Three points that are some of the most important are:

- Medicare costs.

- Social Security benefits.

- Income taxes to individuals and corporations.

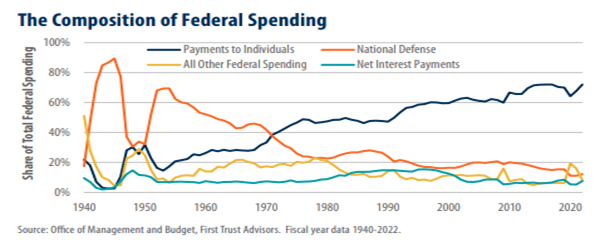

The one that I am going to focus on for a moment is Medicare costs. On page A4 of the March 12th Wall Street Journal, there was an article titled, "Plan to Shore Up Medicare Revised." It references what Biden supposedly would do with taxes to fund the increases in Medicare costs, but most importantly, shows that Biden is looking to strengthen his sponsorship with the voters that are Medicare recipients. There is also Biden’s proposal called a budget, where he proposes $7 Trillion in new taxes. The article states that this is Biden's attempt to "throw down a marker" on a sensitive political issue for the fall election. I bring this one up as I found a quite startling chart from the Office of Management and Budget for the fiscal year data going all the way back to 1940. Note that National Defense, Net Interest Payments, and All Other Federal Spending is basically flat as a share of total spending, but Payments to Individuals continues to rise.

In the end, candidates will not talk about difficult issues or will talk up their opinion on issues that will gain voter sponsorship, but the fact remains, whoever is elected in November they will be forced to deal with these three demons listed above. I don't bring this up to cast cold water on things, but there could be a somewhat silver lining. As I see it, once the new President is elected, they will begin to do the heavy lifting of changing the cost of Medicare, extending the age to begin taking Social Security benefits, probably increase the taxation of the benefits, and raise taxes to individuals and corporations. The silver lining to all this is that this could cause somewhat of a slowing of the overall economy, not a recession, but a slowdown. Along with that slowdown could be lower inflation and interest rates. As we all know, the level of the national debt and the amount of interest expense that goes along with it continues to be the growing elephant in the room.

In closing, I thought I would go over how the economy and the markets sit currently as I see it:

- Earnings- the last earnings report beat expectations by 78% of the companies, this is a good thing.

- Fed- although the CPI and PPI are too strong to let them ease now, they are focused on dovish activity when the indicators permit.

- Valuation- if we remove the Magnificent Seven FAANG stocks, the S&P 500 is trading at around 15.8X earnings, not overvalued. If the Magnificent Seven are included, the number jumps to 31X.

- Technical Market Action- Small-Cap and Equal Weighted S&P are coming out of their slumber and showing increased breadth.

- Flows of Capital- as I referenced above, lots of dry powder to buy up the market and move off the sidelines.

- Sentiment- many media prognosticators are calling the need for a top. Virtually nobody stating the market should go higher. Great contrarian indicator.

The market is still due for the digestion I keep talking about. Mark Newton, the technician of Fundstrat, still feels relatively confident that late March into early April we could see the market digestion we have been speaking of since early February. Whether it is a decline or a sideways consolidation that achieves this pause to refresh is yet to be seen. We will be paying attention and are here to answer any questions you may have about your individual situation or any changes you would like us to address in your personal situation.

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

-

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.