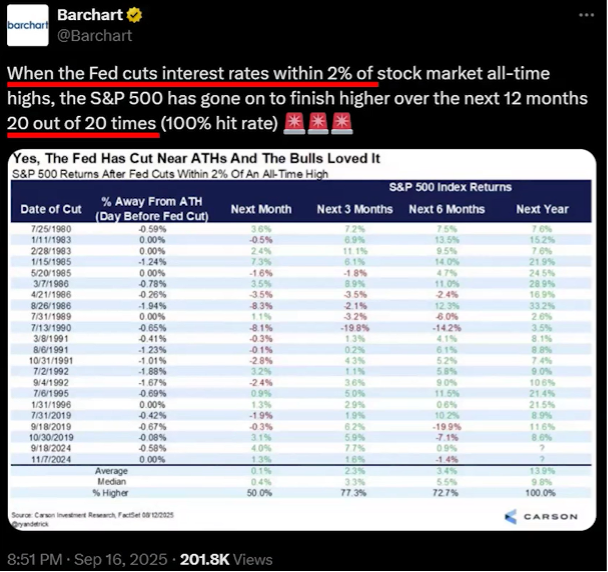

The Fed made a dovish cut Wednesday of 25bp, dovish because to us, this is the start of an easing cycle rather than “one and done.” There are many who are wondering how this could be positive for stocks, but we see multiple reasons this is positive for equities.

Foremost, as I’ve been saying for weeks, we see several benefits from easing:

Fed is boosting monetary liquidity, which is good for asset prices: If interest rates are cut by the Fed, it decreases interest rates on short-term funds to business. This is the money used to finance manufacturing, production, and inventory. If it is cheaper, then profit margins are immediately enhanced.

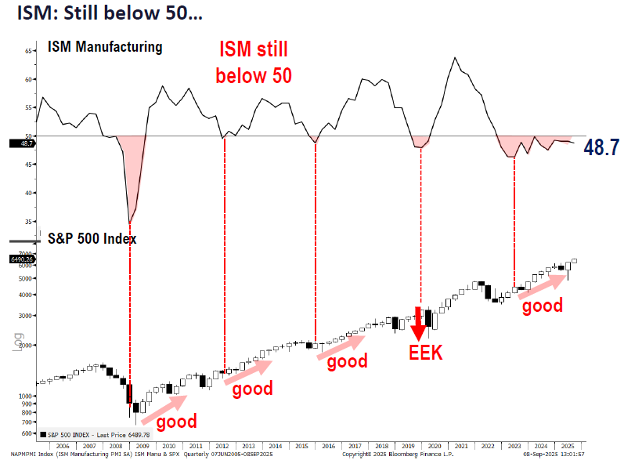

Fed cut likely boosts CEO and business confidence, allowing ISM to move >50: an ISM over 50 is a sign of business expansion. As can be seen below, the ISM has been under 50 for some time and if the markets respond as they have in the past, this could lead to a further melt-up in

Higher biz activity means improved hiring, which Fed would like to see:given that the stated reason for the rate cut was an expected decline in labor and hiring, if business improves due to the rate cut last week and the expected cuts in the rest of this year, hiring could stabilize and the employment picture should improve.

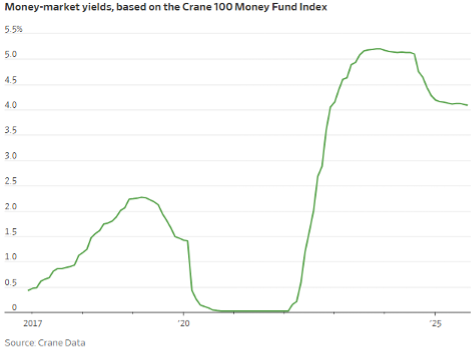

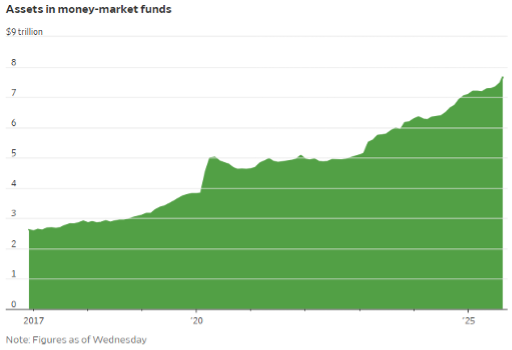

Fed is making cash less attractive, which is risk-on:this is one of the most important points of the cut. The Wall Street Journal started the week with what I believe is one of the most important current facts that almost nobody is talking about. U.S. investors are sitting on a pile of cash. Even with rates now coming down, many are in no rush to move it. Assets in money-market funds reached a record $7.7 trillion last week, with more than $60 billion flowing into those funds during the first four days of the month, according to Crane Data, an industry researcher. That is unlikely to change soon, even with the Fed now cutting rates. Money funds are still yielding a lot more than what they had in the 2010s and early 2020s, when the Great Financial Crisis and then the Covid pandemic pushed rates to ultra-low levels.

I want to note that the press (with clearly liberal bias) chooses to blame it on the crisis’s themselves rather than on the administrations that helicoptered copious amounts of cash into the hands of US citizens. This has created a level of money sitting on sidelines almost beyond comprehension, but also so much that at the current 4% interest rate grows by almost $400 Billion per year creating an amount of money that desperately needs a home in addition to the money markets that it currently resides. The path of least resistance has shown itself in the price of US Equities, gold & silver, and crypto currencies. With stocks by some measures, now more expensive than ever, some investors are willing to wait for discounts. And it will take more than one (or two or three) rate cuts to change their minds. Here is an illustration of where yields on cash were and where they are currently followed by the clear and unabated rise in money fund balances. Note that even though the Fed cut rates last week, the current yield still sits at very attractive levels compared to the last ten years.

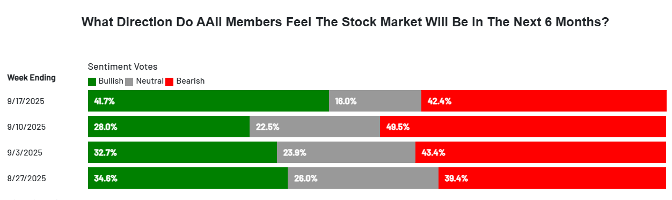

It seems as though it has been a waiting game for the last month to two. Looking historically at August and September, this tends to be the toughest part of the year for the equity markets. There have been a variety of reasons, but “this time” it seems to be centered around the fact that the markets have been moving consistently higher since the Tariff Tussle in April and therefore is thought to be in desperate need of a correction / digestion. As the market has continued to just gurgle higher and higher, the American Association of Individual Investor sentiment poll shows that the individual investor is unwavering from a negative opinion. Here are the numbers going back for the last few weeks as the markets have continued to hit all-time highs, even before the Fed decision:

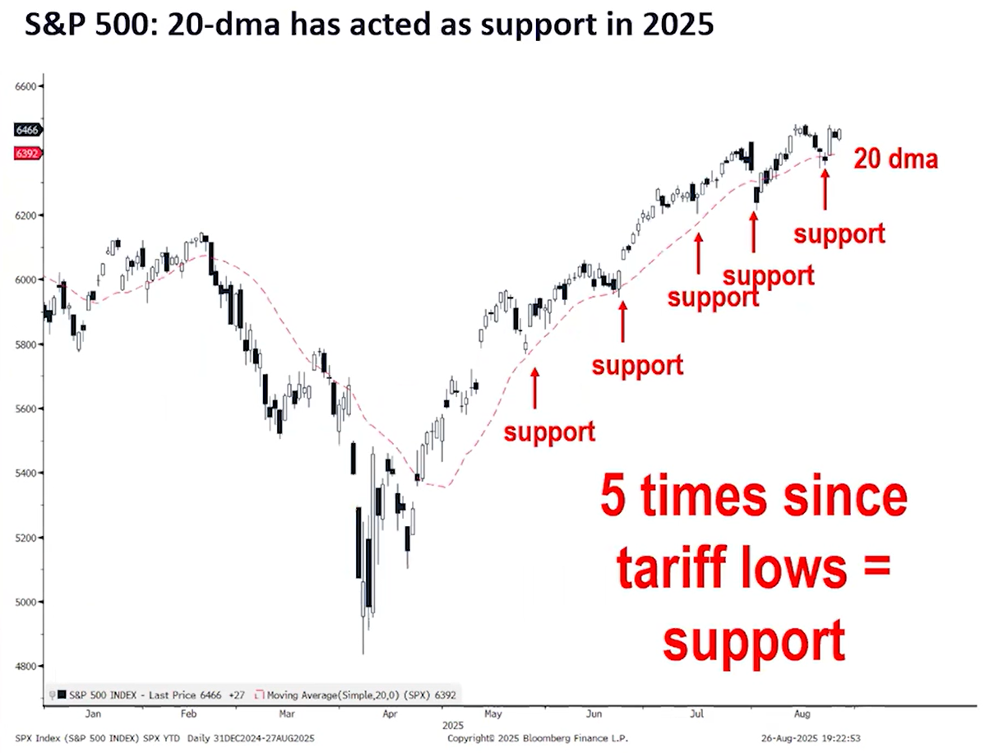

Every time the market has even attempted a decline, it has found support and continued higher. There have been five recognizable times that this has happened since the April low:

What is frustrating many of those looking for the correction is that the current market looks even better than it did at the beginning of 2025! There have been many bombs dropped on the US equity market since COVID in 2020, and 2025 has not been lacking in the least. These are the major issues that have been shrugged off by the markets:

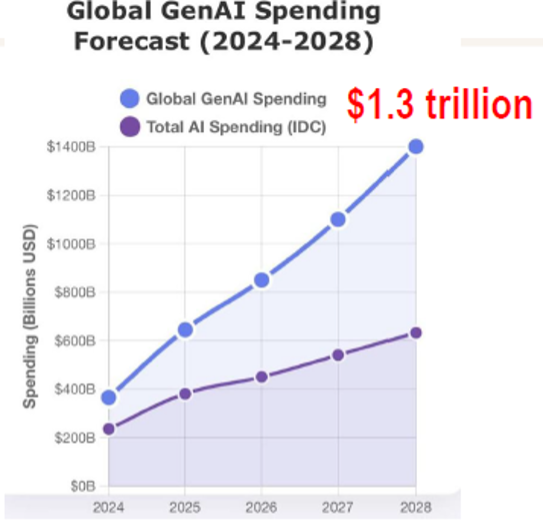

So many investors are looking for what to do “right now” rather than what has the best runway it seems. Since these negative media induced points seem to be large and meaty with lots of stuff to chew on. If one is to look beyond the surface level of the negative connotations, it is clear more often than not that these are nothing more than many things that the media needs to retain readers and listeners. One point that is strong and growing that the media has basically almost quit mentioning is the growth and benefits of AI. Since technology seems to be the overwhelming thing that is continuing to drive increased profitability, AI is at the epicenter of this. According to IDC, AI spending is in the early innings. This is what they forecast for AI spend going forward:

All industries benefit from increased efficiency. Many are concerned that AI will erase much of the labor force, but I believe that much like historical technology changes business is resilient and labor will simply be displaced into other areas.

Ever since the stock market collapsed around “Liberation Day” back in April (which now feels like a distant memory), it has faced a number of hurdles and challenges on it way higher. It has surpassed each one of these in short order as illustrated above. Last week was sort of a culmination of all that. It was a key test for stocks, both from the Federal Reserve making official the rate cuts that had been priced in for weeks and then the high volume “quadruple witching” session on Friday. In each instance, the market not only took the tests in stride, but seemingly aced them once again.

There is a slight caveat to the ostensibly unstoppable stock market. The major indices are not entirely “the market” even though they are often used interchangeably for it. When we look at the internal data for the broad market from day to day, the action over the past week was surprisingly lukewarm. Despite this lackluster breadth, last week unexpectedly produced very little volatility aside from the hour immediately following the Fed policy announcement on Wednesday. So, we entered this week once again without any distinguishable change in recent status quo. As I have been stating in the last few months, the longer this melt-up continues the odds of getting a better buying opportunity in the days to weeks ahead are better than average. But….. if what you own ain’t broken, no reason to fix it! Stick with the winners, and if there is a better opportunity that comes around, then get rid of what is least good and take advantage of other opportunities.

- Ken South, Tower 68 Financial Advisors, Newport Beach

-

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The S&P 500 is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States. Indexes are unmanaged and cannot be invested in directly.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

Data sourced from Bloomberg (2025).

Stock investing includes risks, including fluctuating prices and loss of principal.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Bonds are subject to availability, change in price, call features and credit risk.

Government bonds are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

Bond yields are subject to change. Certain call or special redemption features may exist which could impact yield.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor’s portfolio. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

LPL Tracking #800910