The turkeys of the market this week seem to be the giant technology companies of the year. They stair stepped higher all year and finally they appear to be giving up a bit of their advance to the laggards. As of Monday, 95% of the companies in the S&P 500 had released their Q3 earnings and the results were spectacular. The results show a robust third quarter for sure. Profits for the quarter were up 8.2% from a year earlier on 5.1% revenue growth.

We can continue to talk about the election, about who President elect Trump is placing in important roles in his new administration, and more interestingly the Musk / Ramaswami duo that is sure to do all in its power to recommend how to decrease spending in the US Government, but at the end of the day it is really all about earnings, earnings, earnings.

Markets love a clean sweep. With near certainty, it appears that the U.S. Republican Party has gotten a clean sweep of the executive branch and both the House and Senate in the November elections. With that could come sweeping change, including tax cuts. As Ed Clissold has shown in the NDR election outlook, a Republican clean sweep has historically been the next-best scenario for equities (after a Democratic president and split Congress). This is likely because tax cuts and deregulation, key positions of the Republican party, are market and business friendly.

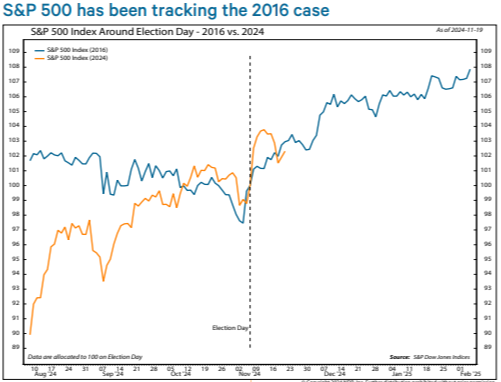

What I want to also focus on is how our economy and incoming party change is reflected in the US Dollar and how our stock market is performing relative to foreign and emerging stock markets. The US Dollar has been unbelievably strong. This infers that massive amounts of capital are flowing into the US from outside our borders, inferring that our US economy is going to get even stronger. I find it important to look at a comparison of the US market today vs. the US market in 2016. This is more important than normal as we had a previous 4 years with Donald Trump as president and we know how he operated then and quite possibly his actions to come should rhyme with his past economic policies. Below is a picture of the current market overlayed on the 2016 market since August. If this coming year should prove to be anything similar, the stage could be set for a further continuation of the rally the S&P 500 started in October of 2022.

Many seem to wonder how there can possibly be enough fuel to send our markets higher, but I believe that a good percentage is coming and could continue to come from foreign investors. As I had said earlier about how the economic growth must exist and provide a foundational backdrop to a market so it may go higher, I believe that an analysis of how the foreign economies and doing, and how they are doing relative to the US economy to give an even more graphic confirmation of why investors from the Eurozone might be investing in the US markets. As can be seen from the Composite Purchasing Managers Index from late 2021 till the end of November of this year, the Eurozone is actually contracting and ours is expanding and beginning to accelerate.

Record net capital inflows

Foreign investors are still interested in the U.S. Net international capital inflows totaled a record $398 billion in September 5.5x more than the 12-month average. The fourth largest purchase of bonds and the second largest purchase of stocks led to a record increase of purchases of long-term U.S. securities. Subtract $47 billion of U.S. purchases of foreign securities and you end up with a net inflow of $216 billion. Add in net inflows to short-term cash equivalents and bank liabilities and you will nearly double the total! I think we can assume that foreign investors could have been sitting and waiting for the election outcome and they seem to be giving us their opinion with the action of their wallets.

The negative offshoot of this continuing and increasing economic growth could unfortunately also include rises in US domestic inflation expectations. The bond market seems resigned to the fact that inflation expectations will settle at a level above the Fed’s target rate of 2%. In Barron's this past weekend, the interview for the week was with a past Fed member. He also confirmed this point. The Fed is lucky. It could be worse. Long-time readers know that rising inflation expectations have been my biggest intermediate-term concern.

After an expected slowdown (which never materialized), I was concerned that if the Fed didn’t get inflation back to target, investors would become disillusioned that it would ever do so and demand a higher term premium. Now with a potential reacceleration of economic activity, the risk of inflation expectations becoming unanchored is real. Although inflation expectations have moved up from their September lows, they still remain below 2.8%. I add this to the list of reasons why the Boo Birds kept on calling for a market decline in 2024. Here is their list of reasons why the market should have gone down this year:

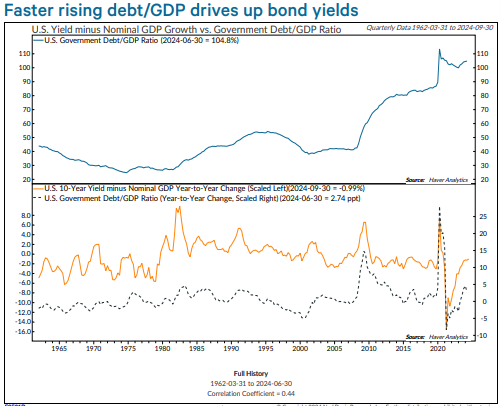

Even though the stock market has cheered the election of Donald Trump as the 47th President of the United States, the bond market has been less than gleeful. The 10-year Treasury yield jumped after the election, extending its upward trend of the past couple of months. On Friday it had just kissed 4.5%, the highest level since July. It reflects legitimate worries about the path of government spending and what that could mean for inflation. As we discussed several months ago, Trump’s policy proposals, including tax cuts, sweeping tariffs, and deportation of undocumented immigrants, would amount to a significant bump in the government’s budget deficit and debt. The nonpartisan Committee for a Responsible Federal Budget (CRFB) estimates that Trump’s plan would add $7.75 trillion to an already bloated outstanding government debt, which exceeds $35 trillion. The new deficit spending would likely boost economic growth in the near term. But since the economy is already operating close to potential, spending would also likely be inflationary. The argument against this is that the decrease in the size of government and the increase in tax revenues due to a booming economy could offset this. This will certainly be fun to watch!

Higher bond yields over time

Debt-to-GDP in the coming years will also likely rise. Despite selling an image of fiscal conservatism, government debt has increased more with a Republican in the White House than with a Democrat, regardless of the makeup of Congress. Historically, debt-to-GDP has run up the most during a Republican presidency with a split Congress. But even in a GOP sweep, odds are that debt-to-GDP will continue to creep up. We expect this to keep upward pressure on long-term government bond yields. The chart at left sums up the potential impact of the expected fiscal expansion on bond yields. Historically, the acceleration in debt-to-GDP growth has been associated with an increase in the gap between the 10-year Treasury yield and nominal GDP growth. In other words, when debt grows faster than the economy, bond yields tend to rise as well. While the increase in yields so far has not been a drag on the cyclical bull market in equities, the risk remains that further and faster runup in yields may cause equities to stumble.

My Other Concern

With this backdrop, now that interest rates are rising, am I more concerned about valuations? The short answer is, yes.The truth is always more nuanced than a simple yes or no. Interest rates have not yet hit critical levels, based on the level and speed of ascent that have derailed stock market rallies in the past.Inversely, the Fed easing cycle puts short-term interest rates on track to being less competitive versus stocks. Finally, a big question for 2025 is whether the stock market can grow out of its valuation problems via earnings growth. When it comes to interest rates and stocks, speed matters, especially when rates are coming from low levels, and the recent spike in bond yields is threatening to be a bigger problem for the bulls. I believe this is part of the reason why the market seemed to hit sort of a flat spot after its initial post-election rise. Bond yields have not risen quickly enough to threaten the rally, but if they do not reverse or even stop rising, they could soon.

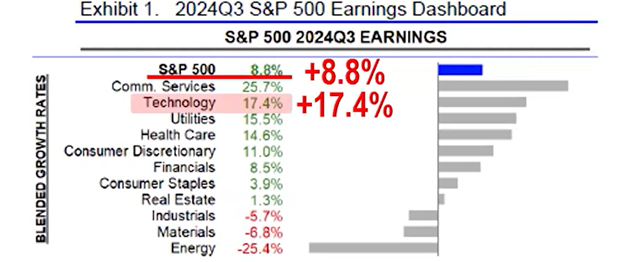

The ultimate elixir for high valuations due to high prices is earnings growth. S&P 500 EPS growth has been accelerating all year:

I am showing this as it means that each quarter the growth rate has been faster than the previous quarter. When earnings growth has been accelerating rapidly, as it is currently, the S&P 500 has risen at a faster pace than its long-term average. This explains how the S&P 500 has gained close to 30% year to date despite elevated valuations. Earnings growth could slow in 2025, as the mega-caps that have driven the earnings acceleration struggle with tougher comparisons. If the rest of the market does not pick up the slack, valuation risks could come to the forefront. If this week is any indication, this broadening of the market seems to be buoying indexes even though the air in the balloon seems to be coming out of the Magnificent seven a bit.

This Thanksgiving we have much for which to be grateful. Cooperative markets, a constructive earnings trajectory, prescient commentaries, and thoughtful, appreciative investment partners like yourself! Wishing you and yours a festive Thanksgiving and a strong finish to 2024!

- Ken South, Newport Beach Financial Advisor

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.