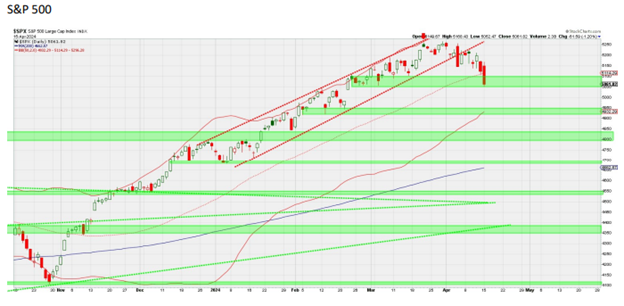

To say that it is infuriating reading about all the government spending, and the United States financing of external causes, is an understatement. This is only exemplified by the amount of taxes that we must pay and particularly what we deal with in the lovely state of California! How ‘bout those gas prices! OK, enough about that. I start almost every note with some reminder of the amount of gain that has been experiencing this far in US equity markets (almost unabated) and that I am expecting some level of pullback / digestion. Well, we may be experiencing it as I pen this note. I have gone on to say, for many reasons, that I expect this to be just a pause for the markets and not a significant decline. Well, we are around 5% from the highs of March 28th at 5,264 on the S&P 500. There are a number of subjects that I want to cover, but I think that the subject that is most prescient on the minds of investors is whether this is a digestion or the beginning of a more substantial decline. Here is where we are, with a green bar at different levels of support on the downside. These green bars represent likely places where buying could begin kicking in. The unfortunate thing is that going up tends to be a staircase and going down tends to be more of an elevator. As can be seen below, this has really been an almost straight up staircase since the end of October last year.

Last week the Dow Jones Industrial Average closed below its 50-day moving average while the Dow Jones Transports broke below their 200-day moving average. The result is two pretty ugly looking chart patterns on a short-term basis. Longer-term, I do not think this is a problem, but in the short-term my cautionary stance on stocks of roughly a month ago, while a bit premature, was clearly reinforced last week. While there were a number of reasons offered for the stock slide, I think the real reason was really a combination of these three major unknowns:

1) Middle East- Iran responded to the Israeli attack on their embassy in Syria. The response was breathlessly anticipated and thought likely to ignite further escalation in the region. Iran’s retaliatory attack was surprisingly muted, drones and missiles but plenty of warning so targets could be evacuated etc. Iran has declared the response finished. This could clearly flare up again, but since the warning came out last week selling into the weekend was a logical action.

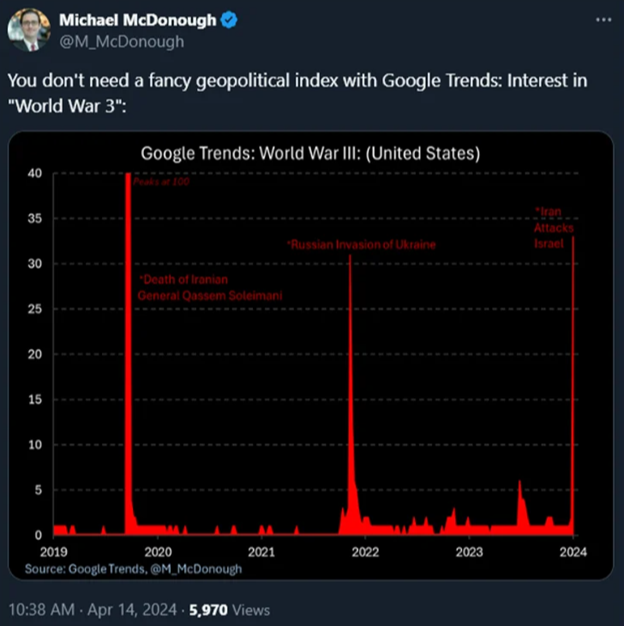

2) Conflict Translates- into greater conflict and fear of a global confrontation. This is due to China, Russia and Iran being joined and all collectively anti-US Dollar, further escalating the friction of global conflict. In looking at Google searches for World War III, there are more fear searches this last weekend then there were during the Russian invasion of the Ukraine. Below I show a graph of these Google searches going back to the death of the Iranian General in late 2019:

3) Tax Day- Since Monday was April the 15th (hence today’s title), taxpayers must pay taxes owed to avoid penalties even though they can file extensions that can carry them all the way out to October.

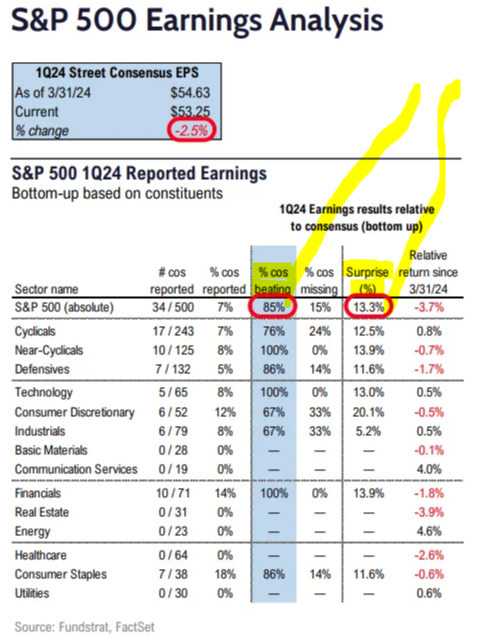

4) Economic Strength- that translates into interest rates being higher for longer. Last Wednesday was a strong CPI, followed by a firm PPI on Thursday, and then Monday of this week retail sales were particularly strong coming in up .7% vs. the expectation of up .4%. On top of this earnings are already coming in full steam ahead. I have included a chart of earnings reports thus far below. But it should be understood that these all lead to higher interest rates. The higher rates on the 10-year really broke higher on Monday when the rate broke above 4.6%, up almost 3% for the day.

I am attaching a link to this blog post on our website of how to understand earnings season and how to read earning reports. This is from FundStrat, and I found it particularly good and quite easy to follow for those interested:

https://fsinsight.com/academy/earnings-season-and-financial-earnings-reports-explained/

Even though the economic reports and earrings reports have been strong and not showing signs of abating, it must be remembered that inflation reports as well as earnings reports are backward looking. They represent what HAPPENED, not what is GOING TO HAPPEN. I found it particularly interesting that in the Wall Street Journal, they put a daily comic strip in that I found particularly fitting this past Friday:

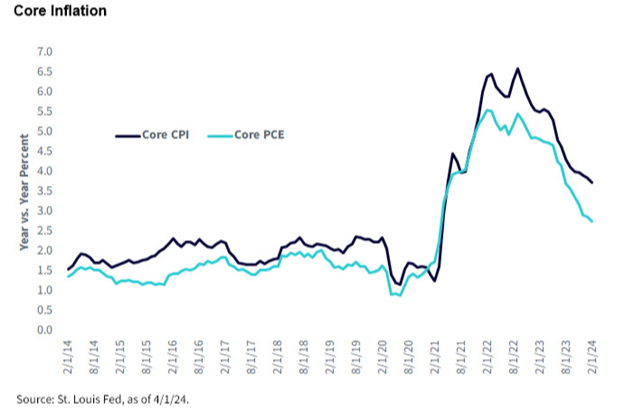

What I think is the clearest depiction of this is the core inflation as evidenced by the Core CPI and Core PCE. Since much of our economy is consumption based, consumer prices and prices in general tend to be indicative of what is happening with prices. As can be seen below, although core inflation is not down to the Fed’s target rate of 2% since their high point in the beginning of 2022 they are clearly on the decline.

It could very well be that we are at the tail end of the inflationary growth reports from the US economy. If this is the case, then this could be the final push higher for interest rates and in doing so the correlative action to the short-term decline in the US equity markets prior to their expected second half rally expectations into the end of the year.

I want to take a bit more time and touch on the new conflict in the Middle East, and its timing. We are facing a moment of dual fragility for equities. We don’t think stocks will fail this test. The two important factors as I see it are how broad is this Iran-Israel conflict going to be and what will the Fed do if it does in fact spiral further. At this time, one cannot tell what can be expected to be Israel’s response to the Iran attack. As shown above, there has been a huge increase in tweets and Google searches about World War III and Stock Market Crash, so investors are bracing for the worst. And reasonably, it would be expected that many investors would de-risk in the face of Iran-Israel and the specter of a broader conflict. We are more concerned with the duration of the ongoing US military support in multiple theaters which may require incremental fiscal outlays. The first indicator that I watch is the price of oil. If the global markets truly think there is a conflict that is expanding, oil should rise to the $100 per barrel range. Instead, what we saw on Monday was a blow off in both the price of oil and the price of gold.

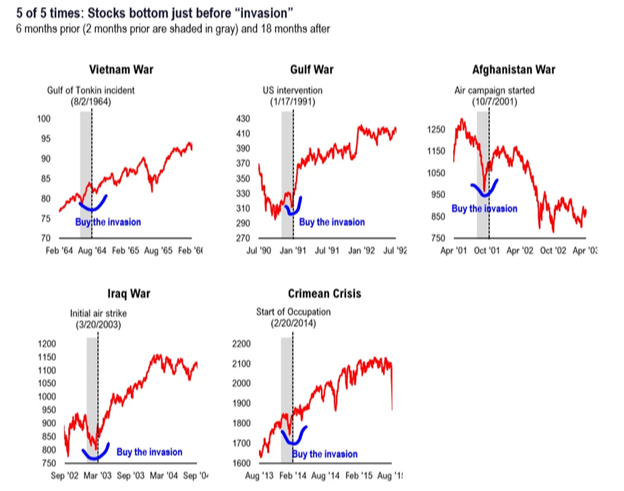

To give some color to how the markets have behaved after previous conflicts, Thomas Lee of FundStrat put together a great table of charts showing major conflicts back to the Vietnam War back in 1964. Although the initial fear action is a quick exit, these quick fear actions tend to be quite temporary. More important is the overall economy.

In closing, I would like to stress once again that the stressful period that we are all experiencing with domestic politics, international conflicts, Tax Day, and short-term market declines are nothing abnormal. It is part of the process. None of these events are fun, but they are part of life, and we need to make sure we adapt to them and drill down and focus on our own individual situations. This is why I put together these weekly notes. Please, please, take the time to think about yourself- selfishly, and make sure that you are saving as you should, taking care of yourself, your health, and your family as you should and if there is anything at all that we can do to help, please don’t hesitate to reach out and ask us for our input and suggestions.

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

-

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.