I’m not a big baseball fan, but I had to take a pause when I saw that Otani was signing a contract for $700 million over a 10-year period. I mean, what does the team have to charge for a seat, a hotdog, and a beer if they are paying players this much! To repeat a very common phrase, “We live in unprecedented times.” Since the COVID pandemic, the economy has been deeply influenced by a massive increase in government spending, COVID-related shutdowns, and a huge increase in the money supply. In all our years of economic forecasting, the task of identifying where we are and where we are heading has never been so difficult. To try and apply conventional rules and expectations after a 42% increase in money supply is quite difficult. Now more than ever, it is important to follow real-time data on the economy. To rely on 10-year historical data seems almost irrelevant as the landscape is so completely different.

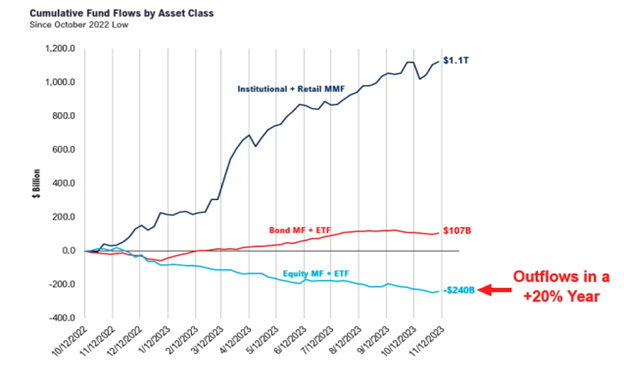

Every week I bring to you charts and tables that make me think. They make me wonder where there is an advantage. They make me wonder when to be cautious and when to be on offense. The chart below is a repeat of what I had in last week’s letter, but I feel it to be incredibly important. This year, even though it has been one of the best performance years for the S&P 500 (currently moving in on +20% for the year), there has been a mass exodus out of stocks and into cash and short-term US Treasury instruments. Even bonds, where higher interest rates than have been enjoyed for many years aren’t getting the attention they probably deserve. I mean I get the fact that bond investors have lost money for three years and this has never happened before in history! But, if the economy is going to either go into a recession or a soft landing, aren’t rates almost certainly going to go down? And if they do go down, are current rates even more attractive? So here is the picture of what investment capital has done since October of 2022:

If any of the money that is in the MMF category in the above graph goes into US Equities and ETFs, imagine what could happen next year to returns on investment. One of the cautions that I keep hearing is that of consumer debt and the level of defaults on credit card debt, personal loans, and car loans. Here is the chart since 1980. Remember, 1980 is right before interest rates hit their high point. Note that the ultimate low point was when the $5.5 Trillion was dumped on the US economy and our money supply ballooned by 42%. Since every man, woman, dog and cat got free money, clearly defaults were at a low point. Since that time leverage has increased, but not at a level that appears to really be showing consumers as in dire straits:

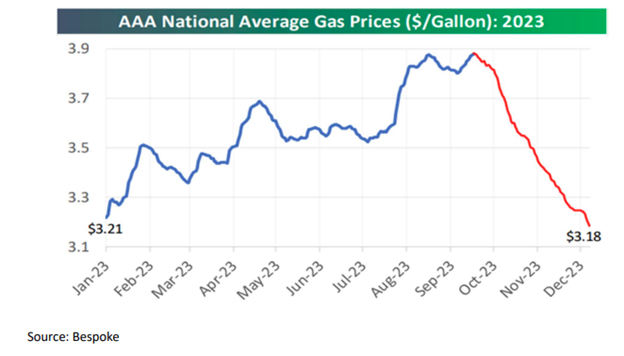

The next two charts I want to show are that of the two most important costs to most every citizen. The first one is that of interest rates. It took from December of 2021 to November of 2023 for the 10-year US Treasury to go from 1.5% to 5% (basically two years). In a matter of 4 weeks this rate has dropped from 5% to almost 4%. This is without any change in the interest rate policy of the Federal Reserve. Hence, the cost of mortgages, if they were to respond with equal speed would have dropped by almost 20%. This is huge. The other major cost is gasoline. Note that there has been no commentary in the media about this one. From $3.90 a gallon on the National average to $3.18. Again, in a little over 4 weeks! This is a decline of almost 20% as well. And where do you think this disposable income of the average consumer is going to go? They are going to spend it!

Again, I think both of these add to the possibility that the consumer could drive equity prices higher. So, this makes me take a moment and look at what the FactSet estimates for earnings are for 2024. I took the time to look at what was being forecasted for 2024 6 months ago, then 3 months ago and what the current expectations are. Needless to say, for the S&P 500, Japan, the Pacific region ex-Japan, and the MSCI Emerging Markets the earnings estimates keep rising.

Markets don’t tend to develop a downtrend when earnings are being ratcheted higher. See below:

I then took some time to check in with Ari Wald of Oppenheimer. According to Ari’s OPCO Bullish Composite, an aggregate of four popular investor surveys, the composite has increased to 67% from 41% since the start of November. Ari’s analysis shows:

- optimism has not reached the extremes that have historically limited bull market activity, and

- broader participation readings are an offsetting positive. Since 1994, forward S&P returns haven’t turned below-average until four-week sentiment readings are above 80%.

- In addition, forward S&P returns are slightly above-average when sentiment is above 60% and the percentage of NYSE stocks above their 200-day average is also above 60% (currently 57%).

It’ll therefore be important that internal breadth broadens further over the coming weeks. This is what we will be paying attention to. Remember last week I showed that Thomas Lee of FundStrat expected the markets to have some digestion difficulty in the first couple of weeks of December but expected them to end the year firmly. It is beginning to appear that maybe the fear of missing out (FOMO) of a good year-end finish is enough that many investors are broadening out their holdings and making sure that they are in so that they don’t miss out.

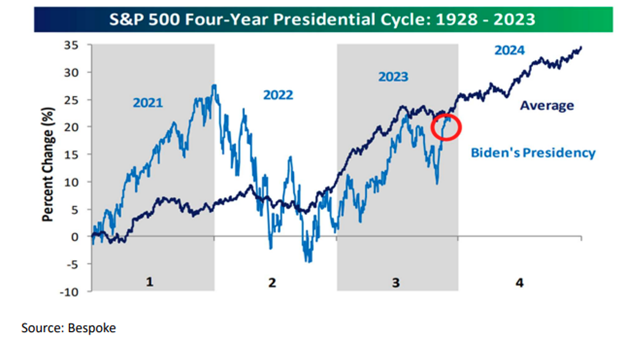

This brings me to my last chart for you to study. This is the chart showing the Four-Year Presidential Cycle going all the way back to 1928. I’ve taken the liberty of putting a red circle right at where we are currently. As can be seen, if history is any precedent, we could be ready for a continuation of the performance of 2023. This would be happening in the face of numerous news reports asserting that we are at best going to slow down into an economic soft landing, and at worst a full-blown recession once the ether of the massive stimulus money burns off and there is supposedly no money left to buy with.

In closing, I take some time to read the comic strip in the Wall Street Journal every day. Most of the time I am not particularly amused, but I saw this one last week and found it to be enough to generate a chuckle. But again, I find it indicative of the mood of the investing public. A mood that says that hope is not particularly prevalent, no matter how many facts seem to exist to the contrary.

We hope that you have got most of your Christmas shopping done and, if you are being more nice than naughty, that maybe there might be something nice under the tree for you!

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.