For the last number of weeks, I have been writing to be prepared for the feared seasonal correction / digestion. As of yet, it just has not happened. The media has continued to expound on the point that the fuel that they say would be "necessary" to get the market to its new highs would be the Fed lowering interest rates. Well, no such luck here as the economic indicators and fourth quarter earnings showed little weakness. And weakness is the necessity that the Fed would need to begin lowering rates.

I have been preparing for this possible digestion period by watching all indexes, interest rates, the US Dollar and commodities, waiting for signs of weakness to show their hands but again no such thing has happened. Therefore, I keep "watering my flowers, looking for weeds to pull." At this point, I have noticed that big-cap tech continues to lead and extend its lead, but at the same time the second tier of industrials, financial services, and discount / specialty retailers have clicked into gear and are exhibiting strength. This is super important as the healthiest thing a market can do is continue the leadership it has and begin to expand the leadership into other sectors. Ari Wald, Chief Technical Analyst of Oppenheimer said it best this last weekend, "Worry about the weak not the strong." If the market is showing consistency in its advance, be concerned when this advance falters. But if the advance isn't faltering, then focus on the weakest sectors and companies as they should continue to be weak. Market pundits fretful about overbought conditions often miss the bulk of an advance because overbought conditions are a function of a bull market. In addition, they tend to recommend stocks / sectors that haven't worked, whereas we see relative risk in relative weakness. I've often tried to explain to clients who have felt that the market has gotten away from them and therefore they don't want to invest in the leaders that if the leaders were to digest their move, the laggards would decline miserably as well. I explain that to rotate into the cheapness of smaller and medium companies is usually a statement that if these smaller companies are cheap, then the leaders most likely aren't that expensive!

Below I want you to really look at this chart. In having discussions with people, many say that they are happy that their holdings / accounts are "finally" above where they were in November of 2021. Now think about this. If they are just now seeing things above where they were two years ago, then this market is just now breaking out. The market has actually spent this entire time building up its energy for its next move. If this is the beginning of a two-year breakout (as Ari was quick to mention), then this new advance is really only one month old! Ponder this one.

To give an update of what the S&P 500 has done since the end of the 2022 decline, and how the current advance looks relative to the previous two legs, here is an update of last week’s chart. I add this as I believe that spatiality and scope is important to understand why I have been expecting some sort of a digestive phase consistent with the normally tired March-May period.

I sort of stole my title this week from the article in Barron's by Ben Levisohn in Up & Down Wall Street, Ben starts by saying, "This stock market shows no signs of quitting just yet. You wouldn't know it from all the hand-wringing goin on. Searches on Google for the words "stock bubble” have reached their highest level since January 2022, and judging by my in-box, strategists are fielding questions from worried clients on just how frothy the stock market is."

Bridgewater Associates founder Ray Dalio wrote a 1,700-word missive just last week on why the market isn't in a bubble. Funny how the need for rate cuts has started to fade away. It is becoming clear that the Fed is not going to deliver the seven rate cuts in 2024 that markets were expecting. Sure, there is some froth, possibly in Bitcoin or some technology companies, but for the most part the advance has been consistent and quite tame with less than 50% of the companies above their major moving averages.

Hedge funds, meanwhile, are protecting themselves against a downturn in the market by remaining underweight companies that would benefit from higher inflation and good economic news. They seem to be hedging against everything but positive tail risk according to Savita Subramanian, head of US equity and quantitative strategy at BofA securities. "Instead of expecting the worst, investors should just accept that the bull market that began in October 2023 is only half over, at least based on history. The average bull market since 1930 has lasted 694 days." This according to Pat Tschosik of Ned Davis Research, who goes on with, "the current one is only 344 days old, implying that it's only at about its midpoint." Now I am not saying that Ari is right, and we are only one month into a new move or Pat is right and we are only halfway into a move that started in October of 2023, but instead I am saying that this move is real, it appears to have legs that are getting stronger, not weaker, and being cautiously optimistic could be a better strategy.

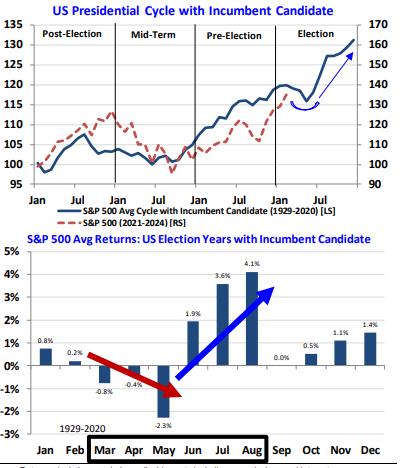

I often use seasonal data to show what possible expectations could be. I find them valuable in a secondary sense to the points I made above. This has been particularly true "this time" as this market bounce from the lows of October 2022 have followed very closely to the seasonal expectations of a typical election year, and actually, as seen below, this presidential cycle from 2021-2024 has been quite consistent with cycles going all the way back to 1929! What I have been warning of as a possibility is what is seen in the lower graph where March through May tend to be the worst months of the year and to be prepared in case this ended up being the case.

The S&P 500 has closely followed its typical seasonal trajectory in recent years. It can therefore be considered concerning that this March through May period has been the poorest stretch in a first-term election year since 1929. Since the overriding trend has been consistently positive, this negative seasonal time could be a sideways move instead of a decline, particularly when the average company is not super extended above moving averages. So, I come away with an expectation that this seasonal weakness instead of being a headwind for a further advance, we believe these seasonals indicate the potential for market consolidation but that there is so much dry powder that market participants aren't waiting for the consolidation to be over given the expectation of further advances post May. One other point I have observed in the strong weakness being exhibited by Apple and Tesla (members of the Magnificent Seven) have had virtually no impact on starting a wave of negativity in the broad indexes that they have a big vote in. I think this is really important. Oftentimes, when a couple of big companies begin to show weakness, this can be the first two dominos to fall where momentum builds on the downside, and this hasn't happened either.

In closing I wanted to once again touch on how truly strong the markets have been for the last 18 weeks. In looking back through history, four straight months of gains during the Winter months has had a perfect track record for full year performance for SPX. Don’t look now, but SPX has managed to turn out four straight months of gains following last October’s 2023 market bottom.November, December, January and February have all been positive, a feat that’s only happened on 16 prior occasions over the last 90 years. Interestingly enough, each time this has happened, the entire year has shown positive returns, for a perfect record of 16-0. Moreover, the average return from March until year-end has averaged +15.5%. March’s average return in those 16 years where the prior four months showed consecutive gains was also +2.2%, much higher than the average +0.4%. Overall, given this undefeated record of gains, I feel that 2024 could prove to be a stellar year. At present, the key takeaway here is that “Momentum usually begets more momentum,” and as the popular saying goes, “The trend is your friend until it ends.” While an intra-year pullback is normal and even likely, 2024 should prove to be a positive year, and recent gains and momentum seem to back that up.

Happy Wednesday.

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

-

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.