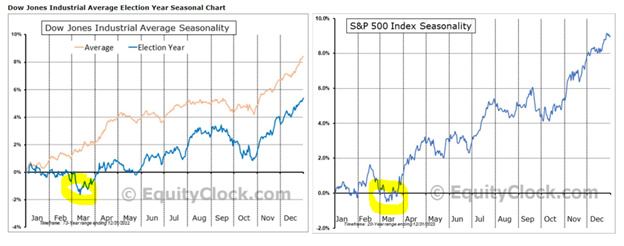

In last week's newsletter I gave a lot of perspective on the markets and that it appears that it might be time for a “digestion." Given that I have received many calls and emails about this term "digestion" and how to quantify it, I thought it might be good to take another look at the markets overall and really think about where things could go. Obviously, nobody knows exactly where and how high or how low the markets will go, but there are some breadcrumbs that often give some hints based on history, current performance statistics, and internal measures. I always caution against relying too much on seasonality since it is only an historical average and guarantees nothing, but it can be helpful to at least keep it in mind and be mindful. Over the past 20 years, the S&P 500 has been strong, on average, during the first half of February but tends to top out around February options expiration (this Friday, February 16th) and fall into mid-March. Similarly, over the past 73 years, during election years, the Dow Jones Industrial Average has tended to struggle into mid-March before rallying into the pre-election period. If history plays out again here, it may mean the recent strength could keep up at least this week and possibly next before finally providing a more meaningful pullback. As is normally the case, this has tended to rely on inflation / interest rates, which clearly were not friendly this week with Tuesday’s Consumer Price Index (CPI) number being hotter than expected. Here are the charts from EquityClock.com that show exactly what I am saying. I've circled the March period in yellow:

To give some color on the bigger picture from Bespoke Media,

“In terms of the S&P 500's performance over the last three months, it ranks as one of the strongest in market history, and as of 1/30 it reached the 99th percentile of all periods. When the trailing three-month performance of the S&P ranks in the 90th to 100th percentile, forward returns over the following one, three, six, and twelve months were among the strongest of any other decile.”

That seems fairly compelling to me to be a reason to stick in the markets even through the digestion period that Thomas Lee of FundStrat keeps mentioning. At the same time, as seen in the chart below, the S&P 500 has done the infamous "hockey stick" straight up for the last 14 out of 15 weeks.

One of the logical things that I consider is, if the market is going to pullback, where will the money go? This last weekend in Barron's there was an article titled, "Cash's Reign Looks Over. What's Next?" Interest rates have begun rising once again due to the Fed Chair Powell stating publicly- numerous times, that he is in no hurry to cut interest rates. He appears right, at present as illustrated by the CPI strength I mentioned above. Since the markets seemed to be depending on the rate cuts beginning in March, and instead the labor numbers a couple Fridays ago were off the charts to the upside and interest rates bottomed and started to turn up, this could quite possibly cause a small shockwave in the equity markets given that this is different than what has been expected to happen in the next quarter. What is different is that the markets seemed to be banking on the first rate cut being in March, and in doing so preventing the bigger fear- recession. Instead, it is seeming like the rate cuts might not begin until May or even June. See the chart below. Notice how the bottom in the equity market above (before this big 15 week run) coincides with the top in interest rates below.

It is beginning to appear that the current status of the market is a tug-o-war between nervous bulls and angry bears. For the bulls, they have been enjoying the rally for the last 15 weeks and are now wondering if there is still enough fuel in the tank to keep it moving higher. For the angry bears, there simply has not been an entry door in the form of a pullback to invest sidelined capital. Based on my multiple interactions with traders and investors, the predominant view is that of the angry bears. Most recently, many cite the fact the Fed is not nearly as accommodative as the markets are hoping for. On the surface, that is what Fed Chairman Powell has stated, even in his most recent 60 minutes interview.

Given that the markets have been strong and that they are due for a short-term pullback, and given that the labor numbers, the CPI numbers, and comment out of Fed Chairman Powell have telegraphed to the bond market that we are probably on the verge of an economic soft landing and not a recession, how do the markets usually act going forward? I mean, isn’t this the most important question for investors today? Well, on top of the seasonal and election year statistics going back 73 years as illustrated in the beginning of this note, I then analyzed the work of Ed Clissold of NDR Research. Ed penned a report last week titled, “Dear Jay: move slowly. Sincerely, the bulls.” I found this particularly interesting as it provided a graphic comparison of what happens in various types of economic cycles. What got my attention was that the slow recovery cycles tend to be the best ones. These are measured by the action out of the equity market following the first Fed rate cut. Stocks have tended to rally after the first cut, but the phase of the economic cycle has mattered. The strongest performance has come during soft landings, while the weakest has come when the economy entered recession less than a year after the first cut.

The slower pace of rate cuts (which seems to be what we are moving towards today), has been bullish for stocks historically. The reason being that this slower cycle of rate cuts tends to imply a soft landing. If the economy is heading toward a soft landing, the Fed can afford to move gradually, like in 1984, 1995, and 1998. The way to interpret the chart above is that it is a fast cycle if there are more than five rate cuts. A slow cycle is less than five rate cuts.

In closing, it appears that the economy is more resilient than the rate cut expecting camp is expecting. This appears to be confirmed by the labor numbers, the CPI reading and the comments from Powell. As far as when and how many rate cuts are to be expected, the window to make the cuts seems to have a hard close around September or October as it is highly doubtful that there would be rate cuts in the 6-8 weeks leading into a Presidential election. If the economy is stable—not too hot or too cold—then more than five cuts wouldn’t really be needed. This on top of the statistics provided would intimate a decent market going into year end 2024 even though there could clearly be periods of discomfort as we are expected now. If this roadmap changes, we will be sure to let you know what is changing and what should be expected as a result.

Stay tuned!

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.