After a very aggressive (almost historic) advance in the equity markets stateside, a much-needed digestion has begun. I have been talking about this in the last month or so in my missives, but I wanted to kind of put a bow around a lot of things today. This is the short list of the many points that market naysayers have been espousing as of late. These are in no particular order of importance as they all carry weight at times:

- Interest Rates- interest rates as measured by the 10-year US Treasury has been rising. After being in a range for the better part of three years, the robust earnings of corporate America coupled with the still massive amount of cash on the sidelines is being manifested in higher inflation and therefore higher interest rates.

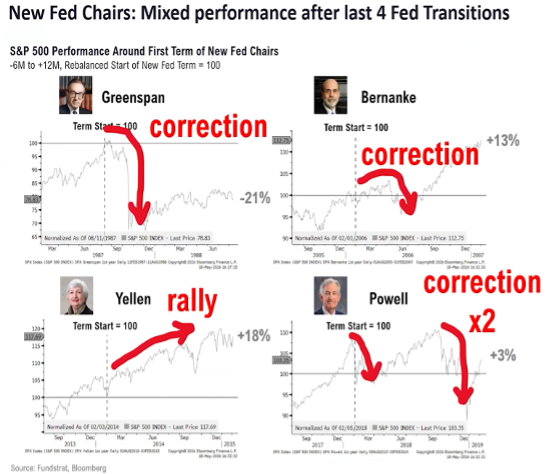

- New Federal Reserve Chairman- historically this has been a negative for markets. In US history there have been 13 Fed Chairs. In 11 of the 13, the markets have had a bout of decline at their onset. I believe this is the result of them being an unknown. Fed Chairs are appointed, they are not elected. So, there is really no precedent for the markets to go off of in handicapping their future expectations. Hence, the markets tend to start off defensive until after the new Chair makes comments and shows their expected actions. This is how the most recent Chairs have experienced the markets:

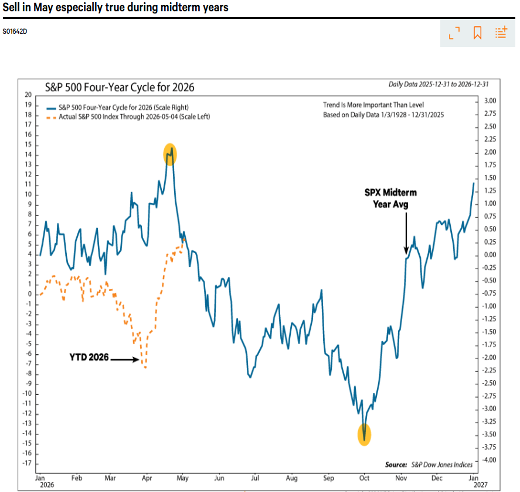

- Midterm years tend to not be friendly. The first year of the term seems to be a bit of a honeymoon year. The second year is when the President does his heavy lifting and this tends to shake things up a bit so again, markets don’t like what they don’t know and as things are shaken up from a policy standpoint it could mean a need to handicap the future in a different way. This tends to correspond to derisking of portfolios by institutions and therefore temporary market declines. Here is this year overlayed on every midterm year going back to the 1920’s:

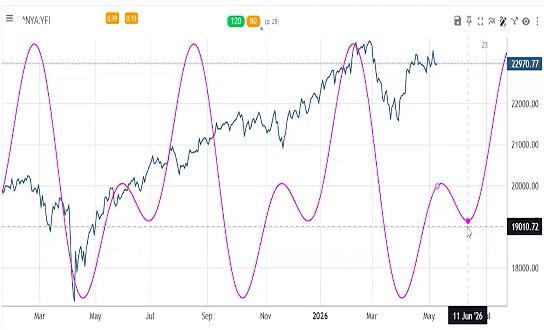

- The cycle work of Larry Williams and FundStrat Direct’s Mark Newton- according to their cycle work that was shared prior to the start of 2026, the market has followed their crystal ball like projections. The interesting thing is that their projections only talk about direction, not target prices. So, when they say things are strong, there is no way to project how strong. Conversely, when things are projected to be weak, this could mean sideways or down or some combo of each. As I stated two weeks ago, this sideways to down should have begun around Mid-May and should last until the second week of June. Here is their cycle study:

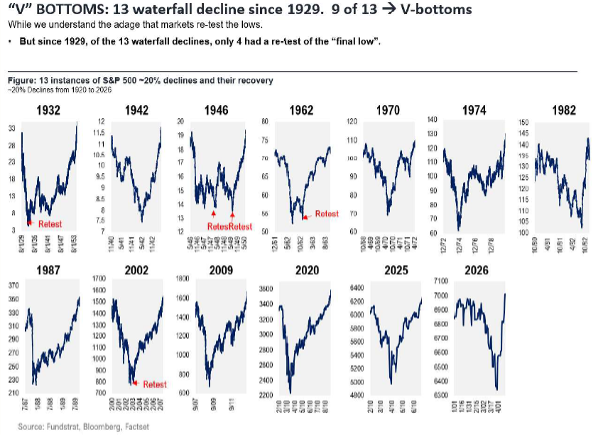

The next point that I wanted to bring up is this incredible friction or bifurcation between the liberal left media who are relentless at bashing the Republican President Trump and therefore anything that could be construed as positive that is going on in the economy and the stock market. This is evidenced by the reading of consumer sentiment being at the lowest it has ever been in recorded history. Thomas Lee states this by showing that this year is a typical V-shaped bottom (at the March 31rst bottom) and recovery. Here is the clear illustration going all the way back to the 1932 bottom:

Notice that 2026 is the most recent so one can see how they all have played out. I don’t profess to say that everything is perfect, particularly when we are in the middle of a conflict that doesn’t seem to have a discernable end, and Russia and the Ukraine are still deep in their conflict. But all the same, earnings are far better than were expected for the first quarter and companies continue to forecast and guide higher moving forward.

In closing, we always need to be prepared for the unknowns out there, but for some strange reason the financial markets seem to sniff these things out ahead of time. Hence, we will be vigilant in paying attention to the markets and moving funds accordingly so as to be as well positioned and prepared as possible.

-Ken South, Tower 68 Financial Advisors, Newport Beach

-

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The S&P 500 is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States. Indexes are unmanaged and cannot be invested in directly.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The NASDAQ Composite Index measures all NASDAQ domestic and non-U.S. based common stocks listed on The NASDAQ Stock Market. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the Index. Indexes are unmanaged and cannot be invested in directly.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

Data sourced from Bloomberg (2025).

Stock investing includes risks, including fluctuating prices and loss of principal.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Bonds are subject to availability, change in price, call features and credit risk.

Government bonds are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

Bond yields are subject to change. Certain call or special redemption features may exist which could impact yield.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor’s portfolio. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

The financial professionals with Tower 68 Financial Advisors are registered with, and securities and advisory services are offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC.

LPL Tracking # 1114549