This week I am going to go over the progression of how we analyze the markets while at the same time trying, as best we can, to ignore the militaristic flurries throughout the world. I say militaristic flurries, but I do not want to minimize the loss of human life and property and the negative effect on quality of life that is sure to last for some time. It can always be discussed "why" Israel attacked Iran, or possibly who motivated this conflict due to oil or some other speculated directives, but it is not a comfortable situation to anyone and we certainly hope for a quick resolution.

As I write this President Trump thanked Iran for letting the US know that they were going to bomb Qatar, and that no lives were lost and nobody was injured, and within 12 hours of the bombs being dropped, Qatar air space was opened back up for commercial travel. Prior to this attack in Qatar and after the three nuclear facilities were destroyed in Iran, I put pen to paper about my opinion on the conflict.

My assumption has been that Iran would not close the Strait of Hormuz because Iran needs revenue. Closing the Strait would deprive them of that revenue and could anger its biggest customers, particularly China. Iran represents 80% of China's imported oil. Iran doesn’t have many friends. Shutting the Strait doesn’t directly impact the U.S. because the U.S. doesn’t need oil from the Gulf. Closing the Strait could hurt Iran more than it would the U.S., which is why I remain skeptical of a sustained rise in oil prices. On Monday, after the bombs were dropped in Qatar, oil promptly dropped by over $5 per barrel, almost 8%. Additionally, Trump needs low oil prices to make his domestic agenda work, so U.S. attacks on Iranian oil infrastructure seem low but anything can happen in armed conflict. With the news flow moving quickly, I will limit my comments to three topics:

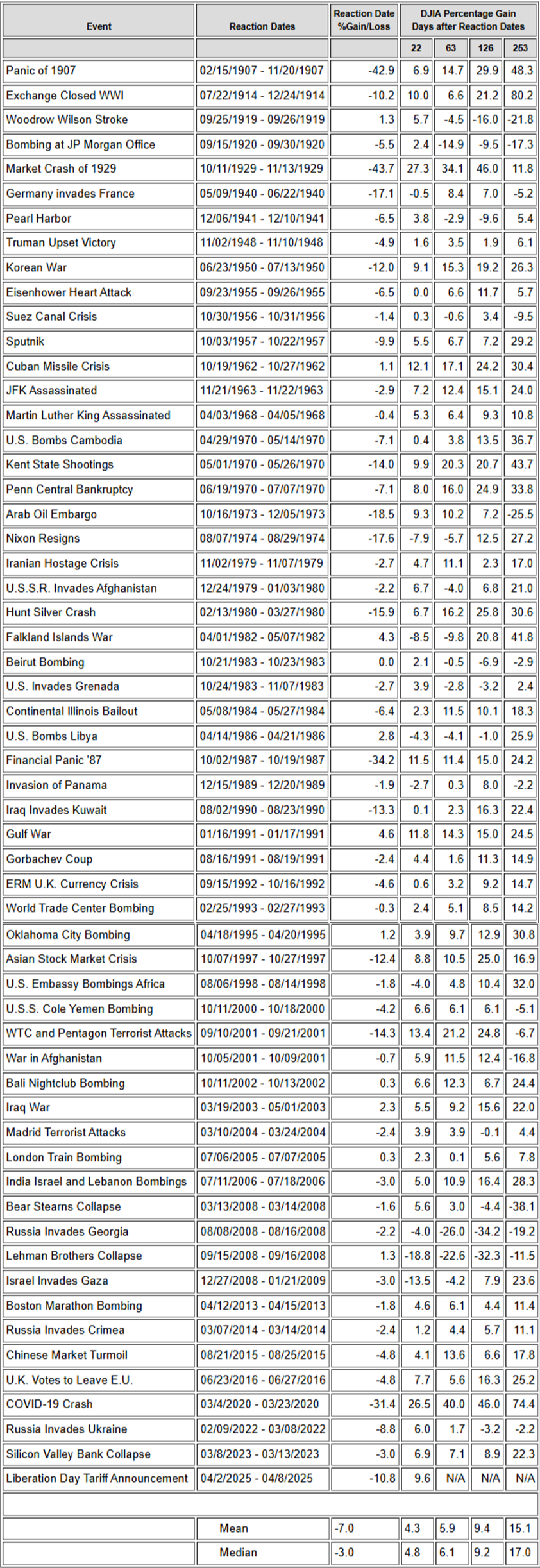

First- are there good historical analogs for what occurred over the weekend? Although no two events are the same, I extracted the instances from the crisis events table that was put together by the team at Ned Davis Research, that were closest to this weekend’s event. The instance of the conflict normally creates defensive action in equity markets initially. Mondy of this week was a perfect microcosm. The markets opened Monday down about 1% on the heels of the US's attack on the nuclear facilities. The markets recognized that oil facilities were not damaged, and human life was spared, so the S&P quickly recovered higher to reverse the decline and rise close to 1% above Friday's close. Then the six bombs were dropped on Qatar. The markets immediately reversed and were down once again. Reports came that there were no deaths, and no injuries and stock prices reversed once more with the indexes closing up almost 2% from Friday's close. In looking at the table below, it can be seen that stocks were mostly higher over many different time periods. I was quite impressed by the team at NDR as they covered virtually every conflict going back to 1900.

Second- as I have written previously, this year I have mainly focused on one of my favorite sayings, "Don’t Fight the Government or the Fed", and what guardrails there might be around policy, if any. In addition to financial guardrails, my assumption has been that Trump would listen to his MAGA base. The hurdle is high for a 2003-style ground invasion. In his brief statement on Saturday evening, the President wanted to avenge the deaths of many Americans at the hands of Iran, given that diplomacy no longer seemed to be working over Iran’s nuclear program.

Third- we need to understand the positioning of the market going into this event. Bond sentiment was moderately pessimistic. The Fed seems to be working opposite to the President's vocal commentaries on the desired direction of interest rates, and even though inflation remains subdued, interest rates remain stubbornly high. We wouldn’t expect a major move to the downside in bond prices (yields higher), considering the flight to safety bid. Crude oil sentiment, however, has remained neutral and Monday morning oil prices actually fell, so again, a quasi-nonevent.

Crisis Events, DJIA Declines and Subsequent Performance

The list below, which I mentioned above, is quite extensive as it covers virtually every conflict going back to 1900. Please feel free to look for virtually every conflict that has transpired. At the end of the table, the amount of the decline is provided (on average) and then the return of the markets 22, 63, 126, and 253 after the beginning of the crisis. This is a table provided by NDR Research. I took the liberty to attach it to this report for illustration purposes.

The Financial Markets

Now that we have addressed what I feel is most current and pertinent about the international conflicts, I wanted to make it clear what we look at from a financial market’s perspective. Of course, conflict must be recognized and handicapped in the markets, but at the end of the day, the money is going to go where it is treated (and expected to be treated) best. Strangely enough, besides the Tariff Tussle that the markets experienced in early April, the S&P 500 seems to be just biding its time and catching its breath since November of last year. This has been almost 3/4 of a year. Oftentimes a move sideways will achieve the same energy rebuilding effect as a moderate correction can.

Ari Wald, this week, made an important point that is being bantered about in the financial press. Is this current price of the S&P 500 a top that is forming, or is it ready to break out to new highs after this eight-month digestive phase? This is really what is driving investors crazy. There have been more than enough reasons for the markets to go down, but they aren't. And if you can recall the statistical studies that I have provided along with the amount of cash on the sidelines, there are a few really strong reasons for the markets to go higher. The S&P 500 is less than 3% away from its all-time high (6,147) set in February. My primary concern is that the rally since the April low has been undermined by narrow internal breadth. What I mean by this is that the companies that led in the move off the April lows have not been joined by the next group of smaller companies that have still not been participating.

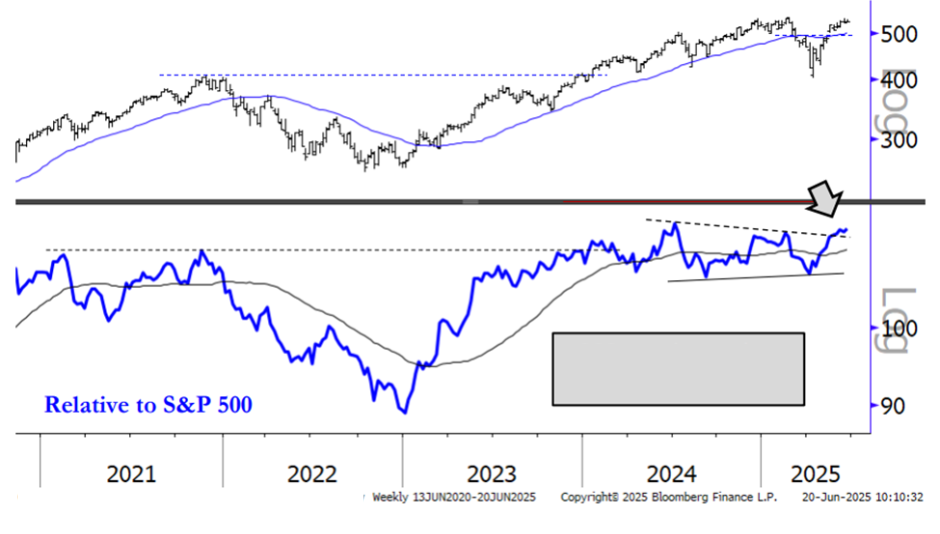

Last week I mentioned that after 16 years of US equities outperforming foreign equities, the large, high quality, foreign companies started a move outperforming the US companies. Well, this changed in the last couple of months and now, relative to the S&P 500, the World (ex US) has begun to pass the baton to the big US growth companies once again. Signs of Rotation back into US Growth in March have mirrored past periods where World (ex. US) outperformance had generally marked opportunities to rotate back into the US over the prior twenty years. We see this as a potential resumption of a long-term trend that still favors growthier benchmarks, like the S&P 500.

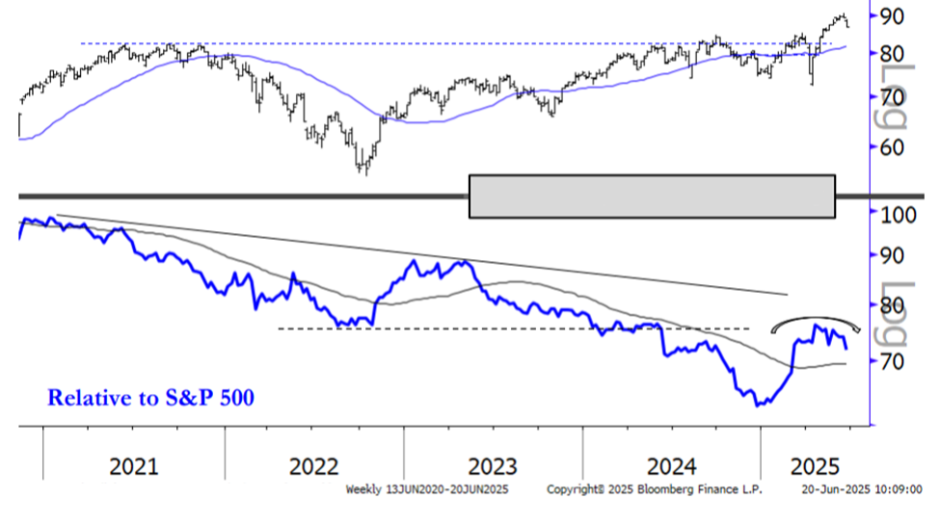

To then take this from a comparison of US to World (ex US) to a measure of what in the US markets are pulling them back to a level of strength, it can be seen in the action of the pure growth NASDAQ 100 and its comparison to the S&P 500. I do this since the driver of the broad US markets have been the bigger, growth types of companies. The clearest sub index to use for this analysis is the NASDAQ 100. Please take the time to recognize below how not only has the NASDAQ 100 started to blast out to new highs, but in the lower part of the graph, relative to the S&P 500 this index has been moving sideways since the beginning of 2024 and is now breaking out to new highs.

If we are to take one more layer off the onion, it can be seen in the comparison of sectors below, that besides Utilities, Technology and Communication services are the clear leaders year to date in the index. I find this particularly important to not only know where an investor should likely hunt, but also where the market has had strength, strength that has been masked by a near zero performance overall year to date.

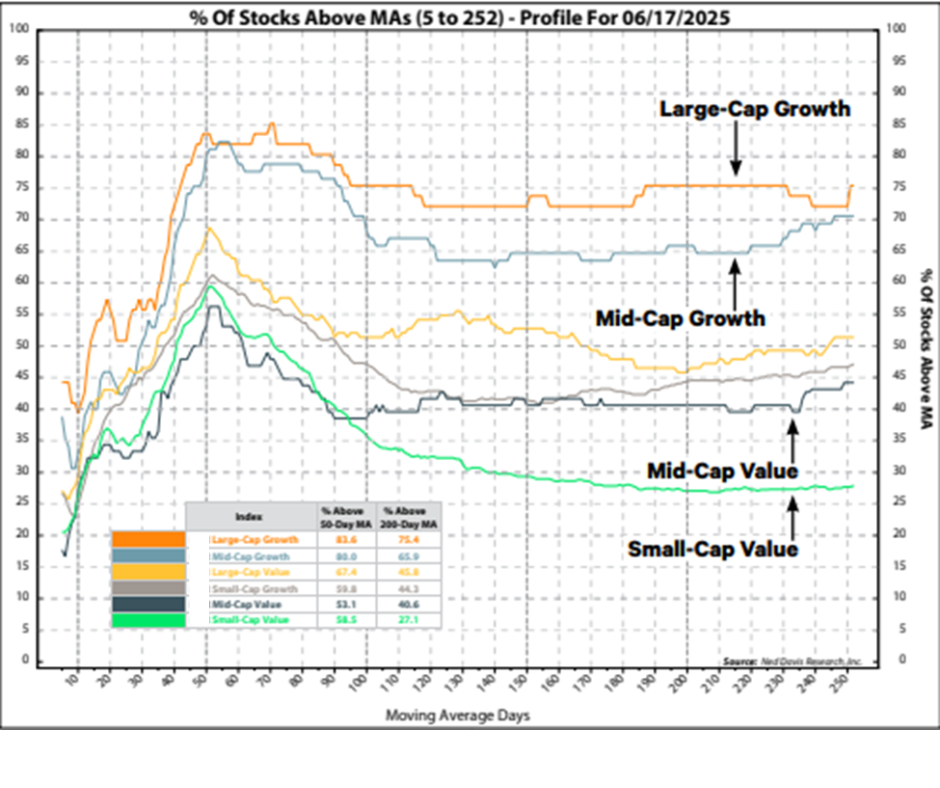

One of the last studies that I find of great importance is the next question that an investor may ask; "OK, we know that growth companies are back to doing the best of overall US companies, and we see that the US seems to wanting to take the lead from the World (ex US) companies, and we know which sectors are driving this move, but should the focus be put on the biggest companies, the medium sized or the small-cap companies?" To answer this, I look at the table below, which compares these against each other. As can be seen quite obviously, the leader is clearly large-cap growth.

I am sure that the international conflicts are not over, and that it might take some time to reach a ceasefire between Russia / Ukraine and the Palestinian conflict but stateside, our economy seems to be doing fine, first quarter earnings were better than forecasted, and second quarter expectations seem to not be ratcheted lower. This could provide a backdrop for further upside in our equity markets.

The last thing I wanted to share was a fascinating Q&A between Martin Armstrong of Armstrong Economic and an undisclosed person. It is in regard to the Iranian conflict as a whole. If you wish, please take the time to read this answer. I found it quite interesting as Mr. Armstrong addresses many issues of the different factions that exist in the Middle East.

QUESTION: I understand you rely on the computer. The forecasts are not your opinion, and that is what makes you stand out among all the talking heads. What is your personal opinion? Do you think that if Trump had given diplomacy a chance, it would have worked, or was this inevitable?

ANSWER: Looking at the computer, I could not see any other outcome. I do believe that Trump acted thinking that this would end the war and the terrorism of Iran. His mistake is judging Iran by what a rational state would typically do. Iran is a theocracy, and its government is driven by entrenched ideas that I do not see changing.

The differing stances towards Israel between many Shia-majority actors (notably Iran and its allies) and some Sunni-led states stem from a complex mix of religious, geopolitical, strategic, and ideological factors, rather than a fundamental theological difference between Shia and Sunni Islam regarding Palestine itself.

The 1979 Iranian Revolution established an Islamic Republic with a strong anti-Western and anti-imperialist ideology. Opposition to Israel (“The Little Satan”) became a core pillar of its revolutionary identity and foreign policy, framing it as a colonial implant, an extension of Western (particularly US) imperialism in the Middle East, and an oppressor of Palestinians.

The Iranian Revolution exported ideology and identity. Championing the Palestinian cause became central to Iran’s self-proclaimed leadership of the Muslim world (“Resistance Axis“) against Western influence and its regional rivals. Iran sees Israel as its primary regional adversary and a major strategic threat, closely aligned with its arch-rival, the United States, and Sunni powers like Saudi Arabia (historically).

Supporting anti-Israel groups such as Hezbollah in Lebanon, Hamas and Islamic Jihad in Gaza, and various Shia militias in Iraq and Syria became the key geopolitical tool for Iran. It projects power and influence far beyond its borders. This established a network of proxies to deter Israeli or US attacks on Iran. This is what I mean about religious issues, for it challenges the regional order dominated by the US and its Sunni allies. This “Axis of Resistance” is fundamentally built on opposition to Israel and the US.

We must comprehend that for Iran and its Shia allies, unwavering support for the Palestinian struggle against Israel is a source of domestic legitimacy and a way to claim leadership of the broader Muslim world, transcending sectarian divides. Portraying Sunni states that normalize relations as traitors to the cause reinforces this narrative. It remains to be seen if the Shia will instigate civil unrest within the Sunni states like Egypt, Jordan, and Saudi Arabia.

There are significant differences in Sunni approaches (pragmatism and shifting alliances) compared to those of the Shia (confrontation).

Some Sunni-led states (UAE, Bahrain, Morocco, Sudan) normalized relations with Israel based on pragmatic national interests, not theological shifts. They have a shared perception of Iran as the primary threat (especially for Gulf states). They are far more practical in terms of access to technology, trade, investment, and tourism. They also gained US favor, breaking diplomatic isolation. They have believed that engagement might yield better results than a boycott or prioritizing other concerns over it. Israel’s attacks on unarmed Palestinians in Gaza threaten that practical view.

It’s crucial to remember that Sunni Islam and Sunni-majority states are not monolithic. Many Sunni populations remain deeply opposed to normalization. Countries like Qatar maintain relations with Hamas but not Israel. Turkey has diplomatic relations but remains highly critical. Jordan and Egypt have peace treaties, but experience significant public opposition and cold relations.

Then there is the risk of state versus non-state actors. Established Sunni states often prioritize state sovereignty, stability, and economic interests. Non-state Sunni actors like Hamas or the Muslim Brotherhood frequently maintain hardline stances closer to Iran’s position (Hamas is part of the Resistance Axis).

Both Shia and Sunni Muslims revere Jerusalem (Al-Quds) as the third-holiest site in Islam. The Palestinian cause resonates deeply on religious grounds across the Muslim world. The difference lies in strategic emphasis. For Iran and its allies, opposing Israel is the central rallying cry and geopolitical strategy. For some Sunni states, while the religious significance remains, it competes with other pressing security and economic priorities in their foreign policy calculus. Iran weaponizes this perceived prioritization to criticize Sunni leaders.

Consequently, Shia opposition (Iran-led Axis) is primarily driven by revolutionary ideology, geopolitical strategy (countering the US/Israel/Saudi axis), regional ambitions, and the use of the Palestinian cause as a tool for legitimacy and proxy warfare. It’s a core part of their identity and foreign policy. This is why I personally am not optimistic, and I fear that Israel may stupidly think assassinating the Supreme Leader will end Iran, and it will return to the days of the pre-1979 Revolution. They put at risk the entire pragmatic national interests of the Sunni States that can see internal strife in response to such an action on top of the hard treatment of Palestinian civilians in Gaza. This can result in shifting regional dynamics that I am deeply concerned about. There is no religious Sunni theological shift on the importance of Jerusalem or Palestinian rights, and it faces significant public opposition within those countries.

The divergence is less about a fundamental Shia vs. Sunni theological difference on Palestine/Israel, and more about differing geopolitical strategies, national interests, and ideological priorities between the Iranian-led “Resistance Axis” and certain Sunni-led Arab states seeking new alliances and security arrangements in a changing Middle East. Iran uses maximalist opposition to Israel as its defining strategy, while some Sunni states have decided engagement serves their interests better, given the perceived greater threat from Iran.

I am not sure that there are people who understand this in the leadership of Israel or the United States. The huge mistake here is assuming that this strike will cause the Shia to throw down their arms and adopt the Sunni pragmatic position. I do not see that sort of religious upheaval.

- Ken South, Tower 68 Financial Advisors, Newport Beach

-

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

Data sourced from Bloomberg (2025).

Stock investing includes risks, including fluctuating prices and loss of principal. (132-LPL)

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Bonds are subject to availability, change in price, call features and credit risk. (116-LPL)

Government bonds are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

Bond yields are subject to change. Certain call or special redemption features may exist which could impact yield.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.