Last week, the equity markets weren't the Thanksgiving turkey, instead they were a bit of Thanksgiving champagne, as is the norm for the week of Thanksgiving. As I have been saying throughout November, the heavily oversold readings in October sort of set the stage for the November / year-end rally. In late October several technical measures of the S&P 500 broke down to highly pessimistic levels. As of now, the market has come out the other side of this critical period in pretty good shape. Being that the markets have gone from “Oversold October” to four weeks of advance and, hence, “Overbought November” gives us a reason to step back, look at where we are, measure the internals and evaluate the most probable next steps. At the same time, we need to evaluate what we should pay attention to in order to see if there are any specific indicators that could tell us to change course or stay on the same course. According to Ned Davis Research, "If the rally is going to make new cycle highs and continue deep into 2024, look for continued improvement from long-term breadth and trend indicators. Topping processes often entail marginal new highs in popular averages and a series of lower highs from breadth indicators."

Last Friday's high "high print" (~4568 on the S&P) sits where there is significant resistance that must be overcome before success is achieved leading to higher prices. Often, I get asked, what exactly this means. If one is to think about it, the market rallied almost straight up through late July, then it backed off. All those that didn't sell at the highs (if past psychological experience is any indicator) think to themselves, hey, I missed selling in July, not much has changed, so I am going to get out here- on my second chance! We never know if this was the right course of action for investors to take till after the fact, but normally, if certain major economic issues change at the lows or are changing when the markets retest these old highs, these can often be good indicators.

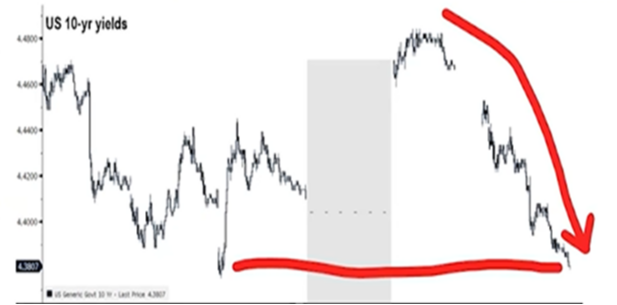

Before I go into the markets, I think it is important to see an update on what I feel is really the reflection of growth and inflation expectations, the yield on the 10-year US Treasury.

Rates seem to be reflecting that the work of the Fed appears to be helping inflation behave and that rates have maybe seen their highs for this cycle. If true, and investors want more than 5% on their funds, maybe a segue into equities could be in the cards.

Below is a picture of the move off the lows, the current advance since this October 27th low, and what is expected by many to occur as a result of the various issues I went over last week. Namely, earnings higher than expected, international issues calming, and most important, measures of inflation subsiding but not at a rate that would infer an oncoming painful recession. I have taken the liberty of inputting the dates of important economic indicators as well to show what “could” cause short-term catalysts for equity market action.

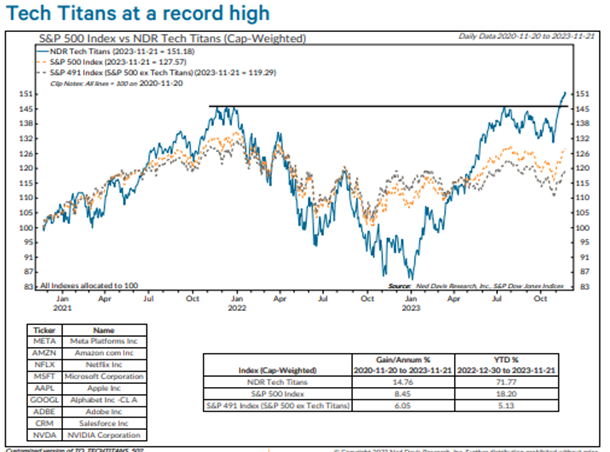

In mid-September Ari Wald made an important comment about the fact that leadership in the markets is narrow, but breadth is not. In other words, as a major market signal, it's important to distinguish between narrow leadership and narrow participation. What this means is that currently, the S&P 500 is still being pulled higher by the "Tech Titans." At the same time, the smaller companies, as referenced by the Russell 2000 Index (companies under $8 billion in size) seem to be coming up as well, but not as much as the big technology leaders. Below is a chart of the Tech Titans, and a table showing the S&P 500 ex-Tech Titans:

But the reason why it has proven best to stick with these leaders is clear in the chart below. The top is a graph of the Russell 2000. Below that is a chart of the Russell 2000 relative to the S&P 500. This is super important! Note that the top chart shows the S&P 500 and the Russell 2000. Note that they look fairly similar. But in the lower graph when the one is compared against the other, it is clear that the best place to be is still the S&P 500 and this index is being led by the Tech Titans:

Relative performance is often tough to see unless a comparative chart is provided, meaning fewer stocks will lead vs. a broad and equally weighted benchmark when the biggest companies outperform. What is important to recognize is that it doesn't mean that only the few are going up. It must also be remembered and observed that the narrow group that is rising doesn't begin to fade.

What is also common about the current market environment is the sector that is leading the markets higher (both S&P 500 and Russell 2000)—the Technology sector. The S&P 500 outperformance in a rising market becomes less surprising when we consider that technology has outperformed during 20 out of the 23 bull cycles (87% of the time) since 1932! This is the top hit rate for all sectors of the economy. Below is a chart of every bull cycle since 1932:

Clearly this speaks to the strength of the NASDAQ 100 as it is 48% weighted in the technology sector. In a comparison to the S&P 500 vs. the Russell 2000, the NASDAQ 100 is dramatically higher weighted in large technology companies. Below, see the S&P Technology ETF vs. the S&P 500. I am showing this to further boil down the clear separation in overall performance of large technology to the broad market:

The next question that I feel is relevant is whether there is enough fuel left in the tank for the markets to move even higher than the July peak and possibly above past cycle peaks. I don’t mean that this has to happen immediately either. It really might take a few tries for the index to move up to this high, bat its head against it, exhaust some of the sellers I mentioned at the beginning of this report and eventually move above old highs.

As to how this eventual breakout could occur, below I look at what the investment of choice has been for both institutional and retail (man on the street) investors combined since October of last year. As can be seen, the biggest flow of capital has gone into money market funds and short-term CDs and US Treasuries. It has been so long since an investor has been able to earn the returns that are currently available in a riskless investment, as inflation, international conflict, unsure earnings future, and high inflation persist, many have taken the choice of low to no risk. The second investment of choice has been bonds in general. Although they are subject to credit risk and higher interest rates, many are plenty happy with the rate they are getting to maturity. Last has been stocks. Massive amounts have flowed out of stocks into other assets and, hence, I must ask what could happen if some of the money in the most liquid choice (money markets) were to decide that taking some risk might be warranted?

Well, if the last few weeks are any indication, some of this money is clearly coming off the sidelines and into the equity markets. Below is a chart that shows the biggest 2-week inflow into equity funds since February of 2022, courtesy of BofA Global Investment Strategy. It isn't a spike like the ones we saw in late 2020 and 2021, but clearly a change from the outflows we have seen all year:

If the two charts above are true, then it is fairly clear that the fearful investors that have stayed in cash have largely missed the S&P 500's 2023 gains. Many will choose to invest in the laggards that are starting to rise, like the Russell 2000, but until there is weakness shown in the larger companies collectively, this might be premature. The percentage of New York Stock Exchange stocks above their 200-day moving average increased to 46% last week from 23% in late October. Looking ahead, if we were to get this reading above 60%, strangely enough, this would argue for less of a chance of it being a market top since breadth is clearly expanding. Taking all of this into consideration, the reasons that I expect there could be higher prices on equities into year-end (as chart 1 illustrates) are multiple. Here is a short list of some thoughts:

- Incoming data continues to support a "soft landing" vs a recession, hence the market participants have been too skeptical.

- Key driver of interest rates, likely the Fed's December FOMC meeting, we believe could lean toward "dovish" and imply rates are done being raised and maybe even lowered.

- Equities finally seeing positive inflows from investors for the first time since February. See charts above.

- Retail investors have pulled $240 billion out of stock market mutual funds and ETFs up till now in 2023.

- Seasonally positive factors still prevail, particularly as we enter December.

Surely there will be some flies in the ointment, but with rates starting to fall from the October highs, measures of inflation cooling off, and companies reporting better and forecasting better than analysts expect, this year could finish higher and next year could see a continuation of the same. An issue I haven't mentioned in this note is the 2024 presidential election. Since Biden's approval ratings are quite low, the current administration could use almost any trick up their sleeve to make a case for them being behind a strong stock market and economy going into the election. Stranger things have surely happened!

-

-

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.