I hope everyone had a terrific Easter. Except for the rain, it was pretty nice on the Southern California coast. Last week proved to be another week of record highs in the major US stock indexes. Over the last few weeks, I have kept on talking about how it is about time for the equity markets to take rest. Clearly the markets haven't been ready as they have continued to percolate higher. I have attributed a lot of this to the level of cash on the sidelines, but there clearly has to be more to it than that. At present, the NASDAQ Composite has been the leading index for the year. Last week showed that even the leading index was beginning to show some signs that maybe a rest is due. This is what it is showing currently:

I bring this up as this index has started to show some distribution days as I have noted on the chart. This is a very short-term chart, just including the period since February. I’ve done this to be a bit more granular so I can show what "may be" starting to happen versus what we have been experiencing.

Above I have given the very short-term. Below, I feel it is important to reflect both on the period of time that the markets have been in an uptrend as well as where we are in the Presidential cycle. I bring up the Presidential cycle as this goes back to the 1920’s. It not only has a very long-term history but is also very consistent. This consistency, coupled with the 21 week straight run higher and the beginning of the distribution days seen above could be quite telling with what could be expected should it follow the historical. Please take a moment and look at the two charts as they should be committed to memory:

Now, look at the Presidential cycle chart and notice that I have drawn a small annotation to show the small pullback that tends to happen during April & May. Will it happen this time? Well, I believe that probability says that it might not be a big decline, but it could be a sideways sort of back and forth at least, given that the monetary situation has changed somewhat. When I say monetary, I am referring to the expectation of the slowdown in the economy, yet the most recent economic indicators are far from a slowdown and are actually quite inflationary! The 10-Year US Treasury yield has reflected this economic strength, and the yield has gone from 4% to 4.4% in the last 30 days. This may not seem like much, but it is a 10% increase in this interest rate in 30 days. Equally shocking is that our short-term rates are the highest in the Developed World as seen below. This makes very little sense to me if we are the strongest economy.

Last Friday, when the markets were closed for Good Friday, we got an important economic indicator, the PCE report (Personal Consumption Expenditures). The overall number came in as expected, but there were some parts of it that showed that inflation might be accelerating, not declining. The goods inflation came in up .5%. Not an earth-shattering report, to be sure, but the bottom line is that inflation is not going away. Anybody that shops at the grocery store, buys gasoline or goes out to a restaurant knows this, but the politicians and the Fedheads continue to parrot the disinflationary line which really just refers to a steady state rise in prices without any acceleration. That may, however, change as the Fed holds steady but the government continues to shovel trillions into the system.

Monday, we got the ISM Manufacturing numbers. This index rose to 50.3 in March, beating the consensus expected 48.3 (levels higher than 50 signal expansion). The major measures of activity were mostly higher in March.

- The production index rose to 54.6 from 48.4 in February.

- The new orders index increased to 51.4 from 49.2.

- The prices paid index increased to 55.8 in March as well, above the February number.

The ISM Index peaked in March of 2021 (the last month the stimulus checks were sent out) and has been weaker ever since. After the number has been sitting in contraction territory for most of 2023, the prices index has been above 50 each month in 2024, signaling higher prices. This is not a good sign for the Fed, as the goods sector has been a key driver for lower inflation readings over the last year.

The bond market got kicked in the shins pretty hard over these two numbers from Friday and Monday and the 10-year US Treasury rate spiked higher. This unexpected shock could be the catalyst that is needed for the market to begin its digestive phase. If the institutional investor is expecting interest rate cuts to fuel money flows into stocks, and the economic indicators are strong enough that the Fed needn't do anything then year-end expectations might have to be recalibrated assuming higher interest rates. To almost confirm this, on Friday, Fed Chair Powell delivered the same message that he had the week before following the FOMC meeting- the Fed was in no hurry to cut rates.

Last week, Joe Kalish, Chief Global Macro Strategist of NDR Research identified a number of reasons why the Fed should begin trimming rates as soon as June. Negative market prognosticators continue to ask why the Fed needs to cut rates at all. Yet there are five clear reasons that evidence that the last set of Fed rate hikes have slowed the economy and therefore if the Fed were to wait too long, the economy could accelerate its slowdown velocity and we could end up in a recessionary environment.

- Softer employment- When the Fed began hiking rates in March 2022, the year-over-year change of cyclical employment was growing greater than 4%. Today, that growth has slowed to just 0.6%, as shown on the chart.

- Slower loan growth– The increased cost of capital and tighter lending standards and terms caused the year-over-year change of loan growth to peak above 12% in December 2022. Today it has plunged to 2.1%.

- Weaker housing– Residential construction spending, which had been growing 25% year-over-year when the Fed started tightening policy, collapsed to nearly -15% a year ago, before rebounding some to 5% in recent months.

- Cooler capex– On a trend basis, durable goods orders topped 10% year-over-year in March 2022. In February, it had slowed below 2%.

- Increased delinquencies, defaults, and charge-offs– Whereas consumer delinquencies have risen from 1.53% to 2.62% in Q4, charge offs have risen from under 0.96% to 2.65% in Q4.

How long after rate hike cycles end to rate cut cycles begin?

The last rate hike was almost a year ago. The median time after each rate hiking cycle ends and an easing cycle has begun has been 7.5 months. If the Fed were to cut in June, this would be 10.7 months. My worry for the equity markets has been over the intermediate-term outlook. What happens if labor force growth slows and supply chain improvement fades, and the demand remains strong? With GDP running above potential, our analysis of the output gap shows it is on the cusp of moving into the above-target inflation zone.

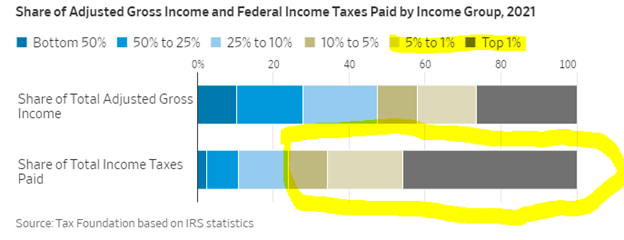

The last point I want to make is about Biden's endless attack on the high-end taxpayer, and the pandering to the constituency about raising the taxes on the rich. In the weekend Wall Street Journal there was an editorial piece worth noting. “The U.S. Already Soaks the Rich.” In 2021 the richest 1% paid 45.8% of income taxes, up from 33.2% in 2001. The link to the full article is here:

The full article explains every detail, but the charts below show not only who is paying the most but also how the highest payors are actually paying even more every year.

The reason that I bring this up is that this is one of the three major points of contention across party lines in the coming Presidential election. Last week I mentioned Medicare, this week’s taxation of the wealthy, and I hope to have data on Social Security this coming week.

-

-

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

-

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.