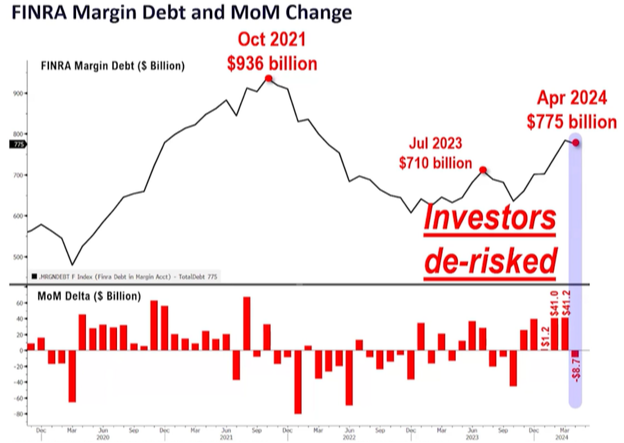

As summer begins in earnest, the slowdown in the markets begins as well. Summer tends to be a little sleepier for the markets, unless of course, there are as many events going on as there are this year. The tug-o-war that I keep referring to between the Fed’s need to cut interest rates to stimulate the economy and, in the process, make real estate more affordable to the purchaser is being negatively counterbalanced by inflation numbers, employment numbers and wage numbers that are showing a still too resilient consumer. Based on the action of investors, they are clearly on the defensive as they have been active at pulling funds from equities:

This past weekend Barron’s showed a picture of Fed Chairman Jerome Powell on the cover with the quote, “WHY HE WON’T CUT RATES THIS YEAR.” The overriding issue that seems to be swaying the normal way of measuring this tug-o-war is unquestionably the $6 Trillion sitting in cash earning a no-risk 5%. This not only is continuing to provide liquidity, but an unquenching purchasing power by the consumer.

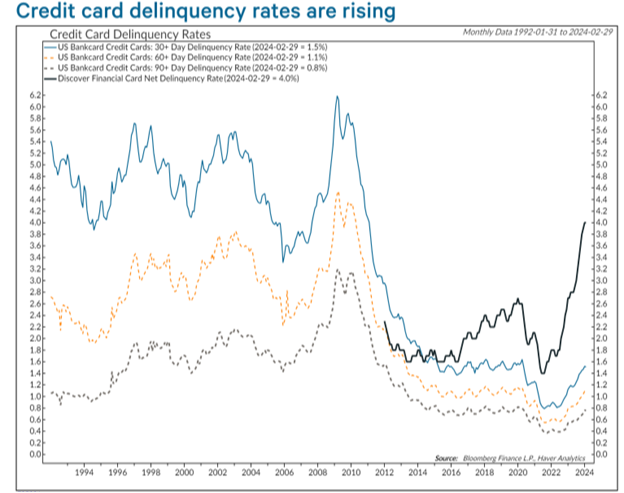

This brings into question “who” is in control of this massive cash balance, and this seems to be obvious if we look at the delinquency in credit card payments. The lower- and middle-income consumer often have to depend upon credit cards to meet shortfalls, where the higher income brackets are diligent to pay their monthly credit card bills to avoid the exorbitant interest rate charges:

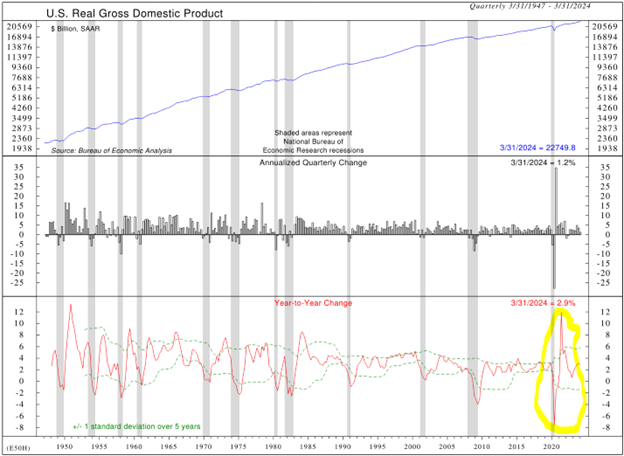

At a deeper level, it is important to not just look at the consumer, but more importantly the broad economy at the GDP, or Gross Domestic Product, level.

The real root of GDP growth is the real story on Q1 GDP: Government spending accounted for 34.4% of all the spending. Over 1/3 was from the government spending well beyond any tax dollars it the government can collect. If you remove the spending for the Ukraine and Israel wars, GDP was negative. Government spending is propping up the GDP ‘growth.’

Oil has decreased in price, likely because economics are poor enough around the world to reduce demand. That helps, but it does not solve the problem for other critical areas. See below. I bring up oil as it is still the backbone of measurement for an industrial economy:

The point: the GDP issues show the CPI, PPI and PCE numbers are the tail wagging the dog. They are the symptom of the problem, and the Fed is focusing on the wrong issues. Growth was the softest since Q2 2022 and much weaker than the 4.1% average annualized rate in the second half of 2023. A significant drag in Q1 came from inventory investment (-0.45 ppt) and net exports (-0.89 ppt), both revised down from the original estimate. But final sales to domestic purchasers, which exclude inventories and net exports, rose at a 2.5% annualized rate, only slightly below the advance estimate and the average rate of 2.8% since 1980. To give a final perspective on the progression of GDP, see the picture below. Please note the massive volatility due to the COVID period and how it has now largely normalized:

The Fed, however, won’t ‘break things’ in an election year. Powell wants to avoid that humiliation, so no breaking things, and will likely cut pre-election. The ‘dip’ in the PCE gives him some sort of moral authority to cut the rates, and thus we should see the PCE grow at around the same rate or slightly lower. If things really get out of hand on the election front, we could see PCE go negative. This leads us to additional measures of weak economic data:

- Income and spending- were considered palatable, but the bottom line is not: real spending fell 0.1% when nominal growth was said to be 0.2%.

- Pending Home sales, April- -7.7% versus -3.6% March. Record lows.

- Bank Deposits- The Fed reported large banks gained $2B in deposits for the week. If you look at the unadjusted numbers (seasonal, of course), the actual numbers, large banks lost $98 billion in deposits. Once again, reality differs from the made-up world of government and not-so-government entities such as the Federal Reserve.

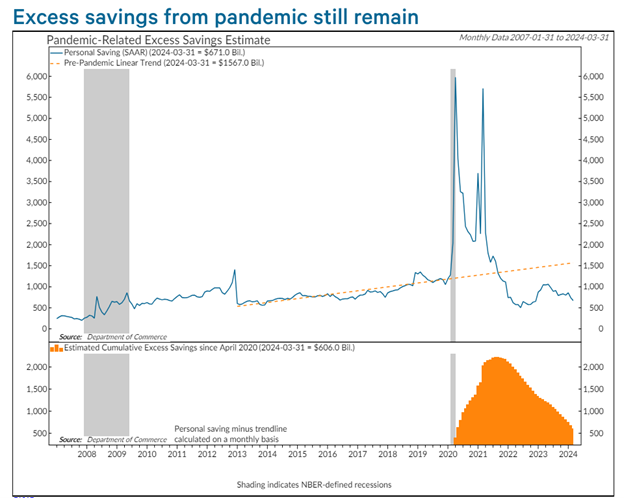

I want to give an update on the amount of money that is still sloshing around out there. I referenced this in the beginning of this comment but wanted to show an updated illustration of the number. It reflects the amount still in savings post the pandemic. This is what I believe, on top of US Government spending, is swaying consumption and accurate economic growth measurements:

All these points I’ve just made I believe point to just the opposite of what we were presented with by Barron’s last weekend. As evidenced by the ISM numbers on Monday, and the Job openings yesterday, the Fed might have to provide liquidity in the form of lower interest rates in short order should economic cracks form. See what the 10-year treasury market is saying as of yesterday, mid-day:

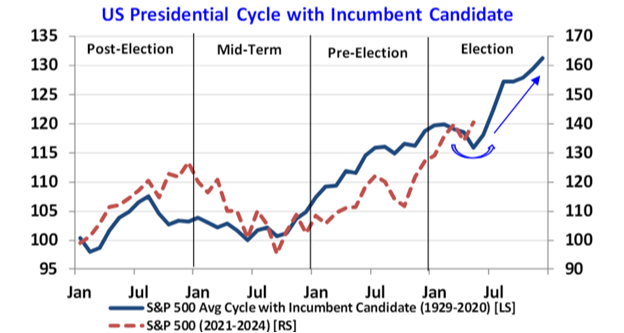

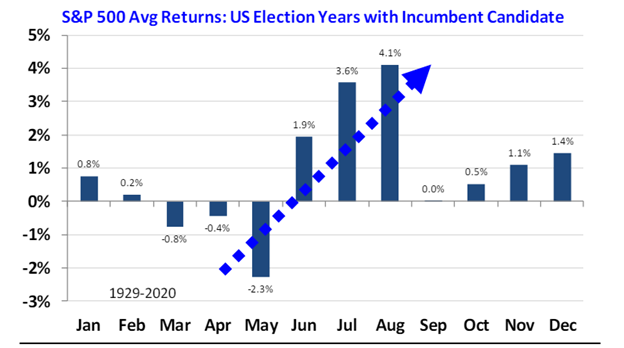

The strange thing is that if interest rates were to fall, this could be the catalyst for the rally that is seasonally / statistically expected. I have brought up the election cycle numbers and the seasonality numbers before, but here is an update:

For the S&P 500, June through August has been the strongest three month stretch of a first-term election year since 1929. This is a fairly strong statistic as it has taken into account many different economic, global, and political environments.

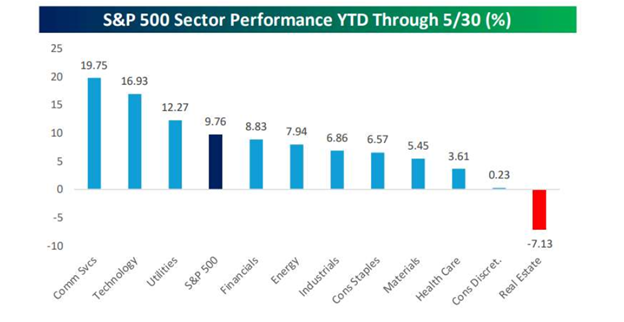

I will close with the measure of the performance of the 11 sectors of the S&P 500 from the beginning of the year through May month end. Note that only 3 of the 11 have done better than the entire S&P. This shows ample room for a broadening of the market index’s performance into the election period.

We will continue to follow the economic indicators as well as the earnings action of individual companies and sectors. If we notice a change afoot, we will make changes to the portfolios. As for now, we are prepared to digest the ample amount of economic data being presented this week.

- Ken South, Newport Beach Financial Advisor

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

.

.

.

Important Disclosures:

These views are those of the author, not of the broker-dealer or its affiliates. This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. All investments involve risk, including loss of principal. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

The fast price swings in commodities will result in significant volatility in an investor’s holdings. Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors.

Standard deviation is a historical measure of the variability of returns relative to the average annual return. If a portfolio has a high standard deviation, its returns have been volatile. A low standard deviation indicates returns have been less volatile.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Gross Domestic Product (GDP) is a comprehensive measure of U.S. economic activity. GDP measures the value of the final goods and services produced in the United States (without double counting the intermediate goods and services used up to produce them). Changes in GDP are the most popular indicator of the nation's overall economic health.

The Consumer Price Indexes (CPI) program produces monthly data on changes in the prices paid by urban consumers for a representative basket of goods and services (Source: U.S. Department of Labor).

The Producer Price Index (PPI) program measures the average change over time in the selling prices received by domestic producers for their output. The prices included in the PPI are from the first commercial transaction for many products and some services.

The "core" PCE price index is defined as personal consumption expenditures (PCE) prices excluding food and energy prices. The core PCE price index measures the prices paid by consumers for goods and services without the volatility caused by movements in food and energy prices to reveal underlying inflation trends.The ISM manufacturing index, also known as the purchasing managers' index (PMI), is a monthly indicator of U.S. economic activity based on a survey of purchasing managers at more than 300 manufacturing firms. It is considered to be a key indicator of the state of the U.S. economy. Formally called the Manufacturing ISM Report on Business, the survey is conducted by the Institute for Supply Management (ISM).

TNX is the ticker symbol of the 10 Year Treasury Yield index.