In last week's newsletter, I covered a few important points. The first point was that earnings have started off being pretty solid. The second point was that February, March, and April; in an election year, have historically proven to be a bit difficult. The third point was what tends to happen in an election year and, more specifically, an election year that follows a year that has been a good one. Now that we are in February, and have finished the first month of the year, several new statistics have popped up allowing us to see what the probabilities are for markets moving forward. But before I begin to go into what market index actions are starting to look like, I thought I would share some other observations that are coming to mind.

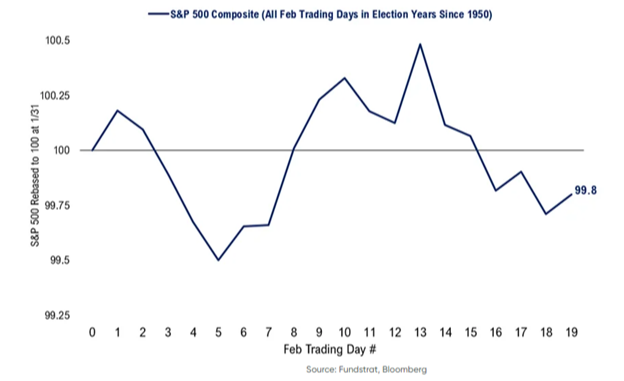

One of the first points that come to mind is the "strength" of the January rally. Many people would equate strength with the overall amount that the broad index has gone up or down, but besides this number I tend to look under the hood at the breadth of the advance. It is still clearly the case that the large-cap technology leaders seem to be leading the charge higher, but beyond that how is everything else doing? When I say everything else, I am referring to the broader Russell 3000, the Value Line Average, and the Dow Jones Transportation Average. These are not the indexes that are often tracked and reported by the broad media, but I follow them as they tend to send a different message than the S&P 500 at times. This seems to be one such time. As I had started out, technology remains the leading outperformer, but we are not yet seeing a breadth increase to new highs from these other broad indexes. It seems to be becoming more clear that seasonal factors could be holding true as they have since the 1950's. If we are to look at the action of all election year Februarys since 1950, this February is starting out as has historically been the case.

Election year seasonality proved to be fairly accurate last month in January, which makes a study of how the average election year February typically plays out. As this S&P 500 average action chart above proves, the bias tends to be initially down for February. Then we could experience a little more strength into President's Day before a continued consolidation. This would fit with the chart I showed last week of what monthly action tends to look like in election years. This backing and filling action could be quite healthy for the markets should it remain temporary and not show too much internal damage. See the monthly action once again below:

Thomas Lee of FundStrat gave an even more graphical representation this week showing what has happened historically when we are in a situation as we are currently:

Going back to 1927, these instances seen above dovetail with what we have experienced thus far.

The next logical question would be to dig into why the markets could be showing some difficulty in this period, this year. As I have said before, the underlying action of the markets should be based on earnings. If earnings are rising, and rising more than what expectations are, then this should give a reason for markets to go higher. As can be seen below, the trough of earnings growth seemed to be in the first quarter of 2023 and since then has continued to show growth and expansion of companies showing increased earnings. We are still not halfway through Q4 2023 earnings and we are already at a good number.

This last quarter of 2023 EPS results season has thus far been positive with 79% of companies beating by an average of 6%. This is with only 32% of the S&P 500 companies having reported thus far. Last week was the heaviest week of earnings for the quarter and it started out shaky but finished strong. So strong in fact it was the 13th week of positive market index action out of the last 14 weeks! It ended with the January jobs report. I don't tend to pay attention to individual economic reports, but this one was a whopper! The number came out almost double what the street was looking for. Many have said that this was only because of seasonal factors, but I looked at the action of interest rates and the action of the US Dollar vs. major foreign currencies and no matter how you slice it, the markets took notice! So, the next logical question is what has happened when the markets have had a fairly aggressive upside move for a period of 14 weeks? Going back to the bounce that started in 2022, the consistency of the action is really quite alarming:

Circled in yellow are the digestive periods that occurred following strong moves to the upside. Since the internals are beginning to show some weakness, could it be that we are about to experience a digestive phase once again? I believe this could possibly be the case. I believe that this time the market pullback could be catalyzed by the comments out of Fed Chairman Powell from his last Wednesday’s Fed meeting that was further confirmed by his appearance and comments on 60 Minutes this past Sunday. I believe that he is quite possibly taking a bit too long before providing the beginning of interest rate cuts. Victor Cossel of Seaport Research I believe said it best this week, “Recent hawkish Fedspeak raise ‘policy mistake’ risks as Fed speaker commentaries suggest a hesitancy to cut despite PCE nearing if not on target. We think the Fed backtracked on prior comments that cuts could start before hitting the 2% target.” This made me take a further look at what is going on throughout the rest of the world. On Wednesday of last week, January 31rst, there was an article in the Wall Street Journal titled, "Europe Economy Falls Further Behind U.S." Headlines tend to be a little dramatic, but this one dovetailed exactly with what was reported two days later with the US labor numbers. In the article they started with, "Europe's economy stagnated in the final three months of last year, expanding a divide between a booming US economy and a European continent that is increasingly left behind." They stated that this was because of the geopolitical issues and the crisis in the Middle East creating gummed up cargo traffic through the Red Sea. Not only is this slowing supply chains, but also cutting off orders from many purchasers across the globe due to the lack of confidence in getting much needed goods.

The US is clearly not experiencing this same issue. Last week we got the PMI numbers on the US industrial economy. Not only are they appearing to bottom, but they are rising from a level below 50 which has led to a strong equity market 95% of the time. Thomas Lee and his team at FundStrat put together this picture of how the PMIs seem to be bottoming and turning higher.

This brings me to my last chart to share. This is an illustration of what the earnings of the S&P 500 tend to do after a bottoming of the PMI's. If this truly is a bottoming of the PMIs, then the increasing in the earnings of the S&P 500 could prove to be a precursor to further advances of the markets later in 2024.

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

-

-

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.