The market does not “need” a catalyst to fall (or to rise), and narratives explaining why the market does what it does are often only clear in hindsight. There could be any number of factors that lead to the pullback that I keep on warning of. It could even be a combination of reasons: liquidity drain, higher than expected inflation, higher interest rates, geopolitics, politics, banking crisis, recession odds going up, etc. Interim high points usually form when it feels like prices can only keep going up, which is one of the many reasons I think extra caution is warranted here.

One email that I got last week asked what the catalyst would be to begin the digestion that I expect is coming in the stock market. I did touch on this a little a few weeks ago but it bears repeating. I do not believe the stock market necessarily “needs” a catalyst to fall, at least not one that is going to be obvious in real time. While it is always easy to look back with the benefit of hindsight and ascribe a narrative to why the market did what it did, it is not as simple to do so when living in the moment. As I’ve pointed out, the S&P 500 topped in late 2007, almost a full year before the heart of the Global Financial Crisis arrived in earnest and everyone became aware of the troubles the economy and market faced. At the top, however, those issues were not nearly as obvious, which is why books and movies have since been released chronicling the stories of those few with the foresight and nerve to bet big on the collapse.

While I believe there is the potential for any forthcoming decline to ultimately morph into a major bear market, I think it’s too soon to actively bet on that happening unless one is singularly focused on possibly having his or her own “Big Short” career-defining moment. I continue to believe the probabilities favor getting some sort of pullback here soon, with that easily being a 7-10% drop without really changing much about the bigger picture. If such a pullback occurs, I will then decide how to proceed next depending on the characteristics and structure of said decline. As can be seen below, the market as referenced by the S&P 500 Index seems to be progressing in a quite orderly fashion and bouncing up off a well-defined support line.

I will identify what I feel to be important price levels / zones, and then watch how the market reacts to them. If you do want to talk catalysts, I can name several that could be assigned responsibility for any market correction that may arrive. The likeliest culprit would probably be a scenario where inflation takes back off to the upside and does not allow the Fed to cut rates as has been the expectation since last fall. That would likely push longer-term interest rates up higher at a time when consensus seems to be that they will fall. Such an event would catch many positioned incorrectly, loaded up on both stocks and bonds. I actually think this is what “could be” the major unknown that becomes knowable by measuring inflation vs. growth, taking into account the money supply that I often reference.

For all the micro-managing the Federal Reserve receives, I think they have actually done about as good a job as they could have in terms of fighting inflation and subduing their impact on the financial system. Yes, they were too slow to take inflation seriously and raise rates, but since doing so it is hard to argue that they haven’t done an admirable job. They have been patient and as I had said last week, it has been 10.8 months since they have taken any action at all rather than “talking” interest rates higher or lower. Inflation, at least the way they measure it, has come back down toward their long-term targets even if it’s not all the way there yet, and it so far has not crashed the economy in the process.

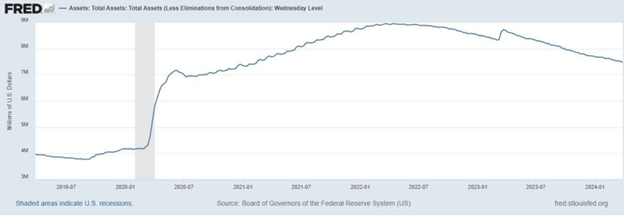

Meanwhile, they have spent the past couple of years reducing their balance sheet, which makes the rally off of the October 2022 low the more impressive since it has come while the Fed has been performing quantitative tightening rather than easing. I want to stop for a moment and address this term “shrinking the balance sheet.” This is a fairly esoteric term that might require you to do a little research on your own. It involves money supply and is fairly theoretical. Please take some time and study this if it is unclear to you. Still, there is always the risk that letting the air out of the financial system, so to speak, could spark another rough patch. If nothing else, it calls into question how much extra help the Fed and the government can give the markets and economy if it is needed. The amount of “help” the Fed and government are providing can be seen in the graph below from the Fed:

My fear is that eventually, the draining of liquidity from the financial system may finally catch up to the market. The Federal Reserve’s balance sheet exploded higher back in 2020-2022 during the government’s COVID response and has since been slowly retreating back down as seen in the graph above. This removal of liquidity is likely at least partially responsible for the rockier markets of the past two years, yet there remains plenty of room for this drain to continue while also giving the Fed less runway in the event they need to stimulate the economy again. Hence the reason for the excessive focus on economic expansion vs. inflation that we are all too focused on currently!

Politics (and the public’s response to them) could also play a role in a decline, especially in an election year if something surprising were to happen (like one of the two major candidates unexpectedly being unable to run). Geopolitics are ever a threat, as well, particularly in this environment with two major wars making headlines. Both of these due to the fact that they are immeasurable in timing and scope. We can’t forget about the banking issues, either, which have not suddenly gone away simply because they are not making the same kind of headlines as last year, instead we keep only hearing about exposure to the commercial real estate side. And, of course, there’s always the possibility of a real Black Swan event occurring, which, by definition, is not predictable. The Global Financial Crisis was not a Black Swan. Neither was the Dot Com Bubble bursting. This appellation should be reserved for truly unexpected events, such as September 11th or the COVID outbreak.

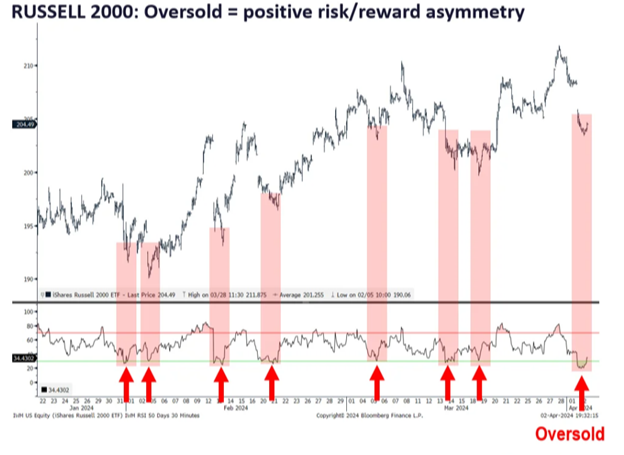

My point is that there are any number of things that could produce more vigorous selling of stocks. However, as I have said before, I do not really spend much time worrying about it or attempting to predict the future. There are ALWAYS risks present, and it’s usually only when those risks appear to not present much of a threat that tops usually form. Conversely, it is usually when everyone is only focused on the risks that bottoms form and rallies begin. Bottom Line the past two weeks and new quarter have seen some of the worst selling of the year. This is also being capped by April 15th, Tax Day, and the fact that gains were made in 2023 and eventually investors need to pay the piper! Recently, in the S&P 500, a lot of trading took place within the 5050-5200 region over the past several weeks, so now the lower end of that zone becomes important as support. A breakdown below 5050 could be our initial signal that some sort of top is in place. Now that the S&P has traded up well within my 5200-5400 “target” zone, I will continue to be even less likely to chase new long stock trades since I question how much upside potential is left relative to downside potential. At the same time, when the small-cap index has gone to low points on its Relative Strength Index, buying opportunities have presented themselves. So here we stand currently:

How this plays out is yet to be seen, but I reserve the right to sit on my hands until after Tax Day. If you have any questions, please don’t hesitate to ask. As always, we have the time and desire to help any way we can!

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

-

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.