As I compile the information for the newsletter this week I felt it important to give you some color on what I am seeing. Besides paying attention to general prices of all asset classes, and their directions, I take a look at the “tone” of the articles in the press as well as the research comments from market commentators like FundStrat and Ned Davis Research. But to begin with this week I wanted to address the articles over the weekend that I found of value. First off was an article in the Review section of the Saturday Wall Street Journal. It was titled, “Walking Longer, Not Necessarily More, Shows Big Health Benefits.” Here is the link: https://www.acpjournals.org/doi/10.7326/ANNALS-25-01547.

I felt this was super relevant for all of us and a great article with no political bias! I understand, this isn’t why you picked up this week’s note, but I felt it was worth providing. The next thing I noticed was the lead article (entire whole front page) of the New York Times Business section, Saturday as about how the top 25 movies of all of 2025 (in cost and well-known actors). To be honest, I really don’t care about this at all, but I do find it relevant that this is all they can pull out for the front page of the business section! Sort of speaks to the fact that nothing really is changing, AI is still leading, and there were no more new Jamie Dimon cockroaches this week! Speaking of Jamie Dimon and the debt cockroaches, there was a comment by the new Global Bond King Jeffrey Gunlach on Monday morning. According to Gunlach, “The next big crisis in the financial markets is going to be private credit.” He feels that the investment industry’s push to have retail investors, like yourself, invest in these illiquid, private pools is the kiss of death and that this is highly similar to the debt crisis of ’08-’09. This is why I keep bringing up the amount of cash on the sidelines and strange way that it seems to keep on finding a home in new and different places.

On the more important news front, I found in Barron’s the article by Randall Forsyth quite interesting. It sort of references back to the Blue Owl article last week and the Jamie Dimon cockroach comment as well. He quotes Dan Fuss, the 92-year-old Vice Chairman of Loomis Sayles (the well-known bond house). He refers to him as the “Buffet of bonds.” He made comment about the “if they knew the credit.” He was referring to the immense amount of debt, particularly to the data center space. He thinks data center debt is too speculative as a result of the future revenue streams being too uncertain. What I thought was most interesting was his comment that the yields aren’t enough to compensate for the risk being assumed. This, I believe, speaks to the immense amount of cash swirling around that simply needs a home. Later in Barron’s, the institutional interviewee was Avery Marquesz, the Director of Investment Strategies at Renaissance Capital. I believe that this is another angle on the concept of where cash is going. She seems to feel that we are about ready to have a large influx of IPOs in 2026. I strongly disagree. Why? Simply because of the current state of the market for private deals in both debt and equity. If there is an almost unlimited amount of money swirling around in the private space, and as Fuss says, at yields that don’t reflect the level of risk, why would a company want to go to the heavily regulated public markets? I think this is super super important in evaluating valuations and global markets in general.

Today’s Market Situation

Since the beginning of October, the US Equity market has gone virtually nowhere. Maybe on a day-to-day basis it has had extreme volatility, but on the basis of the overall price action it has gone virtually nowhere. Here is what we have experienced:

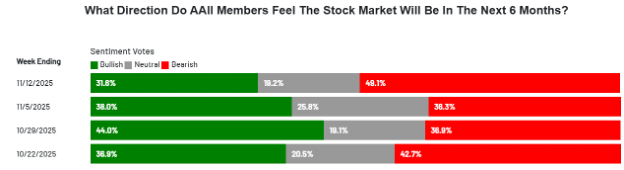

There could be a variety of reasons for this. Many will choose to attribute it to further Tariff negotiations, political discord, and the US Government being closed. These may all be factors, but what I find most interesting is that neither the upside nor the downside has been able to get a firm footing in their directional move. So, I look at the internals of the market and what I find is a very very bleak opinion of the market by investors. Going to the AAII website, it can be seen that the polled investors feel that the market could be negative for the next 6 months. Here are the results of the survey, please note that the red section is the negative (bearish) investors. Just two weeks ago 44% were positive and as of last week, this is down to 31%. This is a quite large reversal:

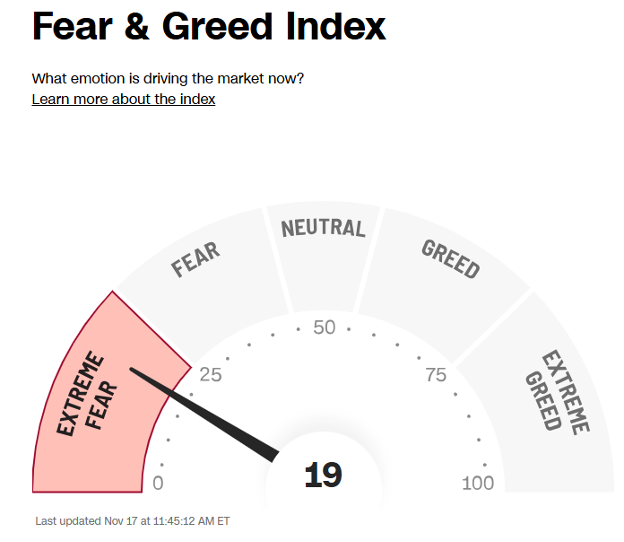

The next survey that is being recognized is the CNN Business, Fear & Greed Index. I don’t give tremendous credit to this as it seems to have strong political bias, but I do have to give it some level of respect due to the extremes that it is currently at.

The reason I bring these two studies up is that I find it really quite fascinating that the broad US markets are with 5% of all-timer highs, which were hit last week, and they are at emotional lows in these studies that would ordinarily reflect a market that is in a complete tailspin. As seen above, the S&P 500 currently sits almost right where it did at the beginning of October. We are therefore going on six weeks with no real progress made in the index even though it has swung around more than 20% in that time. Attempting to trade the news is a losing proposition in the long run. The presumed end to the longest government shutdown in history was the purported reason for the market's bounce into Wednesday, though of course once the two sides came to an agreement and officially ended that shutdown, stocks sold off.

Instead, there has to be something else there. I believe it is the fact that the US Fed really shouldn’t lower the interest rates again in December since aside from labor, there is quite strong economics in corporate America and other studies of business. The issue is that both the 10-year and the 30-year interest rate markets are saying that the economy is strong, and that inflation is not going down. At the same time, the money managers within the institutions are having a dreadful time. I will go into this in a moment, but let’s take a little bit more time thinking about the here and now.

Thomas Lee’s best guess as to what the end of November will bring to the markets is illustrated below. Although there has been lots of turmoil politically, he is still quite positive on the expectations for the month of November. His expectations have been for a choppy first couple of weeks of November, but a finish up around 2.5% or 200 points into the end of the month:

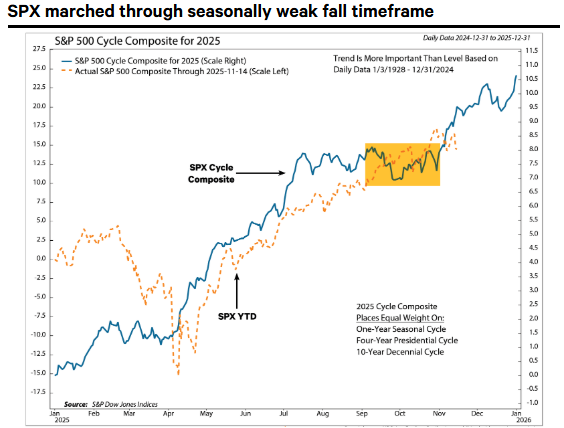

What I believe to be an even more important statistical issue moving into year-end is the S&P Cycles that I often reference. I use the 1-year, and the 10-year, but right now I believe the 4-year Presidential seems to be the one we are most closely following this year. Please notice the yellow boxed area in the chart below. This dovetails almost exactly with the expectations out of Thomas Lee and FundStrat. Also notice what tended to happen in the second half of November and December. This is what some are greatly expecting:

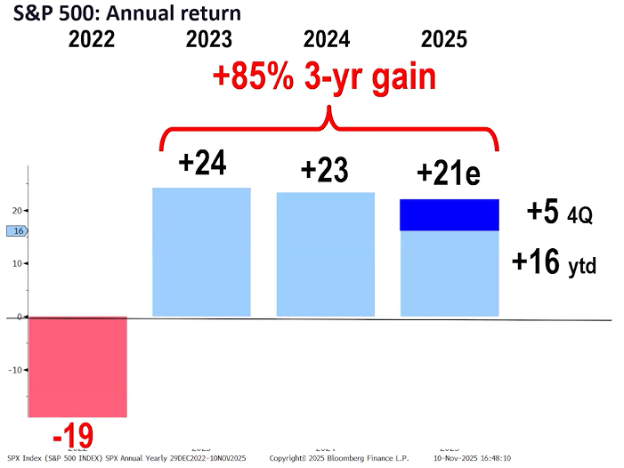

In reviewing the performance of the overall market, it had a very bad year in 2022, as all will remember as a result of the Fed tightening 6 times consecutively to try and stifle the inflation created by the mass helicopter drop of money onto the economy due to COVID. The tightening hit all industries, and this time was clearly proof of that. Then they (the Fed) realized that it was maybe too much too quick, and they started to ease. This provided much needed liquidity right at the time that AI started to blast off. As a result, there was a 24% up year in 2023, a 23% up year in 2024 and even thought this year has been “Trumped” by virtue of many never before seen political and domestic economic tactics- which have all been quite positive, the year has been strong as well. This year has been up over 14% and if historical statistics are to hold true, the year could finish even stronger. Here is what FundStrat’s expectations are:

To me, this is where things are getting interesting going into year end. First of all, as I have said time and again, there is $7.7 Trillion cash on the sidelines needing a home. This has created the birth of a huge expansion in Private Equity and Private Debt financing, but also, the amount that is sitting on the sidelines in short-term treasuries is generating enough cash flow to fuel additional price movement in equities as it finds a home there. This has been a global phenomenon as even though the US equities markets are in the throes of a three-peat, the foreign markets, both developed and emerging markets have actually even done better than the US. This is the first year for this to happen in 16 years. I think this is quite a global statement. But wait, I thought the whole world hated President Trump’s tariff and economic policies? Well, according to the money, this isn’t what is really being seen.

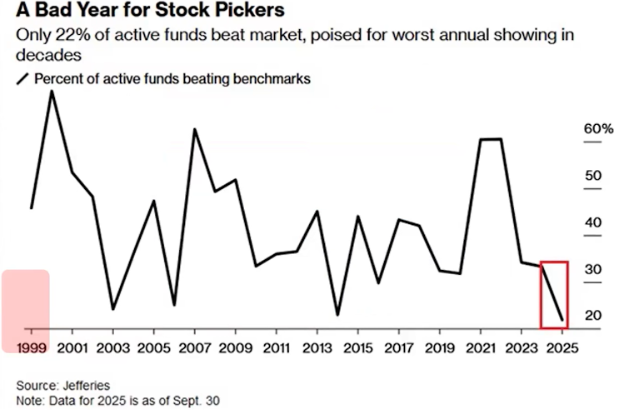

This all brings me to the “how” and “why” there could very well be a strong rally into the end of the year. If we are to look at the performance of the majority of active mutual funds and money managers, currently, only 22% are beating the indexes right now. The overconcentration in the top few names have been a requisite to beat the indexes as they are dragging the indexes higher. Therefore, there could be a “performance chase” going into year-end. This is when the funds have to gobble up the leaders in an effort to get an end-of-the-year push in their performance. Here is how truly few are beating the indexes over time:

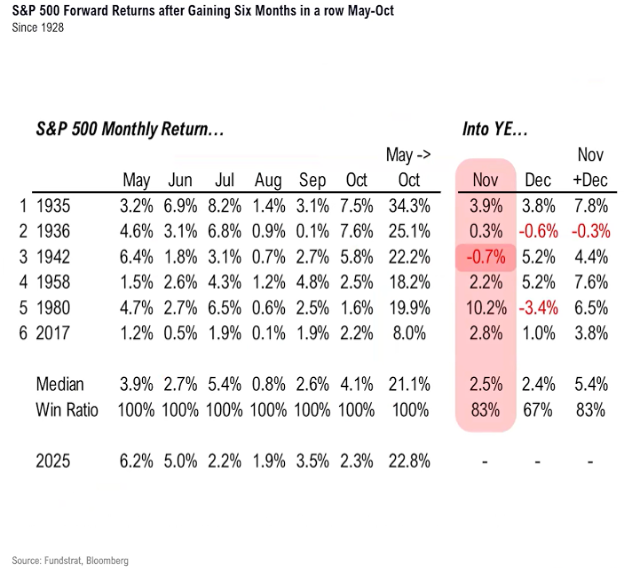

Looking at the statistics that support this as well, I am going to show the chart that I had included last week once again. Going all the way back to 1928, there have only been 7 times that the markets have been up over 10% from the period May-October. This year up 22.8%. When this happens, what has the market historically done in the last two months? It has been up 83% of the time and an average of 5.4%. This is where Thomas Lee and FundStrat get the 5% push into year-end:

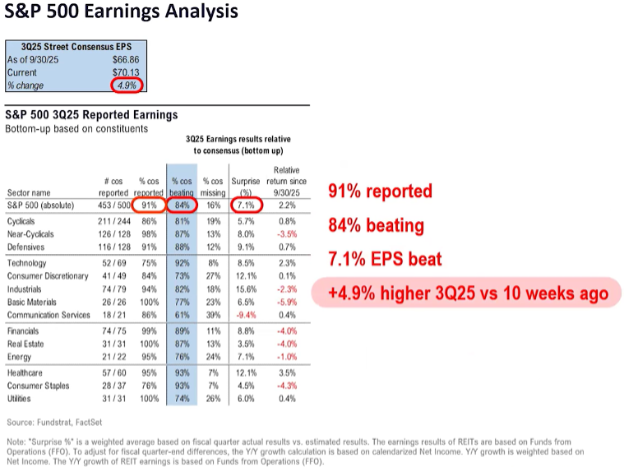

The next logical question is whether the current economy and company earnings support this being a true possibility. In looking at the earnings for the third quarter, 91% of the companies had reported earnings by the end of last week. Of those 91%, 84% beat the expectations from analysts, and beat them by over 7%! This is an acceleration from the previous numbers a few weeks back. I think this is really important, particularly when the negative concept of Tariffs rages on in the media.

This week marks the first week with a full slate of economic indicators. Monday started with the Empire Manufacturing number (New York Industrial measure) coming in up 18.7% when the expectation was 5.8%. This is a quite significant disparity. Construction spending increased month over month and this was expected to be lower. These are not “game changers” by any sense of the word, but they do continue to confirm things not getting worse. The big data point of the week will possibly be the earnings by the juggernaut chip company after the close today.

We are within a stone’s throw of old highs, in the midst of a digestion, and the news is a plethora of negativity. This is a Wall of Worry like something we seldom see. I don’t know which way the market will settle but given historical statistics and underlying corporate economics- baring the few debt cockroaches, things look OK. We will have to wait for more answers, but with this being the week before the shortened Thanksgiving week, I don’t see a lot to move the market much. Baring some Black Swan, this could me more of the same before a hopefully strong end of the year. Oh, and just in, Morgan Stanley ups its year-end target for the S&P 500 for 2026 to 7,800 due to robust earnings and AI-driven efficiencies. This would represent an additional 16% rise. What are investors seeing that Morgan Stanley isn’t? Welcome to the market!

- Ken South, Tower 68 Financial Advisors, Newport Beach

-

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The S&P 500 is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States. Indexes are unmanaged and cannot be invested in directly.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

Data sourced from Bloomberg (2025).

Stock investing includes risks, including fluctuating prices and loss of principal.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Bonds are subject to availability, change in price, call features and credit risk.

Government bonds are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

Bond yields are subject to change. Certain call or special redemption features may exist which could impact yield.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

Alternative investments may not be suitable for all investors and should be considered as an investment for the risk capital portion of the investor’s portfolio. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

LPL Tracking #827459