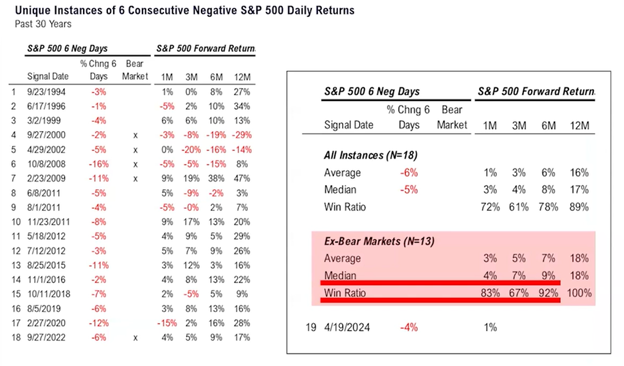

On Friday I penned a Special Report. I felt that there is enough negative news swirling around that it would be helpful to quantify and compartmentalize the biggest issues that are being bantered about by the media. Stubborn & persistent inflation, ensuing lack of interest rate cuts, equity valuations after a straight run since late October last year, and a widening number of international wars / snafus that are coming to our shores in terms of protests and racial discrimination. The cover of Wall Street Journal from yesterday was all about the protesting frictions on campuses. Just when we thought we had enough on our plate, our illustrious governing body approved another massive $95 Billion aid to Israel and the Ukraine when we are dealing with continued unsolved issues like homelessness, immigration and lest we forget the Hawaiian fire devastation (just to name a few). So clearly, after such a big runup in stock prices, it shouldn't be too much of a shock that the digestive period that I have been talking about seems to be in full swing. The decline that we have experienced brought about 6 straight days of declines in the S&P 500. This is VERY uncommon but can be very telling within an ongoing uptrend. Notice in the chart below, that in the last 30 years, 6 & 12 months out the markets had not only reengaged their uptrend 91% and 100% of the time respectively:

This week should prove to be another interesting week with a slew of S&P 500 company earnings reports, The Personal Consumption Expenditures indicator (PCE), and a fresh GDP number. So, with all of this swirling around, what is it that one should look for to tell us that it is the beginning of something worse or getting close to the end of the negative price action? To answer this, I called up my favorite analyst, Ari Wald, Chief Market Technician Oppenheimer & Co., for his comments over this past weekend. It seems to Ari that it is a function of both price and time. The price could come down to a certain level before bouncing, and or the move lower could exhaust itself due to the amount of time that it remains in this corrective phase.

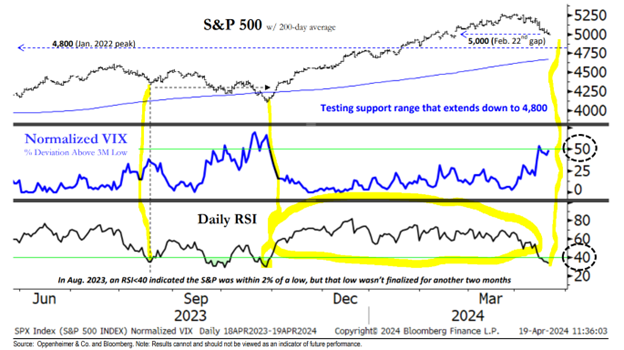

The price of the S&P 500 should find its bottom somewhere in the 4,800-4,900 range (roughly 4-5% below where it closed out last week), and this could happen after some backing and filling in the next few weeks. It should also be noted where it “could” come down to. The index could test the point at which it broke out to new all-time highs in January. The RSI oscillator, at the bottom of the illustration, is coming right down to where it has bottomed out in the past when the price of the index hit its low points. It then resumed its uptrend. I've highlighted these points on the chart below so you can focus on them. I also want you to focus on the length of time that the RSI has been above the green line since October and therefore probably needing a digestion:

It may seem strange that we are looking for a bottom in this short-term decline since the broad index is really only down around 5% since late March, but if this is just a correction within a continuing advance then it should reach a level of being oversold on a short-term basis and ramping back up. Ari points out that his work becomes increasingly bullish as summertime nears because it has been shown that first-term election years are typically strongest between June and August.

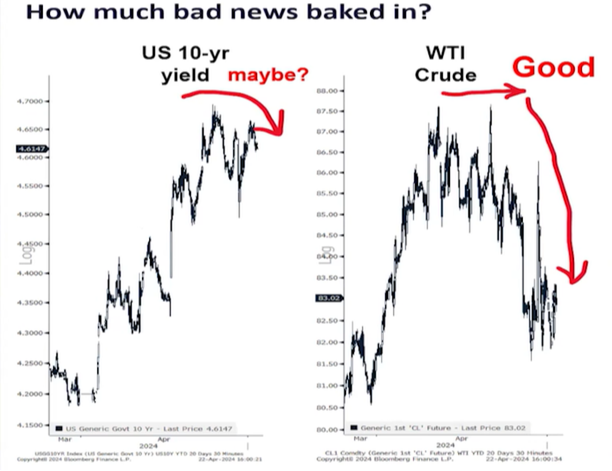

As I see it, I am paying particular attention to the yield on the 10-year Treasury and the action out of US Dollar / Gold, Oil prices and the response to these in the price level of the S&P 500.

The 10-year seems to be locked in a tight range at 4.6% and gold broke down from its strong advance on Monday. Oil prices were feared to ramp up toward triple digits as the Middle East tensions in Gaza spread to Iran and Israel, but this-at this point-seems to be more saber rattling than anything else. I don't say this to minimize the loss of human life or the racial profiling, but when Iran shot off a great number of drones and missiles and then Israel again retaliated and Iran said they were done, oil has settled in the low 80's and seems to be back to reflecting strong economic activity instead of Middle East friction.

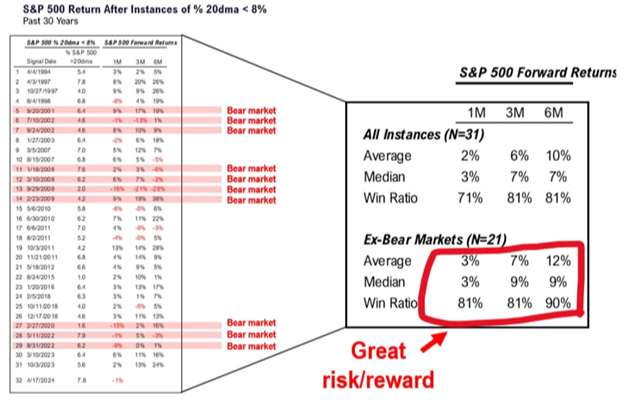

If we look back at measuring the level of the decline experienced thus far, by measuring the percentage of companies in the S&P 500 that are above their 20-day average price, it can be seen that we are pretty much at a place where bounces have occurred. I used the time span going back to the "big low" in late October of 2022. Also, Thomas Lee of FundStrat put together a table that shows the times since 1994 when the market has come down to this level. What is interesting is that there is a very high probability that the markets will be higher 1-month, 3-months, and 6-months later. Since this correction is not occurring in the face of a bear market, this could be a good indication of what to expect in this first-term election cycle year.

The next chart is the action of the top in the 1-year forward inflation measures. Maybe it is a coincidence, but the market seems to bottom at close to the same point as the inflation measures hit their high. Since inflation tends to correspond with interest rate increases, and higher interest rates have seemed to be the nemesis of the stock market, the graph above and the one below tend to mirror each other. Inflation has been the fear that has created the major bottoms in the advance since October of 2022.These fears are now high once again with inflation expectations being 4.533% as seen below:

It would be remiss of me to not address the fact that many market prognosticators are stating that "the" top is in, and that even though we might be experiencing the beginning of the end of the inflationary spiral that a larger top could be in place. I think we need more information before we can assume this to be the case or not but, then again, I’m not in the business of trying to sell newspapers. What I would look for first is when the market bottoms and recovers, if it can't better its previous highs then there could be some more digestion needed before it can ultimately continue its advance. Also, some deeper drivers would need to be in place as well:

- The Fed would need to shift to outright tightening instead of easing should inflation stubbornly continue to increase.

- The Economy shows signs of being weaker than expected signaling a recession is looming.

Neither of these seem to be in my expectations, but we will be sure to be on the lookout for them. To be very short-term, the last major down day was Friday, and if the current market action can hold the lows of Friday, and close above the highs of Friday we could be in the process of hammering out the interim bottom. Again, if you have any questions, please don't hesitate to reach out to us directly and we can work with you to make sure you are comfortable with how your situation stands.

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

-

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax