View the Video Here Read/Print Newsletter Here

![]()

2023 has been quite a ride. The S&P 500 checked off many boxes early on and held true to probability expectations afterwards. The first 5-day rule. The first month rule. The "January Effect" rule, and so on. The market rallied until late July, and then pulled back into late October, as is the norm. Throughout the year I have been providing statistical data of what "usually" happens when the market acts as it has, and to be honest, it is a little scary when things seem to work out so darned textbook! Before I go into exactly what I am looking for next, into year-end, I thought it would be helpful to provide clear illustrations of what we have experienced. For some this will be redundant, but I believe it is important to keep things fresh on one's mind:

- The market was in a positive progression going into COVID.

- COVID hits and the market swoons.

- The Fed throws Trillions of dollars at the market, and this fuels a massive rally that continues into 2021.

- The Fed comes out in 2021 and says, "Hey, we are glad that we were able to rescue the economy, but things are a bit ahead of themselves, so we have to increase interest rates from 0% to stifle inflation.”

- November 2021 the Fed tells us when they expect to start raising rates and the market (a discounting mechanism) starts to digest the massive up move from March of 2020.

- 2022 we experience a painful bear market. Not a bear market based on a structural issue like the Dot Com Bubble or the Great Financial Crisis, but rather a digestion due to things moving too far too fast.

- 2023 proves to be a recovery for the equity market, even though interest rates are hiked voraciously, fueled by liquidity, labor, wages, supply chain recovery and numerous other economic benefits.

So, let's take a look at where we were, what has happened of late, and what it appears we should experience:

As can be seen above, a big move off the November 2022 low, an initial bounce, a pullback into March to test if the bounce was real, a resumption of the up move up into late July then a three-wave decline, again, very textbook:

Once the three waves were over and exhausted themselves the market then gained strength, took some time to catch its breath and broke out from the high point it had put in at the beginning of October:

Now that the market has begun its breakout from the channel of the three-wave decline, it is time to evaluate what "should happen" to facilitate a continuation move higher into year-end and possibly the first half of 2024. The most important things that I have focused on are three major components:

- Earnings reports- needed to be strong, showing that the hike in rates, although necessary to stifle runaway inflation, didn't force the S&P 500 companies into a downward earnings spiral. So far, we are almost completely over the third quarter earnings reports, and we have recognized over 80% of the companies beating their earnings expectations by in excess of 7% on average. This is a pretty consistent and broad-brush positive earnings season.

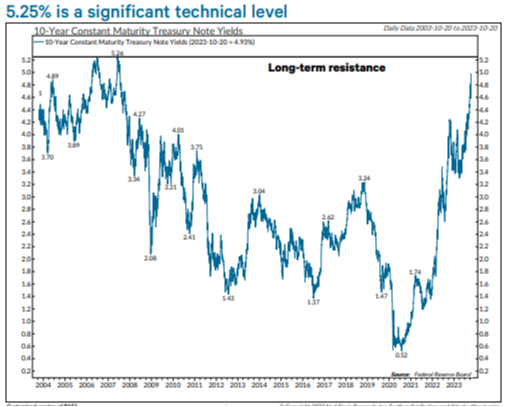

- Interest rates- needed to stop moving up at the rate that they have been for the year. The 10-year US Treasury rate peaked on October 27th, right when the equity market stopped pulling back and started recovering.

Since bonds tend to be a trade-off to stocks as an investment option- particularly when ultra safe US Treasuries under 1-year in maturity are paying over 5%, this sugar high in bond interest rates had to top out. This caused some additional money to be available for the equity market to fuel the next advance.

3. Last week I talked about the "Elite Eight" stocks that were, on their own, virtually pulling up the entire performance of the S&P 500 companies. This number really needed to broaden out to small and medium companies and across to other industries. This has happened in the last week.

So the question now becomes, if these three points are all occurring could this be the start of a new leg higher in the market? I think it could be just that. If true, and if it is to be an upside "measured move," just as the three waves of the downtrend in July-October happened, the current trading target could be somewhere close to 4,700. How do I get to this? To quote Jeff Saut, the old market sage of Saut Research:

- First leg- ~4,100-4,391 for a gain of 291 points.

- Second leg- add the 291 points to the beginning of the second leg around November 9th at 4,393, and one gets to 4,684.

- Third leg- this is yet to be determined based on the finish of the second leg.

If the three legs seem to pan out, and the year-end rally manifests itself, the rally could be quite impressive. If we take a look back through history, going all the way back to World War II, this year's market appears to be an analog that is rhyming quite well. See the chart below, courtesy of Bespoke Media:

What gives me a level of confidence that this rally could really happen is the widening in breadth of participant companies in this current rally leg. Instead of it being narrow and focused across a certain few (the “Elite Eight”), it has actually increased to over 50% of the companies in the S&P 500 trading above their respective 200 day moving average price. In going back to late 2022, this has proven to be a pretty good backdrop for continued market advances. To quote my friend Ari Wald,

"The quality of the next leg higher should help gauge whether a market top develops in early 2024 or late 2024. For instance, OUR BASE CASE IS FOR A NEW S&P 500 CYCLE HIGH IN THE FIRST HALF OF ‘24. However, a new high undermined by fewer than 60% of NYSE stocks above their 200-day average would warn the cycle has topped. Conversely, a re-broadening of the advance would extend the cycle’s duration by another 1-2 quarters, in our view."

I will end with a quote from the Goldman Sachs Economics team for the week ending 11/15/23. This was almost entirely fueled by equity inflows of +$23 billion. Generally, long-term flows seem like they are ready to reverse from outflows for the past 52 weeks towards stabilization or even inflows. See the chart below. Notice that the circles at the top represent a change over to fund flows coming into the equity market. A vertical red line is connected to the circle that represents this change in fund flows. The subsequent reaction of the S&P 500. It is clear that these fund flow changes have come at a very opportune time to invest in the US equity markets.

In closing, have a very very happy and fun-filled Thanksgiving!

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

-

-

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues witha qualified tax advisor.