With no rabbit being pulled from the proverbial hat from last week’s broad trade negotiations, the markets remain hostage to the unknown and unquantifiable. This should keep the markets highly volatile for at least the near term. I found it interesting that Klaus Schwab, after 50 years at the helm of the World Economic Forum board of directors, stepped down at this time as well. What does this mean? I can’t really say, but when the whole world trade situation is in a state of flux strange things begin to occur. But I have to wonder if the trade issue is really “the” issue.

I also found it interesting how the trade situation is starting to unfold. At the end of last week, it was publicized that the US would focus on those countries that were acting as a “conduit” for Chinese goods that were being funneled to US consumers. This seemed to be a bit of a hot point as China warned on Sunday evening that they would take “extreme measures” should their trading partners align themselves with these US intentions.

I also noticed an interesting article in the Wall Street Journal Monday about the “delisting of Chinese companies” from US exchanges. This seemed to be an interesting bargaining tool as this would be a further stoppage of Chinese access to US capital. There was a movie, that is still up on the services titled, “The China Hustle.” The movie is about a bunch of analysts that went to China to sort of put boots on the ground in looking at a few Chinese companies. Turns out one of the ones they looked at was a $150 Million company that was a total sham. Since Chinese companies don’t have to function with US GAAP rules (General Accepted Accounting Principles) it doesn’t come as a shock that possibly we aren’t being told truths about the companies that are flourishing on US exchanges. Imagine if the Chinese capital markets didn’t have access to US investors. Would be pretty bad for them.

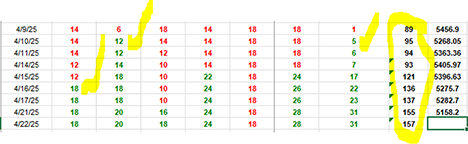

Volatility settled last week on the market side after an aggressive waterfall decline. I’m not saying that global equity markets are ready to rally, but rather that the waterfall decline might not continue to move down. Markets volatility settling down but not recovering is part of a bottoming process. As Ari Wald said so eloquently last week, “The markets may be bottoming but might not quite pegged the bottom.” I find this somewhat comforting as there are many companies whose market prices reflect a negative market, not a negative forward expectation for their businesses. Last week I showed a chart of the morning study that I do every day. I found it quite interesting that my “cumulative number” has risen virtually every day since April 10th. I also found it interesting that on Monday our number actually rose. I think this speaks to the internals beginning to separate from the overall price level of the indexes. I have circled my cumulative number and then put a check mark next to the number of sectors that have turned positive and the percent of equity mutual funds that are beginning to turn up.

One of the latest investment fads is “Private Credit.” This is money being lent to private (non-publicly traded) companies. Since many companies that are very lucrative are the target of large investors who are trying to participate in companies prior to them hitting the public markets in an IPO, so is the access to capital from these companies. They seek this private credit as it is incredibly difficult to evaluate their true debt paying capabilities when their business is nascent for growing dramatically. This private credit is dying up a bit as markets are beginning to be concerned with overall economic growth due to an unclear understanding of the impact of the tariffs on many industries. Risk is being considered now. The world leader, Blackstone, was also written about in Monday’s journal as a huge horder of cash that could be used to hunt companies that could be considered babies being thrown out with the bathwater. As a larger financial company, rallies in the price of Blackstone could be considered sort of an indicator that it could be considered risk had passed. Besides Blackstone, look at the amount of cash that is still floating around looking for a home that is more profitable than short-term US Treasuries. Here is where money market balances are currently sitting:

At the end of the day, if tariffs create inflation and the Fed feels that they could be longer lasting, then the Fed would adjust interest rates to alleviate the issue. Given that the tariffs are a negotiation tool by the current administration, it is believed that the negotiation should end, and a quantifiable outcome could be understood relatively quickly. Therefore, the inflation argument is not really of any importance longer than a year out. This is why the Fed stays focused on employment as their primary inflation gauge. It is far more difficult to hire and fire employees, so Fed believes that employment is a far better way to project business expectations rather than tariff negotiation.

So, the dominos should fall like this: tariff expectations adjust how businesses see their future expansion trends. Businesses then hire or fire based on these expectations. The Fed attempts to either provide access to capital (lowering interest rates) or curtail borrowing of capital (raising interest rates) to keep the overall economy on an expansion continuum that it sees best for stable growth without excess inflation. The bond market will respond to economic weakness. Yields should come back down. One of the best measures of this strength or weakness argument is the slope of the yield curve. If the curve is steep, short rates are lower than long rates, so this implies no recession. If longer rates start to drop to a level at or below shorter rates, an impending slowdown is at hand. Here is where short-term rates are currently sitting:

Please note that since May of 2022, short rates have moved from under 1% to over 5%. This is a very dramatic rise in rates / cost of money, and I believe is the reason why stocks have become considered overvalued- relative to bonds and have catalyzed the current selloff. I don’t believe that tariffs themselves are the cause of this market selloff. I’m not saying that they are not a catalyst or that they don’t create uncertainty, but the market, on many measurement metrics, was already overvalued.

Why this is important is that when the market is overvalued (or in retrospect appears to have been), or it has run up a lot, it is vulnerable. As soon as the Fed began raising interest rates this risk began to rise. Now, that being said, there are many companies and industries that are not affected by interest rates- directly, but when the overall market becomes affected, and these companies are major components of indexes, then they become affected. This is also why it often doesn’t seem to make sense that great companies are dropping in their per share values when their business is flourishing.

Netflix is a case in point. They came out with earnings and revenues far greater than the analysts were expecting. This was on the heels of two days prior they publicly announced that they expected their revenues to double between now and 2030 (five years). Yet, the stock did not reflect these very positive projections due to its weighting in the market indexes. Since our markets have become progressively more indexed due to institutional money pools, even really great companies, that are doing really great, don’t act great if the index itself declines.

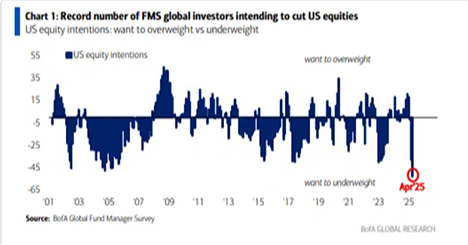

So, how are companies doing so far for 2025? Prior to the start of the quarter, Bloomberg’s bottom-up estimates put analysts’ expected earnings growth at 6.8% from a year earlier. As of last Friday, Q1 earnings growth for the benchmark S&P 500 is 6.8% on the back of 6.2% revenue growth. The five firms (out of 64 total) in the information technology sector that have reported thus far have seen earnings grow 19% from a year earlier on revenue growth of 9.5%. This is higher than expected yet the price of their stocks have faltered. This is what tends to happen in a market decline. In looking back to the year 2000, we are currently sitting with a an extreme of negative sentiment to US equities. Here is the chart of all institutions that are tracked by the FMS global investor poll:

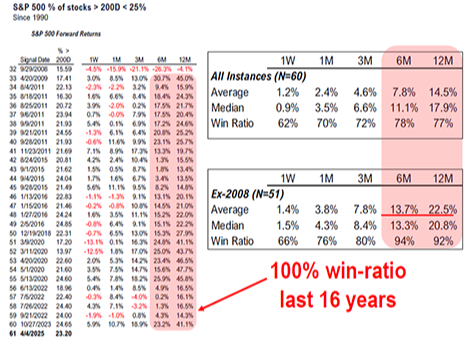

This clearly doesn’t tend to happen at highs, and if measured correctly, tends to coincide with low points. Historical context applied to the markets suggests to us that while risk near term remains elevated—opportunity midterm and longer term suggest portfolio diversification, quality assets and right sized expectations with more than a dollop of patience and perseverance point toward the potential of a likely reengagement of the bull market sometime in the not-too-distant future. In looking at times when the percentage of companies in the S&P 500 that are above their 200-day average price is less than 25% of all companies, the win ratio since 1990 going out 6 months to a year have shown that we are getting close to a pretty good time to deploy investment capital.

I can’t know when the coast is clear and it isn’t time to remain concerned about the course of the economy and the markets, but I can look at history and point out what has happened in the past. Never has the reason for the market declines or recoveries been the same as they are today, yet it has been a pretty good assumption that markets will recover. The question will then become, which companies / sectors / countries recover first and the most.

I want to close with one last study that I feel is always important. I follow this study on a weekly basis. It is the measure of the spread between what rate of interest is on high yield debt (more susceptible to fluctuations in the economy) compared to the rate of interest on US Treasury debt (the safest debt instrument). When the spread expands, there is implied fear of the future of the US economy and if it shrinks, there is confidence on the current and near future course of the US economy. If there truly was fear concerning the US economy, As can be seen below, the spread between these two rates is actually shrinking since the April 9th Tariff Spike. This is a very short-term analysis, but I find it interesting that the spread would shrink since the April 9th spike and then decline as our equity markets seemed to have found at least a short-term bottom. I will provide updates to this in weeks to come.

I believe that today’s note covers the data that we feel is important. Please let us know if we can answer any questions for you.

- Ken South, Tower 68 Financial Advisors, Newport Beach

-

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.