We are faced with a very clear dilemma currently. The media, the Fed, and the market prognosticators appear to be solely focused on interest rates and inflation. At the beginning of the year the expectations were for as many as seven interest rate cuts this year. This was based on the expected slowdown in the economy that was a result of supply chains improving, and a disastrous mortgage market that was thought to surely throw the brakes on everything home building / home buying related. But instead, we have been faced with strong labor numbers, wage growth, consumer prices and producer prices. I must admit that I stole the title of this week's newsletter from the journalist Justin Lahart who penned an article under the same title last Friday in the Wall Street Journal. Lahart opens his article talking about how the Federal Reserve is "still aiming" to lower interest rates later this year, and how households and small businesses are dependent on this. Fed chair Powell said at his Fed meeting last week that he "was prepared" to lower rates, but if it isn't needed, or if the economic indicators don't reflect a slowing trend, maybe these cuts just don't happen. Fed Governor Bostic said on Monday that he doesn't expect more than one cut, and that this cut possibly doesn’t happen till close to the end of the year! Wouldn't this upset all those hoping for rate cuts! Lahart goes on to quote current credit card interest rates and mortgage rates. I don't mean to sound judgmental, but if a spender knows what the cost is to use creditor money and it is too expensive, then they shouldn't spend the money!! instead they are complaining about the cost of using the money. If something is too expensive, don't buy it.

Enough about interest rates, I want to give some perspective on the stock market. On Saturday, Alan McKnight, chief investment officer at Regions Bank said, "We are moving from a Fed-driven rally to an economic and earnings driven rally." If the Investor Intelligence poll says that investors are scared and reticent, why is it that they are fully invested and benefiting from the economically driven equity markets? Seema Shar, chief global strategist at Principal Asset Management said, "If inflation is a little strong because the economy is strong, then that is still broadly good for equities." She goes on to warn, "So long as we are not talking about an inflation resurgence, it's fairly good news." As I have been bringing up week after week, if there is $6 Trillion on the sidelines and the consumer is flush with cash, the stock markets of the world are disengaging from the Fed because of the strength of the economy. This is super important.

If the entire US equity market was narrow, and completely dependent on the Magnificent Seven, then there could be a reason to be cautious and scared of future market movements. But this is not the case! Instead, not only is the market broadening here in the US, but equity markets across the globe are beginning to engage and move higher. If we are to look at the Magnificent Seven, it is clear that there are really only a couple of the seven that are keeping up a head of steam currently:

Instead, what we are seeing is the equal weighted S&P 500 (this is an index where all 500 companies have the same amount of vote in the value of this index, where the normal S&P 500 is capitalization weighted and a certain few have a dramatically greater vote) is breaking out to new cycle highs. This means the breadth of the market is expanding, and this is a sign of health! Not only is the equal weighted index going to these new cycle highs, but the NYSE advance / decline is as well. This means that more companies are joining the advance, and there are more advancers than there are decliners as well.

Another phenomenon that is occurring is that not only is the US market broadening, and more companies are participating, but the international markets are heating up as well. Many would say this is because the US Dollar is declining due to US interest rates topping out and therefore emerging markets and stocks and those of the Europe Stoxx 600 are getting attention. But what I believe is that this is a further illustration of the underlying strength of the markets and the broadening out of companies participating in the advance. Ari Wald, chief technical strategist at Oppenheimer had a brilliant chart that illustrated that the entire Europe Stoxx 600 has had a lid on it since before the tech bubble of 2000 and is now breaking out to the upside as well

All of these points are important:

- Magnificent Seven is now being joined by other companies out of the large-cap technology space.

- Breadth expansion is accelerating across other companies and other sectors.

- The US Dollar is declining- precipitating declining market interest rates, increases in crypto prices, and increases in gold prices.

- Economic forecasts for the jobless rate at year-end has declined to 4% where the expectation of a slowing economy was including higher unemployment projections.

- Personal Consumption Expenditure Index- excluding food and energy is now expected to be higher at 2.6%. Higher than the targeted 2% inflation rate.

- Gross Domestic Product is now expected to rise to 2.1% where in December it was expected to be 1.4%, again, stronger economics than expected.

According to Ed Hyman, Evercore ISI's head of the Economic Team, reckons that consumer net worth is up 9% in the first quarter from a year earlier. His team's proprietary survey of realtors also shows robust home prices. "It would be unusual for a recession to start with house prices this strong." As it stands, and as quoted in the Up & Down Wall Street section of Barron's this past weekend, "There's nothing for investors to fear these days but the lack of fear itself, to turn FDR's famous phrase on its ear, since complacency typically precedes a stock market drop." To provide an update on the status of the current leg of the advance see below:

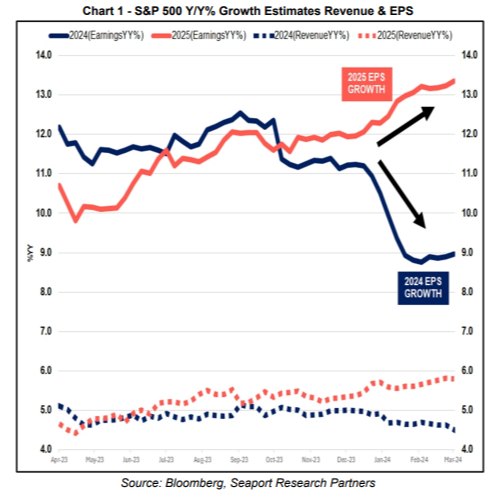

In the end, we are sure to get some kind of market digestion / pullback. What is going to cause this to happen? At present, other than valuations appearing a bit stretched, there really aren't a lot of issues that are apparent. Also, with there still being over $6 Trillion in short term cash, money markets and CDs, the 5% interest rate is appearing less and less attractive as investors who were scared are getting frustrated waiting for a chance to put their cash back to work in the equity market on a pullback. In the Personal Journal section of The Wall Street Journal last Thursday this was exactly the point of the article about 5% interest rates. One of the investors quoted said, "I enjoyed catching my breath with something really boring and safe." But in February they changed tactics and slowly began putting the money from the maturing instruments back into the stock market. Usually there are 2-3 chances per year when the equity markets pull back, and almost always one of them in the area of 7-10%. When we will get this is anyone's guess, but remember, to take advantage, particular after taxes on previous gains, could be futile at best, and if the economy remains strong and company earnings forecasts for 2025 remain robust, sticking with high quality could remain, longer-term, the best policy. Below is a picture of the expectations of earnings for 2024 and 2025, curtesy of Victor Cossel, Macro Strategist, Seaport Research Partners:

This chart is really the most important one for you to remember. Two points are clear. First, 2024 earnings are expected to pullback and hence the reason for the expectation of the rate cuts. Second, 2025 is supposed to be a year that benefits from these expected rate cuts. More than anything else, please remember that the stock market is a discounting mechanism that reflects what is expected 6-12 months out, not what is happening right now.

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

-

-

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.