We have officially entered the dog days of summer. This is when the weather gets hot, the ocean gets warm, the days are long, and the last thing that anyone wants to do is get up early to work all day (when the beaches are perfect) and then come home to prepare for the next day. This year is especially hard as we are faced with just so much stuff:

- Palestinian conflict

- Russia / Ukraine conflict

- Tariffs / trade disputes

- Israeli / Iranian conflict

I am sure that there are many other more domestic friction items that could be mentioned but suffice it to say that there is just a lot of stuff going on that does little to make the economy seem like it is poised for expansion and a time for companies to flourish. This is why I find it most important to separate the actions of the financial markets from discourse and human suffering.

This is especially true when it really doesn't matter what channel you turn on on the television, the radio, or in the press. Over the years, I have learned to really dive into the press, namely the Wall Street Journal, New York Times, Barrons, and Investor’s Business Daily. When I say “dive into” I mean to read the subtle intimations in articles rather than just the raw content. Context and subtleties can completely change the interpretation of the content and sway it to the political leanings of the author or the overall periodical. I read them for content, of course, but I pay special attention to tone. Tone is the subliminal aspect of the articles that are written. I find that quite often, normally in a more politically spectral periodical like the New York Times, issues are often twisted to fit their motives, but all the same address issues that deserve attention.

As an example, and of great importance, I am going to go into the articles that I feel are incredibly important as the content and the tone have relevance. I IMPLORE YOU TO READ THESE ARTICLES. I know this sounds a bit like homework, but if you really want to understand what is really going on, I think it would serve you well to read them. Now, they aren't long, so don't set aside hours, but instead maybe one at a time.

- Why Investors Are Stuck on the Sidelines- Wall Street Journal, May 31: with everything mentioned above, an investor hardly knows where to turn. This is incredibly important as it obviates the need to focus on what the markets are doing rather than focusing on the emotion of issues. What invariably ends up happening is an event occurs (Trump Tariff Day April 2nd, and Israel bombing Iran June 14) and the market sneezes. The press blows it up and then the markets recover when it is clear that these events, although painful, did little to affect the direction of global economies, consumption, production and technology. Then begins the FOMO (fear of missing out). Then, when it bounces and the problems continue there is a feeling of FOGI (fear of getting in). This is because the markets react and bounce then investors are left behind. Moral of the story, don't invest by emotion, invest based on quantifiable facts and studies.

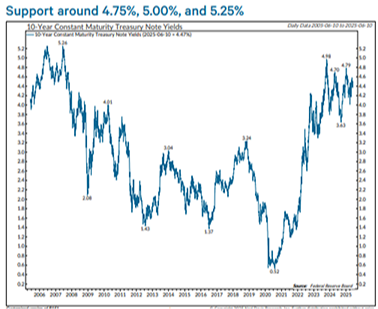

- Don't Fret. American Exceptionalism Isn't Dead Yet- Barrons, June 2: this is the backbone of all of them as I see it. Basically, just because foreign markets are finally catching a bid, the US equity markets, and economy should not be sold short. True, our markets could take a breath, and the capital could flow temporarily to markets outside our shores, but there has been little to slow the growth of US industry and the deflationary effect of technology & AI. The concern that continues to loom is the fiscal concern of US debt as it has hit $37 trillion. I often bring up the yield on US Treasuries, as the yields would be skyrocketing if there was a problem with US debt. Here is a chart of the yield on the 10-year US Treasury. Notice that it seems to be locked in a range since 2022 between 3.6%-4.8%.

Should there really be a problem this wouldn't be the case. Also, more than 60% of US households hold equities through brokerage accounts, IRAs, and 401-Ks, an investment level unmatched by other markets. That makes the US markets the only one big enough to absorb global capital flows. The US accounts for 64% of the global equity market capitalization and 41% of the global investment grade fixed income. Also, some 58% of foreign exchange reserves are in dollars. - Advisors Outsource Asset Choices- Wall Street Journal June 13: this was one of my favorites that I will not put away. It is stated that 8 out of 10 of the major investment firms use "models" to invest client capital. This basically means that the majority of investment firms are more fixated on sticking investors in a box with highly diversified mutual funds and ETFs than to strategically position a client’s portfolio and tailor it to their individual needs. The article says that "outsourcing some or all of their investment management frees up time for advisors to focus on client relationships." Now wait a minute! Isn't the client portfolio and needs predicated on the client relationship. Sounds more to me like the firms don't want the advisors to think, but instead to have them stuff clients in pre-fabbed boxes and be nothing more than a conduit to the firms' models. Does this sound like the way you earned your money to get you to where you are? I find this a terrible testament to the work most advisors put in to understand the financial markets and how they affect their clients' needs. I could really go on in this one, but you can read it yourself and then ask yourself if you call your advisor, can they really answer why you own what you own?

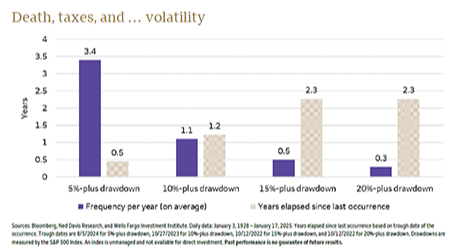

- Your Withdrawals And Gyrating Markets- New York Times, June 15: this one I found most surprising. It seems to touch on how to deal with volatility during uncertain times. As can be seen in the chart I often show, there are ALWAYS going to be uncertain times. This is simply the nature of the financial markets. Actually, there are corrections of around 5% + on average 3.4 times per year, 10%+ 1.1 times per year, 15%+ every 6 months, and over 20% quite seldom.

Given the more liberal leanings of the New York Times, they go on to say, "The Trump administration's aggressive stance toward government agencies and institutions like the Social Security Administration is also raising Americans' collective anxiety. Although polls have shown for some time that skepticism about the long-term health of Social Security has been pervasive among younger adults, more recent surveys show that this gloomy outlook has begun to take hold among older Americans. 70% of respondents between the ages of 45 and 60 believe that Social Security won’t be available for them." The woman they interview in the article says, "I put all my RMD (required minimum distribution) in savings because who even knows if Social Security is going to exist, with DOGE and all." I mean, let's be serious. What I find extremely important about this article is the tone of the person. There is no mention of the growth of the economy, the continued low level of unemployment, the wage growth, and clearly the lack of need up to this point to cut interest rates more due to the lack of softness of the economy.

To give a bit more attention to the conflict that ignited this last weekend, a ramp up in geopolitical risk because of an outbreak of hostilities historically has been a relatively short-term source of downward pressure on stocks when considered in the context of history. While markets stateside from the start of this week may well reflect concerns about the increase in hostilities in the Middle East that erupted on Friday and waged through the weekend (and are still occurring as I write this note), it is our view that historical context suggests downward pressure on stock prices is unlikely to be a protracted negative overhang on stocks. It’s not that equity markets are particularly hard or cynical but rather that military action and conflagration are often followed by a collective realization among investors that such destructive events eventually spur production. The eventual need to repair damage and rebuild inventories depleted by war activity eventually lead to the procurement of goods and services. Such underlying provisions and response often provide opportunities for businesses and innovators in meeting the needs of consumers and the businesses they serve that can lead to revenue and earnings growth.

We remain positive on equities-both US and foreign. Pullbacks earlier this year have mostly looked like “trims” and “haircuts” for the S&P 500 whenever bears, skeptics, and nervous investors have found a catalyst to take near term profits without FOMO (fear of missing out) amid what appears to us in fundamentals that persist in showing resilience like a very much intact bull market. Drivers of the bull market that in our view have provided resilience in the intermittent downdrafts that occurred in 2024 into this year include the success the Fed has had in pursuing tighter monetary policy that has brought down the pace of inflation since March of 2022 aided by resilience in consumer spending, S&P 500 earnings growth, and job growth, which have provided support for the US economy and the markets.

In looking at the current action of the S&P 500 Index, it can be seen quite clearly that the run from the lows in 2022 hit a high point where the market simply got tired and needed more fuel for another move higher. This high point sort of created an overhead ceiling on the markets. This began in December of last year. The first quarter of the first year of a new presidential term had the normal downdraft, and now we are right back there at the old highs. See below:

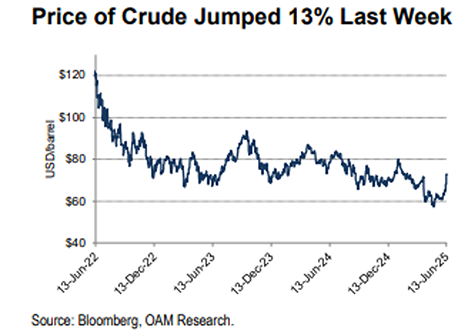

The price of West Texas Intermediate light crude rose 13% last week to close at $72.98 on June 13. Prices rose sharply on Friday (+7.3%) after Israel attacked Iran’s nuclear research sights and as Iran responded. Levels of global crude production and supply have restrained the price of oil this year on concerns about the strength of global economic growth tied to tariff related risks. Recent calls for increased production by OPEC have added pressure on the price of oil as well. The real issue is not so much Iran and its oil, as it is relatively small in overall oil exports, but rather the Strait of Hormuz. There was a particularly good article on this in Barrons this past weekend; War Upends the Oil Trade. How It Could Play Out. I would take the time to read it.

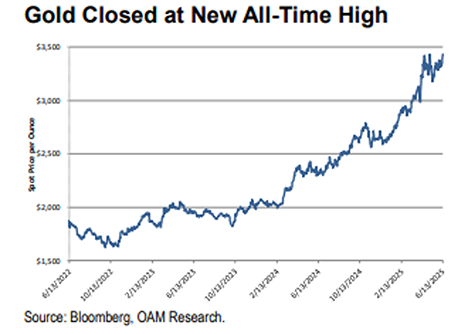

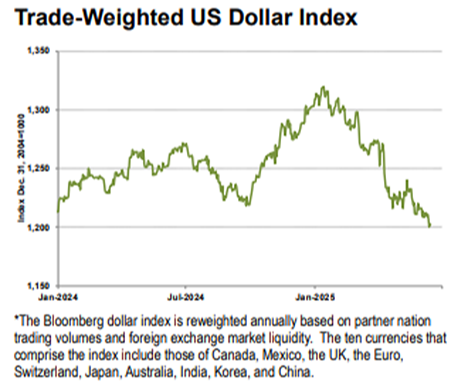

As a result of this conflict and the concerns about our domestic debt levels, the price of gold closed at a new all-time high on Friday, June 13 at $3432/oz. Rising tensions in the Middle East drove a flight to safety on Friday, which pushed the precious metal to a new high. I for one believe that the gold market is big enough for a lot of speculators to participate in it, yet small enough that big speculators can push it around. Given inflation where it is, this move in gold I believe is more deeply rooted in speculation and US Dollar weakness than the fear of inflation running rampant.

If one is to look at the price of gold most recently, it seems to be validated by the move down in the US Dollar. It is assumed that US Dollar weakness is weak=bad, but in reality, it is a function of trade and could actually be quite good for our domestic economy as our goods and services get cheaper to foreign consumers and theirs increase to US Dollar buyers from an exchange rate basis.

The United States consumes a large share of its GDP, China, not so much. The result is Yin and Yang. On net, China produces, and the US consumes. Treasury Secretary Scott Bessent put it this way last week at a Senate hearing – “China has a singular opportunity to stabilize its economy by shifting away from excess production towards greater consumption.” That is the rallying cry for tariffs and trade negotiations. And while the US government seems to blame it all on China, it is also true that the US has a “singular opportunity” to shift away from excess consumption toward greater production. And since consumption is almost 70% of GDP, this transfer of wealth should lift growth. In the real world, it doesn’t actually lift GDP, but it does lift consumption. Since 2008, real consumer goods expenditures are up 62% in the United States. Unfortunately, the most aggressive measure of US “value-added” manufacturing is only up 14%. In other words, because of government policy, the US economy is off kilter. We consume more than we produce…the exact opposite of China.

Don’t get us wrong: We are not asserting that China is playing fair; they aren’t. They steal intellectual property, they pay workers less than they should, and they take advantage of the US’s consumer-driven society. On top of that, they want to undermine US geo-political strength. What we are saying is that the US needs to stop subsidizing consumption and punishing production.

In closing, where does this leave us currently? We are currently in sort of a holding pattern. Q1 earnings are out, Fed meets today, the “big, beautiful bill” is sort of like a golf ball trying to go down the throat of our economic snake, and there are more than a handful of international conflicts still in full swing. When there is this much “stuff” going on, I tend to focus more on the bond market. If things are really getting bad or are getting ready to get bad, it is usually sniffed out by the bond market. The spread between high-yield debt and US Treasury debt expands and fear of impending economic difficulty is telegraphed. As can be seen below, we are right back where we were, and no major economic timebombs seem to be present. This never accounts for a black swan type of event, but as can be seen, the Israel-Iran conflict is having far less affect on our bond market than the Tariff Tussle did:

- Ken South, Tower 68 Financial Advisors, Newport Beach

-

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

Data sourced from Bloomberg (2025).

Stock investing includes risks, including fluctuating prices and loss of principal. (132-LPL)

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise. Bonds are subject to availability, change in price, call features and credit risk. (116-LPL)

Government bonds are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

Bond yields are subject to change. Certain call or special redemption features may exist which could impact yield.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.