August is done and even though it tends to be a negative month, we ended up without even a scratch. Second quarter earnings are over and, as has been the norm, earnings generally beat expectations and revenue expectations going forward were raised. It should be noted that they were raised, but not raised to the extent they have been for the last number of quarters. This is not abnormal given that we are facing a contentious election, and the third quarter tends to be sort of a no-man's-land quarter when most companies are coming off the summertime doldrums and not yet ready to announce what their plans are for the coming year. When I see things as sort of unknown, I tend to focus on what I do know is going on. These are facts that I attempt to quantify and then apply to different asset classes and different sectors & leading companies in these sectors. At present, we are dealing with three things that I think deserve our attention:

Seasonal Headwinds & The Election Cycle

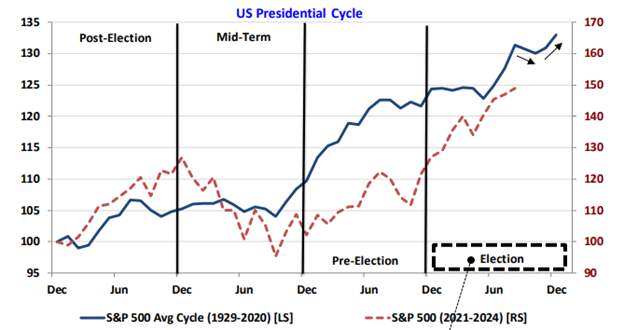

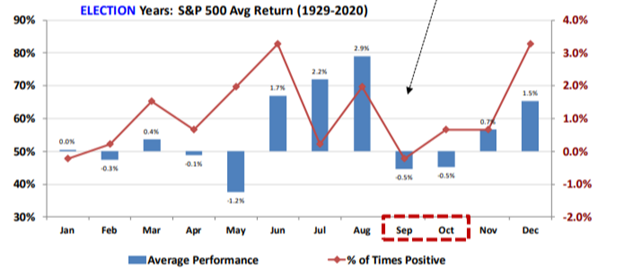

Seasonal trends have historically become a headwind for the equity market. As I said above, coming off of summertime, the momentum of companies tends to have slowed, and it often takes a couple of months for them to get cranked back up into year end. Since 1929, the S&P 500 has averaged negative returns in both September and October, particularly during a Presidential election year. This leads us to believe a seasonal setback, or at least a sideways breather would be reasonable ahead of a year-end rally. It should also be remembered that September is historically the worst performing month of the year. As can be seen below, this year is trending as is the norm for a presidential election year. The chart below this gives the historical returns by month in these presidential election years since 1929. Clearly September and October are the months that investors should be most careful. Overall, while a seasonal setback has become an increasing risk within a maturing cycle, we think the bull is intact and that weakness should be selectively bought.

When do Equity Investors Need to Worry About a Recession?

This issue is the one that I have been focusing on and is what I feel is really the most important one. The banter about Fed Chairman Powell and his directional call for interest rates and his timing for a cut is what seems to be the underlying factor affecting the currency markets and the bond markets. Given that these two tend to set the stage for the equity markets, I have been really quite impressed with the way he has telegraphed his intentions and as such been able to alter rates without too many shock waves to the stock markets of the world. Since raising rates at a ferocious rate during 2022, recession fears have been at the forefront of investors' minds for nearly three years. The debate started when Jerome Powell declared that the Fed was willing to push the US economy into recession to keep inflation expectations in check. Concerns ebbed and flowed, but four major points have been in play:

- The most aggressive tightening cycle in four decades.

- The longest yield curve inversion (when shorter-term interest rates are higher than longer-term rates- usually precedes a recession) on record.

- Two years of contraction in leading economic indicators. This was to be expected as the economy had a shot of adrenaline when money was "helicoptered" into the economy during the pandemic.

- The fairly unknown indicator- The Sahm Rule, has kept recession fears front and center.

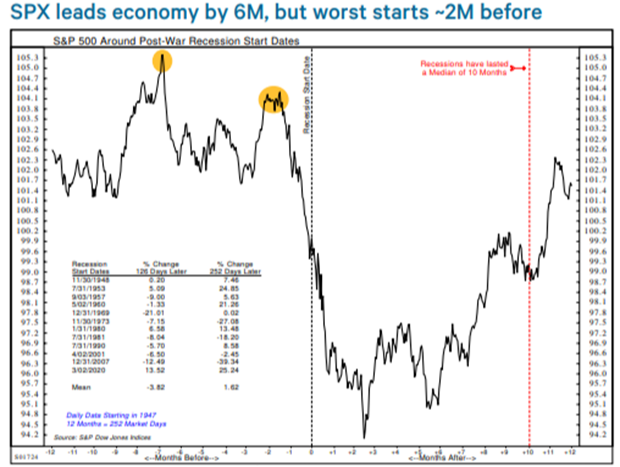

Even Google searches for "recession" have been higher than normal 66% of the time for the past 18 months. For equity investors, the questions of if and when a recession is coming are paramount. The "if" matters since the worst bear markets have been associated with recessions, with an average decline of 35%! The challenge of course is the "when." Economists do not have a great track record of identifying recessions beforehand. As I explained last week, the stock market tends to lead the economy, waiting for an official declaration is far too late normally. On average, the S&P 500 peaks around six months before the start of recessions.

A natural inclination may be to not use the economic data for investment purposes. Instead, we believe that sentiment and technical indicators are more likely to identify market turning points first, with macro-economic indicators and fundamentals confirming these. According to Ari Wald, when over 65% of the NYSE is above its 200-Day moving average, this tends to not be a time when markets roll over and decline. We are above this now and breadth seems to be expanding rather than shrinking, another positive indicator that money is spreading out in the major indexes to sectors that were lagging before. These kinds of indicators tend to provide clues earlier than traditional sources. Currently, their conclusion is that the risk of recession over the next several months is low. Just last week the GDP number came out. It was expected to be up by 2.8% and it came in up 3%. This is hardly recessionary.

While it is always good to do one's homework and have a plan for the next recession, our conclusion is that it is too soon to turn defensive on equities. A closer examination of history yields a secondary reason: while the S&P 500 peaked about six months before the start of recessions, the worst of the damage did not start until about two months beforehand. The stock market entered a protracted downtrend well before recessions started in 1969, 1973, and 2001. In two of the three cases, bursting bubbles triggered the initial declines. In 1973 it was the Nifty 50 and in 2001 it was the Dot-Com bubble. These were some of the worst since the Great Depression. If one were to see the A.I. stocks as a bubble, the Fed easing too soon, or the market entering a secular bear, then these three previous examples would be relevant in 2024. This is not what we see as the case. Instead, a slowing growth cycle of "soft landing" is really what we see on the horizon if anything. Given the amount of information at virtually anyone's fingertips, the markets tend to discount or handicap information sooner and quicker, so the imminent risk of recession is low so I find it too early to turn overly bearish other than normal seasonal market digestion.

Harris vs. Trump on the Economy

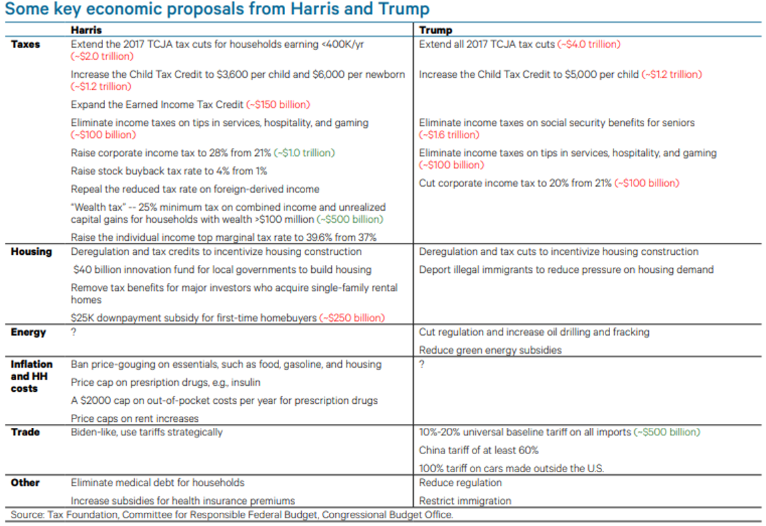

With both party conventions now behind us, and with less than three months until election day on November 5th, neither Kamala Harris nor Donald Trump have released comprehensive economic plans. There are, however, sufficient details in their proposals so far to assess their potential impact on the economy and equities. Based on their public commentaries, both will run up budget deficits which will stimulate economic growth. Below is a table from Ned Davis Research for you to see some key economic proposals from them both. These are of course preliminary in nature, but I feel a good source of initial reference.

With the prospect of a rate cut now less than a month away, it is tougher to imagine the stock market selling off too hard. The last two Fridays have finished quite strong, since the recent lows in early August. That suggests the buying is more likely for real and sustainable for at least an attempt to break out over the prior highs in the larger averages. Even when heavy-weight Nvidia slid the averages were still able to keep their uptrend intact. I do think that we could enter a "sell the news" event at some point during the Fed meeting on September 18th, but this should be after continued strength. Historically, according to the Stock Trader's Almanac, the S&P 500 tends to top out, at least temporarily, around September, during presidential election years. The decline begins, on average, in late September during "all" election years, but has historically started in early September. In most cases, stocks tended to rally into the end of the year after shaking off the pre-election weakness. Should that tendency play out again, it would sync up well with a move sometime after the expected Fed rate cut. As long as dips remain mild and over key support, however, I think we have to expect an eventual resolution higher into year end.

- Ken South, Newport Beach Financial Advisor

Get Ken's Weekly Market Commentary Delivered To Your Inbox!

Important Disclosures:

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial professional prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal.

The Standard & Poor's 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Nasdaq-100 is a large-cap growth index. It includes 100 of the largest domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.